🤑AP Microeconomics Unit 3 Review

3.7 Perfect Competition

3.7 Perfect Competition

Unit & Topic Study Guides

Unit 1 – Basic Economic Concepts

Unit 2 – Supply and Demand

Unit 3 – Production, Cost, and the Perfect Competition Model

Unit 4 – Imperfect Competition

Unit 5 – Factor Markets

Unit 6 – Market Failure and the Role of Government

AP Microeconomics Exam

Big Ideas

Perfect competition is a market with many small firms selling identical products, no barriers to entry or exit, and no individual control over price. Each firm is a price taker that maximizes profit where MR = MC, and in long run equilibrium firms earn zero economic profit while the market reaches both allocative and productive efficiency.

Perfect Competition in Microeconomics

In microeconomics, perfect competition is the benchmark market structure: many firms, identical products, no barriers to entry or exit, and no market power. A perfectly competitive firm is a price taker, so the market graph sets price and the individual firm faces a horizontal demand curve where D = MR = P.

For AP Micro, most perfect competition questions come down to the side-by-side graph. Use the market graph to find price, move that price to the firm graph, produce where MR = MC, and then compare price with ATC and AVC to identify profit, loss, or shutdown.

Why This Matters for the AP Microeconomics Exam

Perfect competition is the benchmark model you use to judge every other market structure later in the course. Once you can draw and read the side-by-side market and firm graphs, label profit and loss areas, and trace the move from short run to long run, you have the core toolkit for the rest of AP Microeconomics.

On the exam you may need to:

- Define the characteristics of perfect competition and efficiency, using graphs where appropriate.

- Explain firm decisions and how competitive prices lead to efficient outcomes.

- Calculate economic profit or loss from a graph or table.

This topic rewards careful graphing, accurate cause-and-effect reasoning about entry and exit, and clean use of terms like price taker, allocative efficiency, and productive efficiency.

Key Takeaways

- A perfectly competitive market has many small firms, identical (homogeneous) products, no barriers to entry or exit, and no market power, so each firm is a price taker.

- The firm's demand curve is horizontal (perfectly elastic), and for that firm price equals marginal revenue, so D = MR = P.

- Firms maximize profit (or minimize loss) by producing where MC = MR (= P).

- In the short run a firm can earn economic profit, take a loss, or shut down, depending on where price sits relative to ATC and AVC.

- Free entry and exit push the market to long-run equilibrium, where price equals minimum ATC and firms earn zero economic profit (normal profit).

- Long-run competitive equilibrium is both allocatively efficient (P = MC) and productively efficient (P = minimum ATC).

Characteristics of Perfect Competition

Every good is sold inside some market structure, and perfect competition is the first model you study in depth. It is defined by a specific set of traits:

- Many small firms: There are so many firms that no single one can influence the market price.

- Identical (homogeneous) products: Buyers see no difference between one firm's output and another's, so there is no reason to prefer a specific seller.

- No barriers to entry or exit: Firms can freely join the market when there is profit and leave when there are losses.

- Price takers: Firms have no market power. They must accept the price set by market supply and demand. Raising price loses all customers to competitors selling the identical good at the market price; lowering price just sacrifices revenue, since the firm can already sell all it wants at the market price.

Because products are identical and every firm charges the same market price, there is no role for non-price competition like advertising in this model. The agriculture industry is often used as an example: oranges from different farms look the same to a buyer and sell for the same price, so no single grower advertises to stand out. Treat that as an illustration of the concept, not a required AP example.

These traits lead directly to the model's big results: prices signal everyone's marginal costs and marginal benefits, and in the long run firms break even while the market reaches efficiency.

Side-by-Side Graphs in Perfect Competition

Perfect competition uses two graphs drawn next to each other. The pair lets you show the price taker idea and connect what happens in the whole market to what happens at a single firm.

Label the vertical axis P/C (price and cost can both appear there) and the horizontal axis Q (quantity).

- Left graph (market): the standard supply and demand graph from earlier units. Market price is set here.

- Right graph (firm): a single firm's graph. The firm faces a horizontal, perfectly elastic line that represents demand, marginal revenue, and price all at once: D = MR = P. Because every unit sells at the same market price, the extra revenue from one more unit (marginal revenue) equals that price.

The horizontal firm demand line is the visual proof that the firm is a price taker. It cannot charge more without losing all buyers, and it has no reason to charge less.

Short-Run Graphs: Profit, Loss, and Shutdown

In the short run, a competitive firm graph can show one of three outcomes at the profit-maximizing quantity (where MR = MC). Compare the price line to the ATC and AVC curves.

Short-run profit: both ATC and AVC sit below the price line at the MR = MC quantity.

Short-run loss (but still operating): ATC is above the price line at MR = MC, but AVC is below the price line. The firm loses money but covers its variable costs, so it keeps producing in the short run.

Shutdown: both ATC and AVC are above the price line at MR = MC. Price cannot cover average variable cost, so the firm produces zero in the short run.

To find the profit or loss area, use (P - ATC) times Q at the profit-maximizing quantity. A positive result is profit; a negative result is a loss.

Long-Run Perfectly Competitive Graph

In long-run equilibrium, the price line is tangent to ATC at the profit-maximizing quantity (MR = MC). At that single point, price equals marginal cost and price equals minimum ATC, so the firm earns zero economic profit (normal profit).

This outcome is both:

- Allocatively efficient: P = MC, so the price buyers pay for the last unit equals the marginal cost of producing it. Resources go to their most valued use.

- Productively efficient: P = minimum ATC, so firms produce at the lowest possible average cost (efficient scale).

Shift from Short Run to Long Run

When short-run firms earn profits or losses, entry or exit moves the market toward long-run equilibrium. This is the central cause-and-effect chain to know well.

Starting from profit: Economic profit attracts new firms. Entry shifts market supply right, which lowers the market price. On the firm graph, the price line drops until it is tangent to ATC. Each firm's profit-maximizing quantity falls, the market quantity rises (more firms total), and economic profit returns to zero.

Starting from a loss: Losses push firms to exit. Exit shifts market supply left, which raises the market price. On the firm graph, the price line rises until it is tangent to ATC. Each remaining firm's profit-maximizing quantity rises, the market quantity falls (fewer firms total), and losses shrink to zero.

Shift from Long Run to Short Run and Back

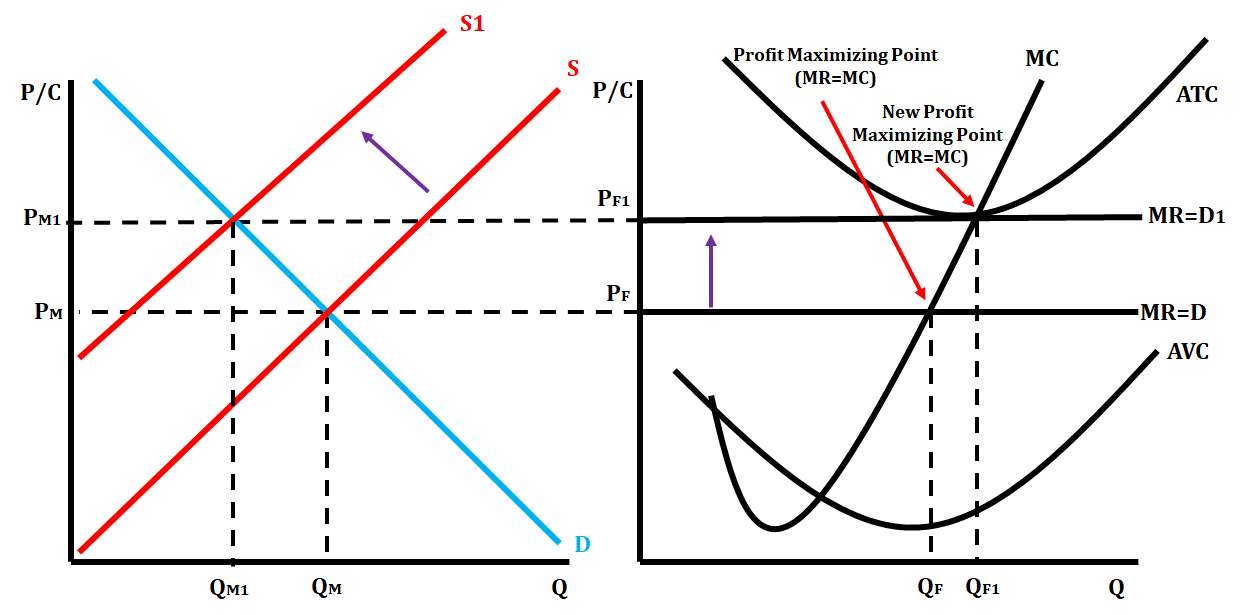

A common multi-step problem starts you in long-run equilibrium, hits the market with a demand change, and asks you to adjust back to long run. Here is the chain using the apple market as an example.

Step 1: Demand changes. Suppose the price of peaches (a substitute) rises. Buyers want fewer peaches and more apples, so demand for apples shifts right and the equilibrium price rises. On the firm graph, the price line rises and you find the new MR = MC quantity. Since price is now above ATC, the firm earns a short-run profit.

Step 2: Adjustment back to long run. Short-run profit attracts entry. New firms shift market supply right, which lowers the equilibrium price. On the firm graph, the price line falls back down, and the firm's profit-maximizing quantity returns toward its original level. Economic profit returns to zero, and the market is back in long-run equilibrium.

The same logic runs in reverse for a decrease in demand: short-run loss, then exit, then a rise in price back to long-run equilibrium. Any time a competitive market is pushed out of long-run equilibrium, entry or exit returns it.

Long-run market price also depends on whether the industry is constant cost, increasing cost, or decreasing cost, which reflects the part of the long-run cost curves firms operate on.

How to Use This on the AP Microeconomics Exam

Free Response

- Draw the side-by-side graphs cleanly: market on the left, firm on the right, with P/C and Q labeled.

- On the firm graph, always show D = MR = P as one horizontal line, and place MC, ATC, and AVC correctly.

- Mark the profit-maximizing quantity at MR = MC, then shade the profit or loss rectangle and state whether it is profit, loss, or break-even.

- When asked to adjust to the long run, name the cause (entry or exit), show the correct supply shift, and explain how price returns until P = minimum ATC and profit is zero.

Problem Solving

- Economic profit per problem: (P - ATC) times Q at the MR = MC quantity.

- Operate vs. shut down in the short run: keep producing if P is at or above AVC; shut down if P is below AVC.

- Long-run signal: profit means entry, loss means exit, zero economic profit means no change.

Common Trap

- Do not slope the firm's demand curve. In perfect competition it is horizontal.

- Read AVC, not just ATC, when deciding whether to shut down.

Common Misconceptions

- Zero economic profit does not mean zero accounting profit. Zero economic profit (normal profit) means the firm is covering all costs, including implicit costs like the owner's time and the opportunity cost of invested capital.

- Price takers can still earn short-run profit or loss. Being a price taker only means the firm cannot set price. In the short run it can still profit, lose, or shut down depending on where price sits relative to ATC and AVC.

- Shut down is not the same as exit. Shutdown is a short-run decision to produce zero output while still paying fixed costs. Exit is a long-run decision to leave the industry entirely once all costs are variable.

- Allocative and productive efficiency are different. Allocative efficiency is P = MC (the right amount is produced). Productive efficiency is P = minimum ATC (it is produced at lowest average cost). Long-run competitive equilibrium achieves both.

- More firms entering does not raise the price. Entry increases market supply, which pushes the market price down and erodes profit. Exit does the opposite.

- The firm's MR is not below its price. Because every unit sells at the market price, MR equals price for a competitive firm, unlike in imperfect competition.

zontal line. The firm can sell all output at the market price.

How do you find the profit-maximizing quantity in perfect competition?

Find the quantity where marginal revenue equals marginal cost, or MR = MC. Since the firm is perfectly competitive, MR is also equal to price.

How do you tell profit or loss on a perfect competition graph?

Compare price to ATC at the MR = MC quantity. If price is above ATC, the firm earns profit. If price is below ATC, the firm has a loss.

When should a perfectly competitive firm shut down?

In the short run, the firm shuts down if price is below AVC. If price is at or above AVC, it keeps producing even if it has a loss.

What happens in long-run perfect competition?

Entry and exit push firms to zero economic profit. In long-run equilibrium, price equals marginal cost and minimum ATC, so the market is allocatively and productively efficient.

Related AP Microeconomics Guides

Vocabulary

The following words are mentioned explicitly in the AP® course framework for this topic.Term | Definition |

|---|---|

allocative efficiency | An economic outcome where price equals marginal cost and resources are allocated to their highest-valued uses. |

average total cost | The total cost of production divided by the quantity of output produced. |

barriers to entry | Obstacles that prevent new firms from entering a market, allowing existing firms to maintain market power. |

constant cost industry | An industry where long-run average costs remain unchanged as industry output expands or contracts. |

decreasing cost industry | An industry where long-run average costs fall as industry output expands due to economies of scale or decreased input prices. |

economic losses | A situation where a firm's total revenue is less than its total economic cost, resulting in negative economic profit. |

economic profit | The difference between total revenue and total economic cost, including both explicit and implicit costs. |

efficiency | A market outcome where resources are allocated to maximize total surplus and no mutually beneficial trades remain unexploited. |

efficient outcomes | Market results where resources are allocated such that no one can be made better off without making someone else worse off, maximizing total surplus. |

equilibrium | The market condition where the quantity supplied equals the quantity demanded, resulting in a stable price with no tendency to change. |

firm decision making | The process by which firms determine production levels and pricing strategies to maximize profit or minimize losses. |

firm entry | The process by which new firms begin operations in a market, typically in response to economic profits. |

firm exit | The process by which existing firms leave a market, typically in response to economic losses. |

increasing cost industry | An industry where long-run average costs rise as industry output expands due to increased input prices. |

long-run competitive equilibrium | A market condition where firms earn zero economic profit, price equals marginal cost and minimum average total cost, and no incentive exists for entry or exit. |

marginal benefits | The additional benefit or satisfaction gained from consuming or producing one more unit of a good. |

marginal costs | The additional cost incurred from producing one more unit of output. |

marginal revenue | The additional revenue a firm receives from selling one more unit of output. |

market power | The ability of a firm to influence the price of a product by changing the quantity it supplies. |

perfectly competitive markets | Markets characterized by many buyers and sellers, homogeneous products, free entry and exit, and perfect information where individual firms are price takers. |

price taker | A firm that cannot influence the market price and must accept the price determined by market supply and demand. |

productive efficiency | An outcome where firms produce at the lowest possible average total cost, minimizing waste and maximizing output from available resources. |

profit maximization | The process of determining the output level where the difference between total revenue and total cost is greatest. |

short-run competitive equilibrium | A market condition where firms produce where marginal cost equals marginal revenue, and price may differ from long-run levels, resulting in economic profits or losses. |

Frequently Asked Questions

What is perfect competition in microeconomics?

Perfect competition is a market structure with many small firms, identical products, no barriers to entry or exit, and no market power. Firms are price takers.

What does D = MR = P mean for a perfectly competitive firm?

It means the firm's demand curve, marginal revenue, and price are the same horizontal line. The firm can sell all output at the market price.

How do you find the profit-maximizing quantity in perfect competition?

Find the quantity where marginal revenue equals marginal cost, or MR = MC. Since the firm is perfectly competitive, MR is also equal to price.

How do you tell profit or loss on a perfect competition graph?

Compare price to ATC at the MR = MC quantity. If price is above ATC, the firm earns profit. If price is below ATC, the firm has a loss.

When should a perfectly competitive firm shut down?

In the short run, the firm shuts down if price is below AVC. If price is at or above AVC, it keeps producing even if it has a loss.

What happens in long-run perfect competition?

Entry and exit push firms to zero economic profit. In long-run equilibrium, price equals marginal cost and minimum ATC, so the market is allocatively and productively efficient.