Banks are financial institutions that accept deposits and make loans. They also serve as intermediary bodies that help the Federal Reserve control the money supply. In our banks, we use a system known as fractional reserve banking.

Fractional Reserve Banking

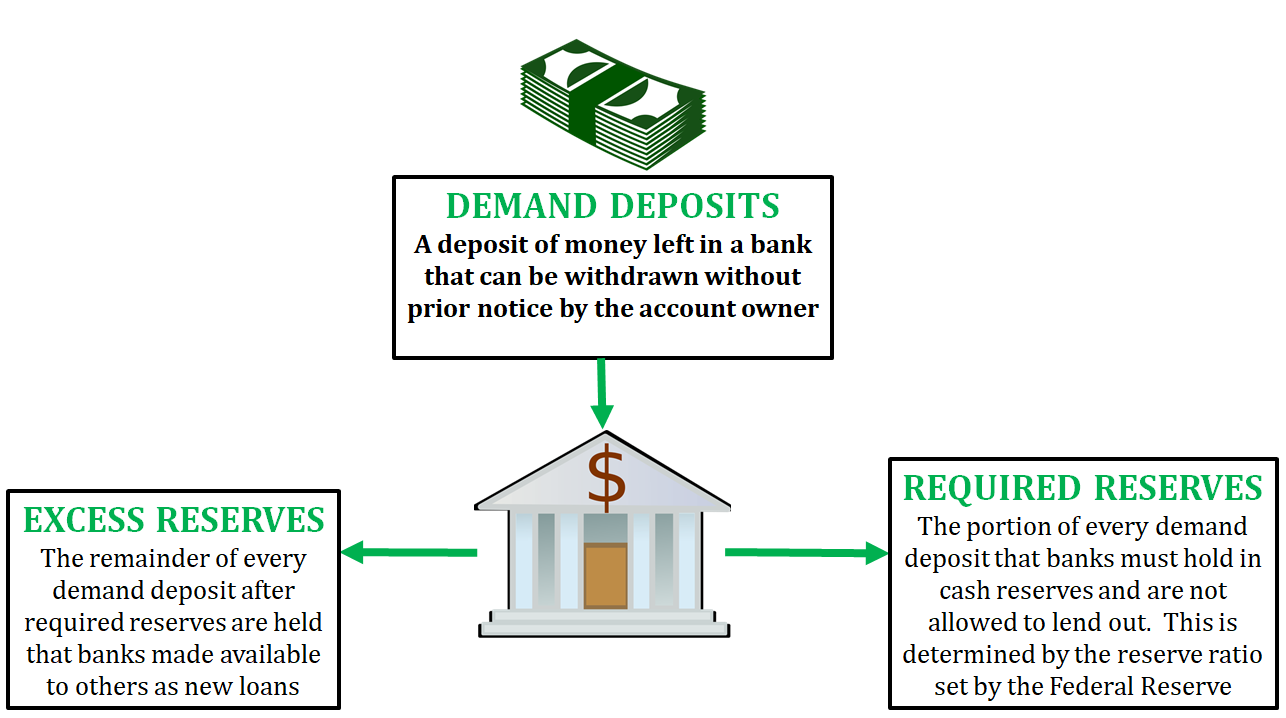

Fractional Reserve Banking is the practice by which a bank accepts deposits and is required to hold only a fraction of its deposits in cash reserves. The amount that the bank has to keep as cash reserves is determined by the reserve ratio (i.e. reserve requirement) that is set by the Federal Reserve. This allows the bank to loan out the remainder of the deposit to borrowers. By loaning out this money the bank creates "new" money in the economy. There are several terms involved in the process of fractional reserve banking.

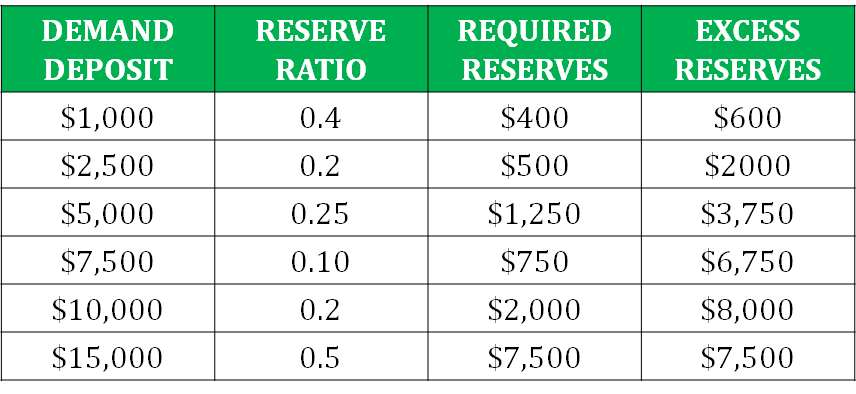

Let's look at how fractional reserve banking operates. In the table below you will see various amounts of demand deposits and a designated reserve ratio. Using that reserve ratio (i.e. reserve requirement), we are able to determine how much needs to be kept in reserves and how much is excess reserves that a bank can loan out.

Money Multiplier

When demand deposits are made, the banks have a portion of excess reserves that are created by the fractional reserve banking system. These excess reserves become new loans and set off a chain reaction of money creation throughout the entire economy. To see how much money is created through this process, we use what is called the money multiplier.

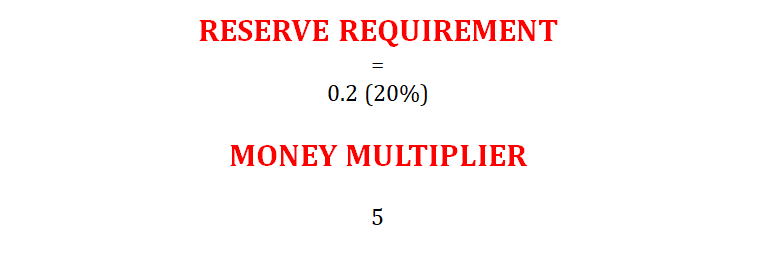

The money multiplier is the amount of money that banks generate with each dollar of excess reserves. The formula for the money multiplier is calculated by dividing the number 1 by the reserve ratio (i.e. reserve requirement).

So, if the reserve ratio (i.e. reserve requirement) is 0.2, the money multiplier is 1/0.2, which equals 5. When we take the money multiplier and multiply by the amount of money that goes out through new loans, we are able to determine how much is added to the money supply. So if $8,000 is in excess reserves, the bank loans out all this money, and the money multiplier is 5, we have $40,000 added to the money supply ($8,000 x 5 = $40,000).

If the reserve ratio (i.e. reserve requirement) is higher, the money multiplier is weaker, and there will be less change to the money supply. If the reserve ratio (i.e. reserve requirement) is lower, the money multiplier is stronger, and there will be more change to the money supply.

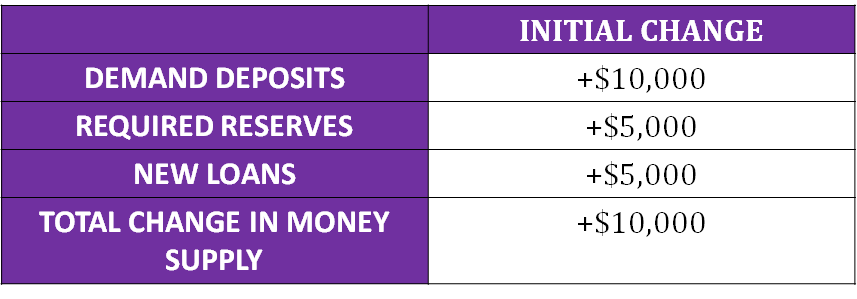

When we are using this process, there are several concepts we are asked to calculate. Typically, when we are given an amount of a demand deposit, the first thing we calculate is how much of this demand deposit is required reserves, and then we calculate the excess reserves. Once we have the number of excess reserves, we can calculate the change in the money supply.

Let's look at two different examples with the same amount of a demand deposit but different reserve ratios (i.e. reserve requirement).

Example One: For this example, the reserve ratio (i.e. reserve requirement) is 20% or 0.2, which makes the money multiplier 5 (1/0.2).

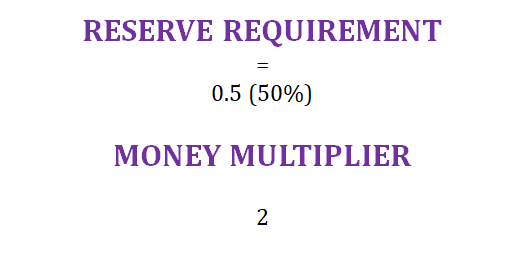

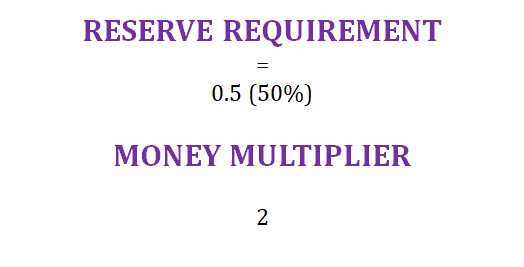

Example Two: For this example, the reserve ratio (i.e. reserve requirement) is 50% or 0.5, which makes the money multiplier 2 (1/0.5).

From these two examples, we can see that the money supply changes more when the reserve ratio (i.e. reserve requirement) is lower than when it is higher.

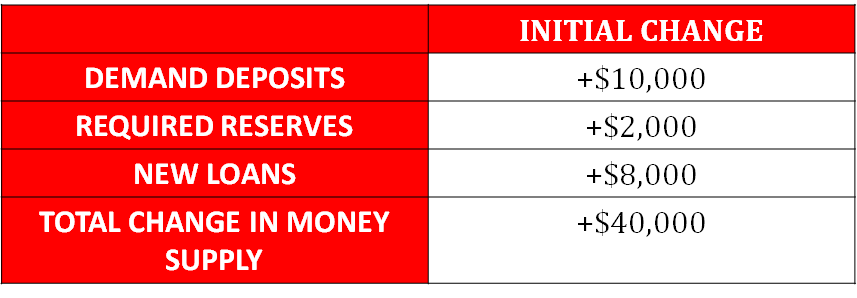

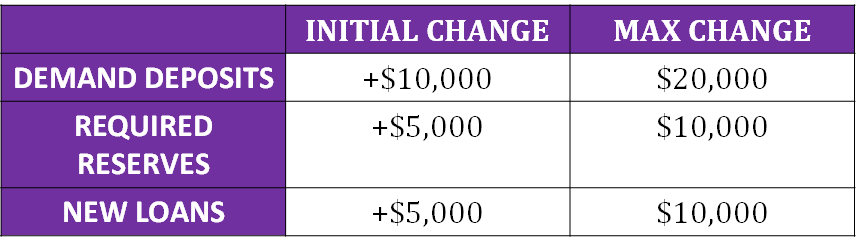

The money multiplier can also be used to determine the total change in required reserves, new loans, and demand deposits throughout the entire banking system. To find the maximum change in any of these terms, we simply multiply the initial change by the money multiplier. Look at the table below to see some examples using a reserve requirement of 0.5 and a money multiplier of 2.

Bank Balance Sheets

Bank balance sheets (i.e. T-accounts) are a visual record of the fractional reserve banking within a bank. These ledgers show the assets and liabilities within a bank. They can show how a bank uses any deposits and available funds to create reserves and new loans for the purpose of lending. They are called bank balance sheets because the liabilities and assets must be equal to each other.

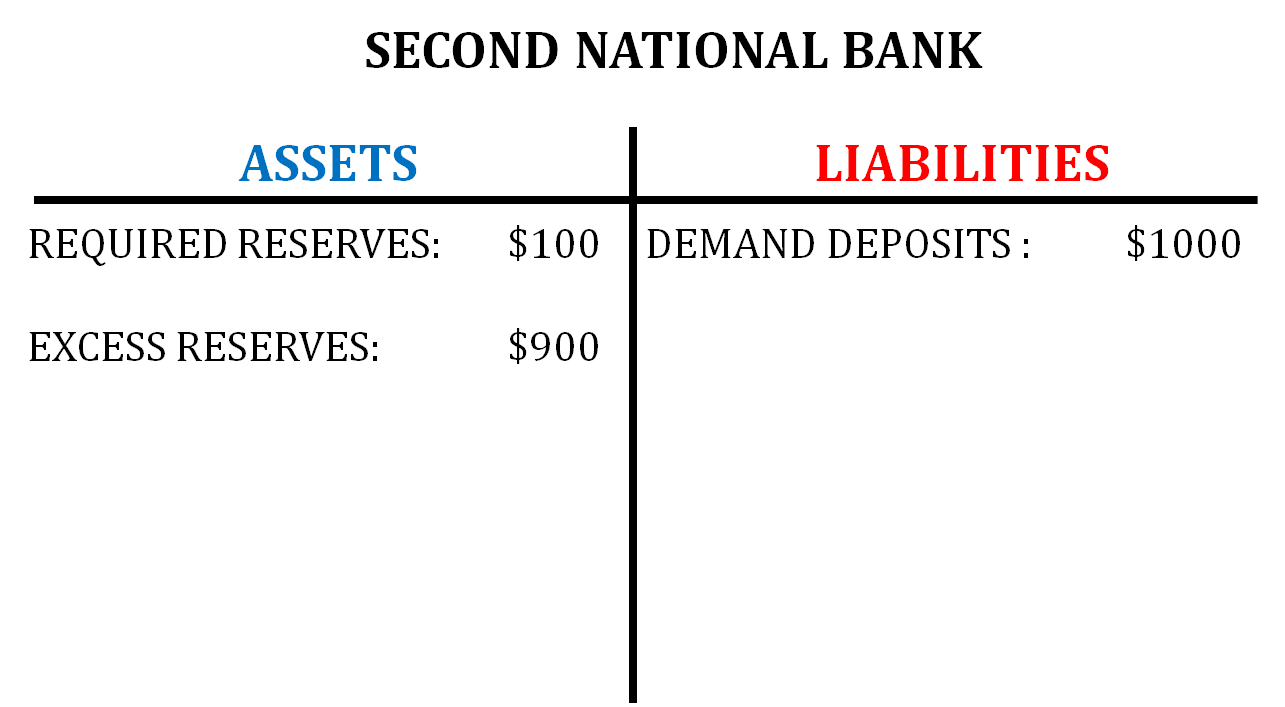

In the banking industry, liabilities are the financial obligations that a bank must pay to a consumer, and they must be repaid when requested. Liabilities include demand deposits, account investments, and equity. Assets are the possessions that are owned by or credited to a bank that can be collected or liquefied into cash. Assets include both required and excess reserves, outstanding loans, and securities.Here is a sample bank balance sheet for the Second National Bank that has a reserve ratio of 10% or 0.1. This means that the money multiplier will be 10. We are going to assume that they will loan out all of their excess reserves.

You can see that this particular bank received a demand deposit of $1000, so 10% of that deposit has to be kept as required reserves. In this case, the required reserves are $100. That leaves $900 of the demand deposit that is considered excess reserves and can be loaned out. Since we said that the bank will loan out all of their excess reserves, we know that $900 will go out into the money supply and will create a maximum change in the money supply of $9,000 ($900 x 10).

Practice Free Response Question (FRQ) - 2016 # 2

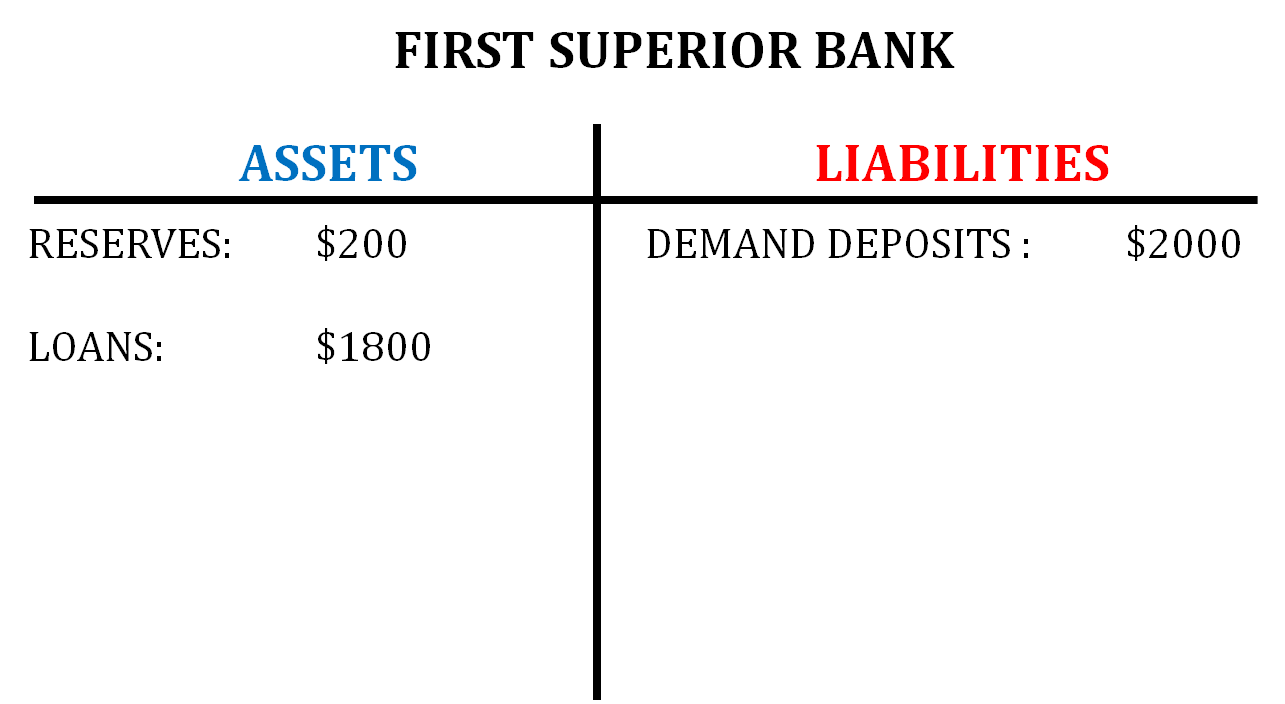

The bank balance sheet above is for the First Superior Bank.

Assume that the required reserve ratio is 10 percent.

- (a) What is the dollar value of new loans that First Superior Bank can make? Explain.

- (b) Mr. Smith deposits $100 of cash in a demand deposit account in First Superior Bank. Calculate the maximum amount of new loans that First Superior Bank can now make.

(c) As a result of Mr. Smith's $100 cash deposit, calculate the maximum change over time in each of the following in the banking system.

- (i) Loans

- (ii) Demand deposits

- (d) As a result of Mr. Smith's $100 cash deposit, calculate the maximum change over time in the money supply.

- (e) Provide one reason why the actual change in the money supply can be smaller than the maximum change you identified in part (d).

Answers

a)

The amount of new loans is zero because the bank has no excess reserves because the bank has loaned all the excess reserves out.

b) The maximum amount of new loans that can be made are $90 ($10 will be the required reserves because that is 10% of 100 and $90 will go into excess reserves and be loaned out)

c)

i. The maximum change over time in loans in the banking system is $900 ($90 x 10 (which is the money multiplier)) ii. The maximum change over time in demand deposits in the banking system is $1000 ($100 x 10 (which is the money multiplier))

d) The maximum change over time in the money supply is $900 ($90 x 10)

e) the money supply can be smaller than the maximum change identified in part d when the public holds more money and/or banks hold more excess reserves.

Vocabulary

The following words are mentioned explicitly in the College Board Course and Exam Description for this topic.

| Term | Definition |

|---|---|

| balance sheets | Financial statements that show a bank's assets, liabilities, and equity at a specific point in time, used to analyze the effects of banking system changes. |

| bank reserves | Money held by banks that is not loaned out, including reserves required by the Federal Reserve and excess reserves. |

| banking system | The network of financial institutions, including commercial banks and central banks, that facilitate the creation and circulation of money in an economy. |

| depository institutions | Financial institutions such as commercial banks that accept deposits from the public and use those funds to make loans. |

| excess reserves | Reserves held by banks beyond the required minimum, which can be loaned out to expand the money supply. |

| fractional reserve banking | A banking system in which depository institutions hold only a fraction of their deposits in reserve and lend out the remainder. |

| monetary base | The total amount of money created by a central bank, consisting of currency in circulation and bank reserves. |

| money multiplier | The factor by which the money supply increases relative to an increase in the monetary base through the lending activities of commercial banks. |

| money supply | The total amount of money available in an economy at a given time, including currency in circulation and deposits in financial institutions. |

| money supply expansion | The process by which the banking system increases the total amount of money in circulation through lending based on excess reserves. |

| required reserve ratio | The percentage of deposits that commercial banks are required to hold in reserve rather than lend out, used as a monetary policy tool. |

| required reserves | The minimum amount of reserves that depository institutions are legally required to hold, determined by the required reserve ratio. |

Frequently Asked Questions

What is fractional reserve banking and how does it actually work?

Fractional reserve banking is the system where commercial banks keep only a fraction of deposits as reserves (required reserves) and lend out the rest (excess reserves). Example: with a 10% reserve requirement, a $1,000 deposit requires $100 held as reserves and $900 can be lent. When that $900 is spent and redeposited, banks can lend 90% of it again, creating new checkable-deposit money. The simple money multiplier = 1 / reserve ratio (so max multiplier = 1/0.10 = 10). That multiplier shows the maximum possible expansion of the money supply from a given monetary base. Real-world limits: banks may hold excess reserves and people may hold currency (currency drain), so actual expansion is smaller. On the AP exam you should know bank balance-sheet basics (assets = loans + reserves; liabilities = deposits), reserve requirement vs. excess reserves, and use the multiplier to calculate maximum deposit expansion. For a focused review, see the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and try practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

How do banks create money when they make loans - I'm so confused about this?

Banks create money through fractional-reserve banking. When you deposit $1,000, the bank keeps required reserves (say 10% = $100) and can loan out the excess reserves ($900). That $900 loan gets spent and redeposited at some bank, which keeps 10% ($90) and loans $810, and so on. Each round creates new checkable deposits, expanding the money supply beyond the original $1,000. The simple money multiplier shows the maximum expansion: 1 / required reserve ratio (so with a 10% RR, multiplier = 1/0.10 = 10). Maximum money supply change = initial new reserves × multiplier. Remember this is a maximum—banks may hold excess reserves and people may hold currency, which reduce the actual multiplier (CED EK POL-2.A.2–A.8). This is a common AP free-response/calculation topic, so practice balance-sheet steps and the multiplier. For a focused review, check the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and run practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

What's the difference between required reserves and excess reserves?

Required reserves are the portion of a bank’s reserves it must hold and not lend out—set by the central bank as the reserve requirement (a percent of checkable deposits). Calculate them as: required reserves = reserve ratio × deposits. Excess reserves are any reserves the bank holds above that required amount: excess reserves = actual reserves − required reserves. Why it matters: under fractional-reserve banking banks lend out their excess reserves, creating new deposits and expanding the money supply. The maximum potential expansion depends on the money multiplier, which in the simple model is 1 / required reserve ratio (so if rr = 10%, multiplier = 10). On the AP exam you may be asked to compute required/excess reserves from balance sheets and to show how changes in reserves or the reserve ratio affect money supply (Topic 4.4). For a focused review, check the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

How do I calculate the money multiplier using the required reserve ratio?

Money multiplier (simple model) = reciprocal of the required reserve ratio. That is: money multiplier (mm) = 1 / required reserve ratio (rr) Example: if rr = 0.10 (10%), mm = 1 / 0.10 = 10. So a $1,000 new deposit could expand the money supply by up to $1,000 × 10 = $10,000 (assuming banks lend all excess reserves and the public holds no extra currency). Keep in mind AP CED cautions: the simple multiplier is a maximum (EK POL-2.A.7). The actual multiplier is smaller if banks hold excess reserves or people keep more currency (EK POL-2.A.4, A.8). The multiplier is also defined as the ratio of the money supply to the monetary base (EK POL-2.A.5), so on FRQ you should show the formula and any assumptions you’re making. For more review, see the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and Unit 4 overview (https://library.fiveable.me/ap-macroeconomics/unit-4). Practice problems: (https://library.fiveable.me/practice/ap-macroeconomics).

Can someone explain bank balance sheets in simple terms - assets vs liabilities?

Think of a bank balance sheet like a snapshot: assets on the left (what the bank owns or is owed) and liabilities on the right (what the bank owes to others). Key items you’ll see on AP Macro balance sheets: - Assets: reserves (cash at the bank + deposits at the Fed), loans the bank made (borrowers owe the bank), and securities. Reserves = required reserves + excess reserves. - Liabilities: customer checkable deposits (what the bank owes depositors) and other borrowings. - Net worth (owners’ equity): Assets − Liabilities (bank’s capital). Why it matters for Topic 4.4: fractional reserve banking means banks keep only required reserves and lend the rest. Excess reserves allow banks to create new deposits (expand the money supply). Use the money multiplier = 1 / required reserve ratio to find the maximum potential deposit expansion (but remember the CED warns this is an upper bound—banks may hold excess reserves and people may hold cash). The AP exam expects you to read balance sheets and do numerical calculations (see Practice/Manipulation skills). For more review, check the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY), the Unit 4 overview (https://library.fiveable.me/ap-macroeconomics/unit-4), and practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

Why doesn't the money multiplier formula always predict the right amount of money creation?

The simple money multiplier (ΔM = money multiplier × Δmonetary base, where max multiplier = 1/rr) gives a “maximum” potential change in deposits, not the actual change. It overstates money creation because it assumes no leakages and that banks loan out all excess reserves. In reality: (1) the public holds currency (currency drain), so some of the base stays as cash instead of deposits; (2) banks often hold excess reserves above the required reserve ratio (especially when loan demand or risk is low); and (3) changes in behavior or Fed tools (like paying interest on reserves) alter reserves-to-deposits and the currency-deposit ratio. Those factors change the effective multiplier (depends on reserve ratio, excess reserves, and currency holdings), so actual deposit expansion is smaller than 1/rr predicts (CED EK POL-2.A.7 and EK POL-2.A.8). For more review, see the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and extra practice (https://library.fiveable.me/practice/ap-macroeconomics).

What happens to the money supply when people hold more cash instead of depositing it?

When people hold more cash instead of depositing it, the money supply shrinks. In fractional-reserve banking banks create deposits (and thus money) by lending out their excess reserves. If people keep currency (a “currency drain”), banks get fewer deposits, so reserves fall → fewer excess reserves → fewer loans. That lowers the money multiplier (simple max = 1/required reserve ratio) and so the total deposit expansion is smaller than it would be otherwise. On the AP exam you might see this as a balance-sheet or money-multiplier calculation—be ready to show how a rise in currency holdings reduces deposits and multiplies less. For a refresher, check the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and try practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

How do I solve money multiplier problems step by step for the AP exam?

Step-by-step for AP-style money-multiplier problems (show your work—the FRQ rubric requires it): 1. Identify the required reserve ratio (rr). If not given, use the required reserve percentage. 2. Find the simple money multiplier: multiplier = 1 / rr. (This is the maximum possible multiplier—EK POL-2.A.7.) 3. If you’re given an initial deposit or excess reserves, use: maximum deposit expansion = initial deposit × multiplier (or excess reserves × multiplier if excess reserves are the source). 4. If the problem includes currency drain or banks holding excess reserves, compute the effective reserve ratio: effective rr = required rr + currency-to-deposit ratio + banks’ desired excess-reserve ratio. Then use multiplier = 1 / effective rr. (Explains why EK POL-2.A.8 warns the simple multiplier can overstate expansion.) 5. For balance-sheet problems: calculate required reserves = rr × deposits, excess reserves = actual reserves − required reserves, then apply multiplier to excess reserves. Example: rr = 10% → multiplier = 10. A $1,000 excess reserve → potential deposit expansion = $1,000 × 10 = $10,000. Practice these on the Unit 4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and run more problems at (https://library.fiveable.me/practice/ap-macroeconomics).

I don't understand how one bank deposit can create multiple loans - help?

Think of one deposit as the start of a chain because banks use fractional reserve banking: they keep required reserves and can lend out the rest (excess reserves). Example: deposit $1,000, required reserve ratio (RR) = 10%. Bank holds $100 as required reserves and can lend $900. That $900 will be spent and redeposited in other banks; those banks keep 10% ($90) and lend $810, and so on. The series of new deposits is $1,000 + $900 + $810 + ... which sums to a maximum of $1,000 × (1 / RR) = $10,000 when RR = 10% (money multiplier = 1/0.10 = 10). Key limits: this is the maximum—if people hold currency instead of redepositing or banks keep extra reserves, expansion is smaller. For AP exam questions you’ll often calculate required reserves, excess reserves, and use the simple money multiplier; practice those on the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and more problems at the Unit 4 page (https://library.fiveable.me/ap-macroeconomics/unit-4) or the practice bank (https://library.fiveable.me/practice/ap-macroeconomics).

What's the maximum money multiplier formula and when do I use it?

Maximum money multiplier = 1 / required reserve ratio (rr). Use it when you want the theoretical upper-bound on how much the banking system could expand deposits (and thus the money supply) from an initial deposit or change in reserves. Example: if rr = 0.10, maximum multiplier = 1/0.10 = 10, so $100 of excess reserves could create up to $1,000 of new deposits. On AP: you’ll use this for numerical analysis problems (CED EK POL-2.A.7)—e.g., calculate ΔM = (1/rr) × initial excess reserves or ΔM = (1/rr) × change in monetary base. Always note the limitation: the “simple” multiplier is a maximum—it overstates real expansion if banks hold excess reserves or the public holds currency (EK POL-2.A.8). For extra practice and worked examples, see the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and lots of practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

Why do banks sometimes hold excess reserves instead of lending them out?

Banks hold excess reserves for safety and policy reasons, not just because they forgot to lend. Under fractional-reserve banking banks must meet required reserves, but they may keep extra (excess reserves) to cover unexpected withdrawals, reduce liquidity risk, or because loan demand is weak. Other reasons: higher perceived credit risk, tighter capital rules, or because the Fed pays interest on reserves (IOER), making holding reserves relatively attractive. Practically, excess reserves limit deposit expansion—the simple money multiplier (1/required-reserve ratio, EK POL-2.A.7) shows the maximum expansion, but EK POL-2.A.8 warns the actual multiplier is smaller when banks hold excess reserves or people hold currency. On the AP exam, expect questions linking excess reserves to smaller money supply expansion and monetary policy effects (Unit 4). For a focused review, see the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

How does the Federal Reserve's required reserve ratio affect money creation?

The required reserve ratio (rr) sets how much of deposits banks must hold as required reserves and so directly controls how much they can lend. The simple money multiplier = 1/rr, so a lower rr → bigger multiplier → more potential deposit expansion; a higher rr → smaller multiplier → less expansion. Example: if rr = 0.10, multiplier = 1/0.10 = 10, so $1,000 of new reserves could support up to $10,000 in deposits in the best-case fractional reserve model. Remember the CED points: required vs. excess reserves (EK POL-2.A.3, EK POL-2.A.4) and that the simple multiplier (EK POL-2.A.7) gives a maximum—real expansion is smaller if banks hold excess reserves or the public keeps currency (currency drain) (EK POL-2.A.8). For AP practice, you’ll be asked to calculate multipliers and deposit expansion—see the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and more Unit 4 resources (https://library.fiveable.me/ap-macroeconomics/unit-4). More practice problems are at (https://library.fiveable.me/practice/ap-macroeconomics).

What's the difference between the monetary base and the money supply?

The monetary base (also called high-powered money) is the sum of currency in circulation plus banks’ reserves at the central bank—it’s what the Fed directly controls. The money supply (M1/M2) is broader: it includes currency plus bank-created deposits (checkable deposits, savings, etc.). In fractional-reserve banking, banks hold required reserves and keep excess reserves; those excess reserves get lent out and create new deposits, expanding the money supply. The relationship is: Money Supply = Money Multiplier × Monetary Base, where the simple multiplier = 1 / required reserve ratio (but it’s reduced if banks hold excess reserves or the public holds more currency). You’ll see both definitions and multiplier calculations on AP Topic 4.4 items and FRQs (use EK POL-2.A.4–2.A.7 vocabulary). For a focused review and practice problems, check the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and the Unit 4 page (https://library.fiveable.me/ap-macroeconomics/unit-4). For extra practice, use the 1000+ practice questions (https://library.fiveable.me/practice/ap-macroeconomics).

Can you walk me through a complete example of how $1000 deposit expands through the banking system?

Put $1,000 in Bank A and assume a required reserve ratio (rr) of 10% (use whatever rr your problem gives). Walkthrough: - Bank A holds required reserves = $1,000 × 0.10 = $100 and can lend out $900 (excess reserves). - Borrower spends the $900; it gets deposited in Bank B. Bank B holds $90 (10%) and lends $810. - Bank C holds $81 and lends $729, and so on. This geometric loan/deposit chain sums to a maximum total increase in checkable deposits = initial deposit × money multiplier. Money multiplier = 1/rr = 1/0.10 = 10. So maximum expansion = $1,000 × 10 = $10,000 in deposits (that includes the original $1,000). The new loans created equal $9,000. AP note: on the exam you may be asked to show bank balance-sheet entries (reserves, deposits, loans) or compute the multiplier (CED EK POL-2.A.1–A.7). Real-world caveats: currency drain and banks holding excess reserves reduce actual expansion. For more practice and a topic review, see the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY) and extra problems (https://library.fiveable.me/practice/ap-macroeconomics).

When banks want to be more cautious and hold extra reserves, how does this affect the money multiplier calculation?

When banks decide to hold extra (excess) reserves, the money multiplier falls because less of each deposit is lent out. AP CED gives the basic max multiplier as 1/required reserve ratio (EK POL-2.A.7). That’s the “maximum” only when banks hold no excess reserves and the public holds no extra currency. More precisely, use the actual reserves-to-deposits ratio (required rr + excess rr; you can also add currency-to-deposits if needed). The effective multiplier ≈ 1 / (required reserve ratio + excess reserve ratio [+ currency drain]). So if rr = 10% and banks hold 5% excess reserves, multiplier ≈ 1 / 0.15 = 6.67 (vs. 10 if no excess reserves). This is why the simple multiplier can overstate expansion (EK POL-2.A.8, EK POL-2.A.4). For more practice and examples, check the Topic 4.4 study guide (https://library.fiveable.me/ap-macroeconomics/unit-4/banking-expansion-money-supply/study-guide/Qnns1418ZAHsaBWIaTbY), the Unit 4 overview (https://library.fiveable.me/ap-macroeconomics/unit-4), and lots of practice problems (https://library.fiveable.me/practice/ap-macroeconomics).