🤑AP Microeconomics Unit 1 Review

1.5 Cost-Benefit Analysis

1.5 Cost-Benefit Analysis

Unit & Topic Study Guides

Unit 1 – Basic Economic Concepts

Unit 2 – Supply and Demand

Unit 3 – Production, Cost, and the Perfect Competition Model

Unit 4 – Imperfect Competition

Unit 5 – Factor Markets

Unit 6 – Market Failure and the Role of Government

AP Microeconomics Exam

Big Ideas

Cost benefit analysis is how rational decision makers compare what they give up against what they gain to find the best choice. You add opportunity cost (both explicit and implicit costs) to find total economic cost, then either compare total benefits to total costs or compare marginal benefit to marginal cost depending on the type of decision.

Why This Matters for the AP Microeconomics Exam

This topic builds the decision-making logic that runs through the entire AP Microeconomics course. Once you understand how rational agents weigh costs against benefits, the later units on consumer choice, firm production, profit maximization, and market efficiency make much more sense because they all use the same compare-the-extras reasoning.

On the exam, expect to:

- Calculate opportunity cost from a word problem, including forgone wages and time.

- Read a cost-benefit table or graph and identify the optimal quantity.

- Explain why a decision is or is not rational using costs and benefits.

- Distinguish when to use total comparisons versus marginal comparisons.

Free-response prompts in this course often ask you to calculate a value and then explain your reasoning, so showing your work matters.

Key Takeaways

- Total economic cost includes both explicit costs (out-of-pocket money) and implicit costs (the value of the best forgone alternative, including time).

- Opportunity cost is the value of what you give up, and rational agents always factor it in.

- Total net benefit equals total benefits minus total costs, and it is largest at the optimal choice.

- For divisible decisions, the optimal quantity is where marginal benefit equals marginal cost.

- Some decisions are lumpy (all-or-nothing) and must be judged by comparing total benefits and total costs instead of using marginal steps.

- Benefits are measured as utility for consumers and total revenue for firms.

Explicit and Implicit Costs

Every choice has a total economic cost, and that cost has two parts.

Explicit costs are direct money payments. Think tuition, the price of a ticket, raw materials, rent, or wages a firm pays. These are easy to count because money actually changes hands.

Implicit costs are the value of the next-best option you give up when you use a resource. No money leaves your pocket, but you still sacrifice something. If you spend five hours at an event instead of working, the wages you skip are an implicit cost. If a business owner invests their own money in a project, the return they could have earned elsewhere is an implicit cost.

Add them together and you get the full picture:

</>CodeTotal economic cost = explicit costs + implicit costs (opportunity costs)

This is why economists insist that opportunity cost shows up in every decision. Ignoring implicit costs makes an option look cheaper than it really is.

Total Benefits and Total Costs

Benefits are the payoff from a choice. For consumers, total benefit is measured as utility (often counted in made-up units called utils). For firms, total benefit is total revenue.

Total net benefit is the difference between total benefits and total costs:

</>CodeTotal net benefit = total benefits - total costs

The optimal choice is the one that makes total net benefit as large as possible. On a graph with a total benefit curve and a total cost curve, this is the point where the vertical gap between the two curves is biggest.

Marginal Benefit and Marginal Cost

Total values tell you the whole amount, but most decisions are made one step at a time. That is where marginal thinking comes in.

Marginal benefit (MB) is the extra benefit from one more unit. Marginal cost (MC) is the extra cost of that same unit.

Picture eating pizza. The first slice might give you 8 utils, the second 3, the third 2. Each slice still adds something, but less than the one before. That shrinking pattern is diminishing marginal utility: as you consume more of a good, the satisfaction from each extra unit eventually falls. It explains why nobody wants to consume infinite amounts of anything.

Marginal costs can be constant (each extra slice costs the same) or can change as you consume more.

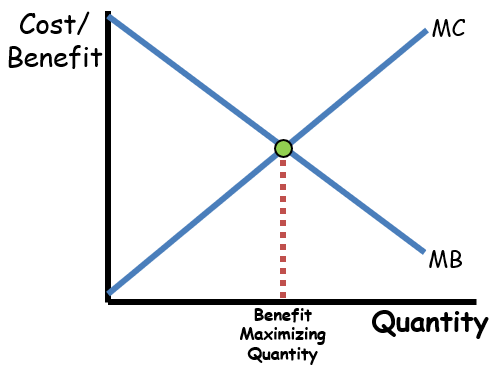

The Marginal Decision Rule (MB = MC)

When a decision can be broken into small increments, use this rule to find the optimal quantity.

Compare MB and MC at each quantity. There are three cases:

- MB > MC: the extra unit adds more benefit than cost, so keep going.

- MB < MC: the extra unit costs more than it is worth, so stop.

- MB = MC: you have reached the optimal quantity. Net benefit is maximized here.

Because of diminishing marginal utility, MB falls as you consume more, so you eventually hit the point where MB meets MC. Consume up to that point and no further.

To the left of the optimal point, MB is greater than MC, so you should consume more. To the right, MB is less than MC, so you have gone too far. If no quantity makes MB exactly equal MC, consume every unit where MB is still at least as large as MC, and stop before MB drops below MC.

Total Versus Marginal: Knowing Which to Use

Not every decision can be sliced into units.

- Divisible (incremental) decisions: you can add one unit at a time, like how many sodas to buy. Use the marginal rule (MB = MC).

- Lumpy (all-or-nothing) decisions: you either do the whole thing or not at all, like building a single bridge or taking a specific job. You cannot evaluate these in small steps, so compare total benefits to total costs and pick the option with the larger net benefit.

Both methods point to the same goal: the largest possible net benefit. They just fit different kinds of choices.

One more rule for both cases: ignore sunk costs. Money or benefits already locked in by past choices do not change the optimal quantity going forward. Only future costs and benefits should affect your decision.

How to Use This on the AP Microeconomics Exam

Problem Solving

For opportunity cost questions, total up explicit costs and implicit costs:

- List the money actually spent (explicit).

- Add the value of what was given up, especially forgone wages or income from time (implicit).

- Do not include costs you would pay no matter what you chose, because those are not part of the trade-off.

For optimal-quantity questions with a table, scan down the marginal benefit column and find the last unit where MB is still at least the price (MC). That unit is the optimal quantity.

Free Response

When a prompt says "calculate," show every step and your arithmetic, then state the final number with correct units. When it says "explain," connect your answer back to the logic: why MB = MC is optimal, or why a forgone option counts as a cost. Stating a number without reasoning usually leaves points on the table.

Common Trap

Watch for costs that appear no matter which option you pick, like clothing or other everyday expenses. Those are not opportunity costs of the specific choice because you would pay them either way.

Worked Examples

Example 1: Opportunity cost of community college

After high school, Billy enrolls in a two-year community college program instead of accepting an internship paying $15,000 per year. Annual tuition and fees are $5,000. What is the annual opportunity cost of attending?

Answer: $20,000

Why: Opportunity cost includes both explicit and implicit costs. The $15,000 salary he gave up is the implicit cost, and the $5,000 in tuition and fees is the explicit cost. Together that is $20,000.

Example 2: What does not count

All of the following are included in computing the opportunity cost of attending college EXCEPT:

(A) interest paid on student loans (B) wages the student gave up to attend college (C) money spent on books and supplies (D) money spent on college tuition (E) money spent on clothing expenses

Answer: (E)

Why: You will have clothing expenses no matter what you choose, so they are not part of the trade-off of attending college.

Example 3: Opportunity cost with time and a discounted ticket

Sylvia earns $12 per hour at a part-time job. She wants to attend a sporting event. The full price is $100, but she buys a discounted ticket for $75 from her cousin. If she takes 5 hours off work to attend, what is her opportunity cost?

Answer: $135

Why: She gives up $60 in wages (5 hours times $12), which is her implicit cost, and she pays $75 for the ticket, which is her explicit cost. $60 + $75 = $135. The $100 full price does not matter because she did not pay it.

Example 4: Finding the optimal quantity from marginal benefit

Jane's marginal benefit per day from drinking Pepsi is shown below. She values the first Pepsi at $1.25, the second at $1.20, and so on. If the price of a Pepsi is $1.00, how many should she drink?

Answer: 3 Pepsis

Why: The price ($1.00) is the marginal cost. Jane should buy each Pepsi where MB is at least MC. The first gives $0.25 of surplus, the second $0.20, and the third $0.00 (MB = MC). After the third, MB drops below $1.00, so a fourth Pepsi would cost more than it is worth.

Common Misconceptions

- Opportunity cost is only money spent. It also includes implicit costs like forgone wages or the value of your time. Leaving these out understates the true cost.

- The full price of something is always the cost. Only what you actually give up counts. If Sylvia paid $75, not $100, her explicit cost is $75.

- Costs you pay no matter what belong in opportunity cost. Expenses you would have under any choice, like everyday clothing, are not part of the specific decision's trade-off.

- You should consume until benefit runs out. You stop where MB equals MC, not where total benefit stops rising in raw terms. Consuming into the MB < MC zone reduces net benefit.

- Sunk costs should guide future choices. Money already spent cannot be recovered and should not affect the optimal quantity going forward.

- Every decision uses the marginal rule. All-or-nothing (lumpy) decisions cannot be broken into units, so you compare total benefits and total costs instead.

Related AP Microeconomics Guides

Vocabulary

The following words are mentioned explicitly in the AP® course framework for this topic.Term | Definition |

|---|---|

explicit costs | Direct, out-of-pocket monetary payments made for resources and inputs used in production. |

implicit costs | Opportunity costs of using resources owned by the firm that do not involve direct monetary payments, such as the cost of financial capital, compensation for risk, or an entrepreneur's time. |

marginal benefits | The additional benefit or satisfaction gained from consuming or producing one more unit of a good. |

marginal costs | The additional cost incurred from producing one more unit of output. |

opportunity cost | The value of the next best alternative that must be given up when making an economic choice. |

optimal choice | The decision that maximizes total net benefits by producing the greatest difference between total benefits and total costs. |

rational agents | Economic decision-makers who make choices by comparing benefits and costs to maximize their satisfaction or profit. |

total benefit | The overall satisfaction or gain received from consuming or producing a given quantity of a good or service. |

total cost | The sum of all fixed costs and variable costs at a given level of output. |

total economic costs | The sum of all explicit and implicit costs associated with a decision or production choice. |

total net benefits | The difference between total benefits and total costs; represents the overall gain or loss from a decision. |

total revenue | The total income a firm receives from selling its goods or services, calculated as price multiplied by quantity sold. |

utility | The total satisfaction or benefit that a consumer receives from consuming goods and services. |

Frequently Asked Questions

What is cost-benefit analysis in AP Microeconomics?

Cost-benefit analysis is the process rational agents use to compare the total benefits and total costs of a choice. The best option is the one with the greatest net benefit.

What is opportunity cost?

Opportunity cost is the value of the next-best alternative given up when a choice is made. It includes both explicit costs, like money paid, and implicit costs, like forgone wages or time.

What is the difference between explicit and implicit costs?

Explicit costs are direct payments, such as tuition or rent. Implicit costs are the value of resources used in another way, such as income you give up by choosing one activity over another.

How do you find total net benefit?

Total net benefit equals total benefits minus total costs. The optimal choice is where total net benefit is highest, which is also the largest vertical gap between total benefit and total cost on a graph.

When should you use marginal benefit and marginal cost?

Use marginal benefit and marginal cost when a decision can be broken into increments. Choose each unit where marginal benefit is at least marginal cost, and stop before marginal cost exceeds marginal benefit.

How is AP Micro 1.5 tested?

AP Micro 1.5 is tested with opportunity cost calculations, tables, graphs, and explanations of rational choice. Be ready to decide whether a situation calls for total cost-benefit comparison or marginal analysis.