Posterior predictive distributions are a key concept in Bayesian statistics, combining observed data with prior beliefs to make future predictions. They play a crucial role in model evaluation, forecasting, and decision-making by incorporating uncertainty in both parameter estimates and future observations.

These distributions are calculated by averaging the likelihood of new data over the posterior distribution of model parameters. They serve as a powerful tool for assessing model fit, generating simulated datasets, and facilitating model comparison by evaluating predictive accuracy.

Definition and purpose

- Posterior predictive distributions form a crucial component of Bayesian statistics by combining observed data with prior beliefs to make future predictions

- These distributions play a pivotal role in model evaluation, forecasting, and decision-making within the Bayesian framework

Concept of posterior predictive

- Represents the distribution of unobserved data points conditioned on the observed data and model parameters

- Incorporates uncertainty in both parameter estimates and future observations

- Calculated by averaging the likelihood of new data over the posterior distribution of model parameters

- Provides a probabilistic framework for making predictions about future or unobserved data points

Role in Bayesian inference

- Serves as a key tool for assessing model fit and predictive performance in Bayesian analysis

- Enables researchers to generate simulated datasets for comparison with observed data

- Facilitates model comparison by evaluating the predictive accuracy of different models

- Allows for the incorporation of prior knowledge and uncertainty in predictive tasks

Mathematical formulation

- Bayesian statistics relies heavily on probability theory and integration to derive posterior predictive distributions

- Understanding the mathematical foundations helps in interpreting and implementing these distributions effectively

Posterior predictive equation

- Defined as the probability distribution of new data (y_new) given the observed data (y)

- Expressed mathematically as

- Integrates the likelihood of new data over the posterior distribution of parameters

- Accounts for uncertainty in both the model parameters and future observations

Integration over parameter space

- Involves integrating over all possible values of the model parameters (θ)

- Often requires numerical methods due to the complexity of the integral

- Can be approximated using Monte Carlo methods or other sampling techniques

- Allows for the marginalization of parameter uncertainty in predictions

Relationship to other distributions

- Posterior predictive distributions are closely related to other key distributions in Bayesian statistics

- Understanding these relationships helps in interpreting and utilizing posterior predictive distributions effectively

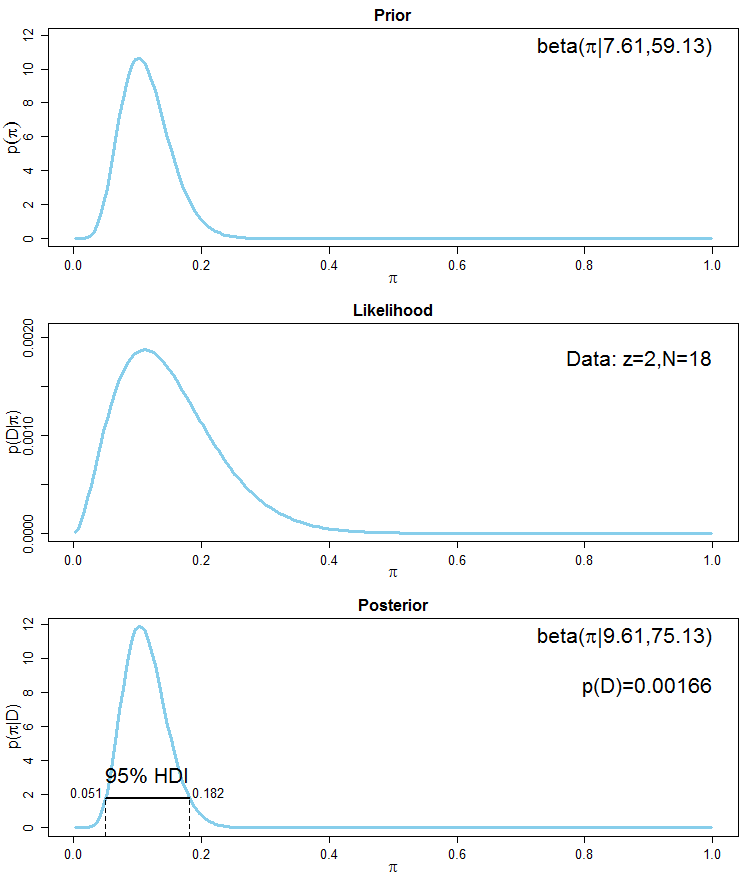

Prior vs posterior predictive

- Prior predictive distribution represents predictions before observing any data

- Calculated by integrating the likelihood over the prior distribution of parameters

- Posterior predictive incorporates information from observed data, leading to more refined predictions

- Comparison between prior and posterior predictive distributions can reveal the impact of data on predictions

Likelihood vs posterior predictive

- Likelihood represents the probability of observing the data given fixed parameter values

- Posterior predictive accounts for parameter uncertainty by averaging over the posterior distribution

- Likelihood focuses on model fit to observed data, while posterior predictive emphasizes predictive performance

- Posterior predictive distribution typically has wider uncertainty bounds compared to the likelihood

Computation methods

- Calculating posterior predictive distributions often involves complex integrals that require numerical approximation

- Various computational techniques have been developed to efficiently estimate these distributions

Monte Carlo sampling

- Involves drawing samples from the posterior distribution of parameters

- Generates predicted data points for each sampled parameter set

- Approximates the posterior predictive distribution through the empirical distribution of simulated data

- Provides a flexible approach for handling complex models and non-standard distributions

Markov Chain Monte Carlo

- Utilizes MCMC algorithms (Metropolis-Hastings, Gibbs sampling) to sample from the posterior distribution

- Generates a chain of parameter values that converge to the target posterior distribution

- Allows for efficient sampling in high-dimensional parameter spaces

- Facilitates the computation of posterior predictive distributions for complex hierarchical models

Applications in model checking

- Posterior predictive distributions serve as powerful tools for assessing model adequacy and fit

- These methods help identify discrepancies between observed data and model predictions

Posterior predictive p-values

- Quantify the discrepancy between observed data and posterior predictive simulations

- Calculated by comparing a test statistic for observed data to its distribution under the posterior predictive

- Values close to 0 or 1 indicate poor model fit or systematic discrepancies

- Provide a Bayesian alternative to classical goodness-of-fit tests

Graphical posterior predictive checks

- Involve visual comparisons between observed data and simulated datasets from the posterior predictive

- Include techniques such as posterior predictive density plots, scatter plots, and residual plots

- Help identify specific aspects of the data that are not well-captured by the model

- Facilitate the detection of outliers, heteroscedasticity, or other model inadequacies

Interpretation of results

- Proper interpretation of posterior predictive distributions is crucial for making informed decisions and drawing valid conclusions

- These distributions provide rich information about future observations and model performance

Uncertainty quantification

- Posterior predictive distributions capture both parameter uncertainty and inherent randomness in future observations

- Width of the distribution reflects the overall predictive uncertainty

- Allows for probabilistic statements about future outcomes (80% of future observations will fall within this range)

- Helps in assessing the reliability and precision of predictions

Predictive intervals

- Derived from the posterior predictive distribution to provide a range of plausible future values

- Typically reported as credible intervals (95% credible interval)

- Account for both parameter uncertainty and variability in future observations

- Useful for decision-making and risk assessment in various applications (financial forecasting, climate predictions)

Limitations and considerations

- While posterior predictive distributions are powerful tools, they come with certain limitations and challenges

- Understanding these issues is crucial for proper application and interpretation of results

Sensitivity to prior choice

- Posterior predictive distributions can be influenced by the choice of prior distributions

- Weak or uninformative priors may lead to overly wide predictive intervals

- Strong priors can dominate the data, potentially biasing predictions

- Requires careful consideration and sensitivity analysis to assess the impact of prior choices

Computational challenges

- Calculating posterior predictive distributions can be computationally intensive, especially for complex models

- May require large numbers of MCMC samples to achieve stable estimates

- High-dimensional parameter spaces can lead to slow convergence and mixing of MCMC chains

- Approximation methods (variational inference) may be necessary for very large datasets or complex models

Extensions and variations

- Posterior predictive distributions have been extended and adapted to handle various complex modeling scenarios

- These extensions enhance the flexibility and applicability of posterior predictive methods

Hierarchical posterior predictive

- Extends the concept to multilevel or hierarchical Bayesian models

- Accounts for multiple sources of variation and dependencies in the data

- Allows for predictions at different levels of the hierarchy (individual, group, population)

- Useful in fields such as ecology, epidemiology, and social sciences where data have nested structures

Cross-validation with posterior predictive

- Combines posterior predictive distributions with cross-validation techniques

- Used for model comparison and assessment of out-of-sample predictive performance

- Includes methods such as leave-one-out cross-validation (LOO-CV) and K-fold cross-validation

- Provides more robust estimates of model generalizability compared to single-sample posterior predictive checks

Software implementation

- Various software packages and libraries have been developed to facilitate the computation and visualization of posterior predictive distributions

- These tools make it easier for researchers and practitioners to apply posterior predictive methods in their analyses

R packages for posterior predictive

bayesplotpackage provides functions for posterior predictive checks and visualizationsrstanarmandbrmsoffer convenient interfaces for fitting Bayesian models and generating posterior predictive distributionsloopackage implements efficient approximate leave-one-out cross-validation for Bayesian modelscodapackage provides diagnostic tools for assessing MCMC convergence and posterior summaries

Python libraries for posterior predictive

PyMC3offers a probabilistic programming framework with built-in posterior predictive sampling capabilitiesArviZprovides tools for exploratory analysis of Bayesian models, including posterior predictive checksPyStanallows users to fit Stan models in Python and generate posterior predictive samplesTensorflow Probabilityincludes functionality for posterior predictive inference within deep probabilistic models

Case studies

- Examining real-world applications of posterior predictive distributions helps illustrate their practical utility and interpretation

- These case studies demonstrate how posterior predictive methods are applied in different domains

Posterior predictive in regression

- Used to assess the fit of Bayesian regression models and generate predictions for new data points

- Allows for the incorporation of uncertainty in both parameter estimates and residual variance

- Facilitates the detection of outliers, heteroscedasticity, or non-linear relationships

- Provides probabilistic forecasts that account for all sources of uncertainty in the model

Posterior predictive for time series

- Applied to evaluate and forecast time series models in fields such as finance and economics

- Enables the generation of probabilistic forecasts that account for parameter uncertainty and future shocks

- Helps in detecting model misspecification, such as autocorrelation in residuals or regime changes

- Allows for the comparison of different time series models based on their predictive performance