Numerical integration is a crucial tool in financial mathematics, approximating complex integrals when analytical solutions are elusive. It bridges theoretical models and practical applications, enabling the pricing of derivatives and estimation of risk measures in quantitative finance.

This topic covers various integration methods, from simple rectangular rules to advanced Monte Carlo techniques. We'll explore error analysis, applications in option pricing and risk management, and computational considerations, providing a comprehensive overview of numerical integration in finance.

Basics of numerical integration

- Numerical integration approximates definite integrals when analytical solutions are difficult or impossible to obtain

- Essential tool in financial mathematics for pricing complex derivatives and estimating risk measures

- Bridges the gap between theoretical models and practical applications in quantitative finance

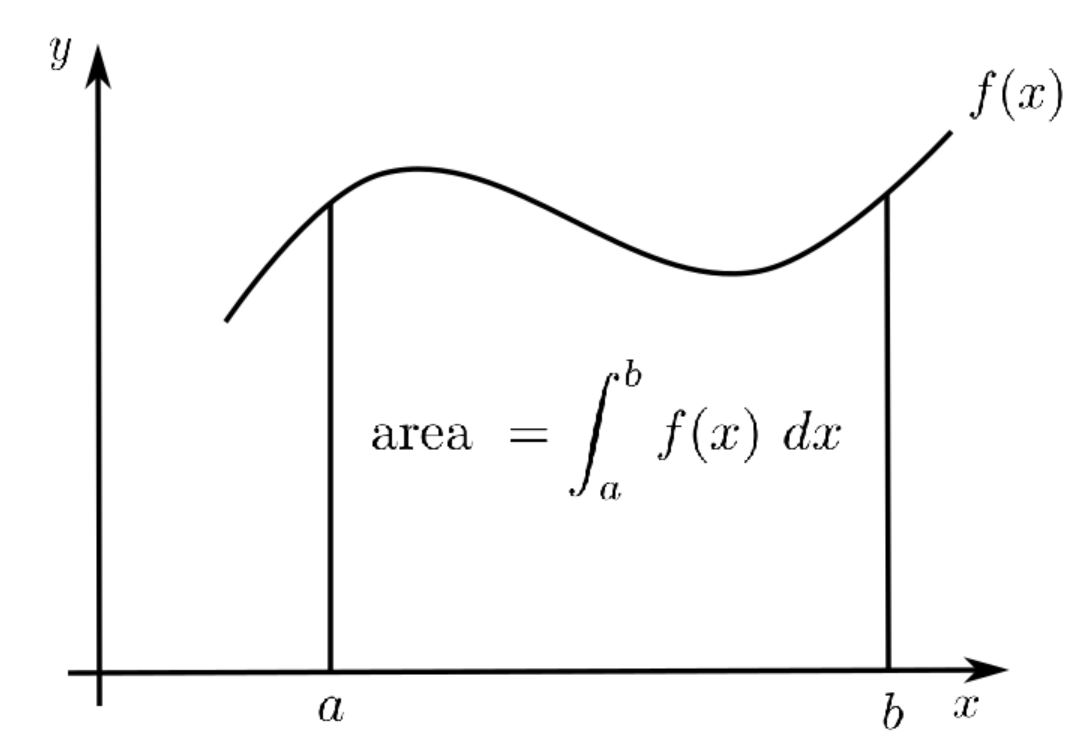

Definition and purpose

- Numerical integration calculates the approximate area under a curve using discrete data points

- Employed when integrand functions are complex or only known at specific points

- Enables evaluation of integrals that lack closed-form solutions in financial modeling

- Provides flexibility in handling various probability distributions and payoff structures

Continuous vs discrete data

- Continuous data represents uninterrupted measurements over a range (stock prices)

- Discrete data consists of distinct, separate values (daily closing prices)

- Numerical integration methods adapt to both data types through appropriate sampling

- Continuous functions often discretized for computational feasibility in financial applications

- Discrete data may require interpolation techniques to estimate intermediate values

Common integration methods

Rectangular rule

- Simplest numerical integration method approximating area with rectangles

- Left-point, right-point, and midpoint variations based on rectangle positioning

- Formula for left-point rectangular rule

- Accuracy improves with increased number of subintervals

- Often used for quick estimations in financial modeling (simple option pricing)

Trapezoidal rule

- Approximates area under curve using trapezoids instead of rectangles

- More accurate than rectangular rule for most functions

- Formula

- Widely used in finance for numerical integration tasks (yield curve calculations)

- Easily implemented in spreadsheets and programming languages

Simpson's rule

- Higher-order method using parabolic arcs to approximate curve

- Generally more accurate than rectangular and trapezoidal rules

- Formula

- Requires even number of subintervals for implementation

- Commonly applied in option pricing models and risk calculations

Error analysis

Sources of error

- Discretization error from approximating continuous functions with discrete points

- Truncation error due to finite precision arithmetic in computers

- Rounding errors accumulating over multiple calculations

- Method-specific errors (rectangular rule tends to overestimate concave functions)

- Input data errors propagating through integration process

Error estimation techniques

- Comparison of results using different integration methods

- Richardson extrapolation improves accuracy by combining results from different step sizes

- Adaptive quadrature methods adjust step size based on local error estimates

- Error bounds derivation using Taylor series expansions

- Monte Carlo simulations to assess error distribution in complex financial models

Applications in finance

Option pricing

- Numerical integration used in Black-Scholes model for European options

- Handles complex payoff structures in exotic options pricing

- Calculates risk-neutral expectations for various underlying asset distributions

- Enables pricing of options with no closed-form solutions (Asian options)

- Incorporates time-dependent parameters in option valuation models

Risk management

- Computes probability distributions of portfolio returns

- Calculates Value at Risk (VaR) through numerical integration of loss distributions

- Estimates Expected Shortfall (ES) for tail risk assessment

- Evaluates credit risk by integrating default probability curves

- Performs scenario analysis by integrating over multiple risk factor distributions

Advanced integration techniques

Monte Carlo integration

- Utilizes random sampling to approximate integrals in high-dimensional spaces

- Particularly useful for complex financial instruments (basket options)

- Convergence rate independent of dimensionality (√n)

- Enables simulation of various market scenarios for risk assessment

- Incorporates importance sampling techniques to improve efficiency in rare event simulations

Gaussian quadrature

- Approximates integrals using specially chosen abscissas and weights

- Achieves high accuracy with relatively few function evaluations

- Different variants (Gauss-Legendre, Gauss-Hermite) suited for specific types of integrands

- Applied in bond pricing models and interest rate derivatives valuation

- Efficiently handles integrals with singularities or infinite integration limits

Computational considerations

Efficiency vs accuracy

- Trade-off between computational speed and precision in numerical integration

- Higher-order methods (Simpson's rule) generally more accurate but computationally intensive

- Adaptive methods balance efficiency and accuracy by focusing on regions of high variability

- Parallel computing techniques improve efficiency for high-dimensional integrals

- GPU acceleration enhances performance in Monte Carlo integration for large-scale simulations

Software implementations

- Built-in functions in financial software packages (MATLAB, R, Python libraries)

- Custom implementations in low-level languages (C++) for performance-critical applications

- Specialized quadrature libraries (GNU Scientific Library) for advanced integration techniques

- Cloud-based solutions for distributed computing in large-scale financial simulations

- Automated code generation tools for optimized integration routines in quantitative finance

Numerical integration vs analytical methods

Advantages and limitations

- Numerical methods handle complex integrands without closed-form solutions

- Analytical solutions provide exact results but are limited to specific function classes

- Numerical integration more flexible for incorporating empirical data and complex models

- Analytical methods offer insights into parameter sensitivities and limiting behaviors

- Numerical approaches may introduce errors and instabilities in certain scenarios

Choosing appropriate approach

- Consider problem complexity, required accuracy, and computational resources

- Analytical methods preferred for simple, well-behaved functions with known primitives

- Numerical integration suitable for complex financial models with multiple factors

- Hybrid approaches combine analytical and numerical methods for optimal performance

- Sensitivity analysis helps determine impact of integration method on final results

Multi-dimensional integration

Challenges in higher dimensions

- Curse of dimensionality increases computational complexity exponentially

- Difficulty in visualizing and interpreting high-dimensional integrals

- Increased susceptibility to numerical instabilities and error propagation

- Sparse grids techniques reduce computational burden in certain cases

- Dimension reduction methods (principal component analysis) simplify integration task

Adaptive integration methods

- Dynamically adjust integration points based on function behavior

- Concentrate computational effort in regions of high variability or importance

- Cuhre algorithm efficiently handles moderate-dimensional integrals (up to 15 dimensions)

- Adaptive Monte Carlo methods (MISER, VEGAS) effective for high-dimensional problems

- Quasi-Monte Carlo sequences improve convergence in multi-dimensional integration

Numerical integration in derivatives pricing

Black-Scholes model application

- Numerical integration calculates option prices for non-standard payoffs

- Handles time-dependent volatility and interest rate scenarios

- Enables pricing of exotic options (barrier options, lookback options)

- Incorporates dividend payments and other cash flows in equity option valuation

- Facilitates sensitivity analysis (Greeks) through numerical differentiation of integrals

Exotic options valuation

- Path-dependent options (Asian options) priced using multi-dimensional integration

- Basket options evaluated through high-dimensional numerical integration techniques

- Quanto options pricing incorporates correlation between asset and exchange rate

- Numerical integration handles complex exercise conditions in American-style options

- Enables valuation of options with non-standard underlying asset distributions

Integration in time series analysis

Cumulative returns calculation

- Numerical integration computes area under return curve over time

- Handles both discrete (daily returns) and continuous (log returns) data

- Enables comparison of investment performance across different time periods

- Incorporates reinvestment assumptions in total return calculations

- Facilitates risk-adjusted return measures (Sharpe ratio, Sortino ratio) computation

Volatility estimation

- Integrated volatility calculated through numerical integration of squared returns

- Handles intraday data for high-frequency volatility estimation

- Enables construction of volatility term structure in options markets

- Incorporates jump processes in volatility modeling through appropriate integration techniques

- Facilitates realized volatility calculations in risk management applications

Practical implementation

Excel for numerical integration

- Built-in functions (SUMPRODUCT) implement basic numerical integration methods

- VBA macros enable custom integration routines for complex financial models

- Data Tables feature allows sensitivity analysis of integration parameters

- Solver add-in optimizes integration parameters in calibration exercises

- Charting capabilities visualize integrand functions and approximation errors

Programming languages comparison

- Python offers NumPy and SciPy libraries with efficient numerical integration routines

- R provides extensive statistical packages with built-in integration functions

- MATLAB excels in matrix operations, beneficial for multi-dimensional integration

- C++ enables low-level optimizations for performance-critical integration tasks

- Julia combines ease of use with high performance for numerical integration in finance