Annuity Definition and Types

An annuity is a series of equal payments made at regular intervals over a specified period. In financial accounting, annuities show up constantly: loan repayments, lease payments, pension obligations, and bond coupon streams are all annuities. Getting comfortable with annuity math is essential because it drives how businesses measure and report these obligations.

The two distinctions you need to know are when payments occur and whether the end date is fixed.

Ordinary vs. Due Annuities

Ordinary annuity: payments occur at the end of each period. Most loans and bond coupon payments work this way. If you take out a car loan, your first payment is due one period from now, not today.

Annuity due: payments occur at the beginning of each period. Rent and insurance premiums are classic examples. Your landlord expects payment at the start of the month, not the end.

This timing difference matters because annuity due payments are each one period closer to the present. That means an annuity due always has a higher present value and a higher future value than an otherwise identical ordinary annuity, by a factor of .

Annuities Certain vs. Contingent

- Annuities certain have a predetermined number of payments and a fixed end date (e.g., a 5-year loan with 60 monthly payments).

- Contingent annuities depend on an uncertain event, such as the death of the annuitant. Life insurance payouts and certain pension arrangements fall into this category.

- Contingent annuities require actuarial assumptions to estimate their value, so they're more complex. For this course, most problems involve annuities certain.

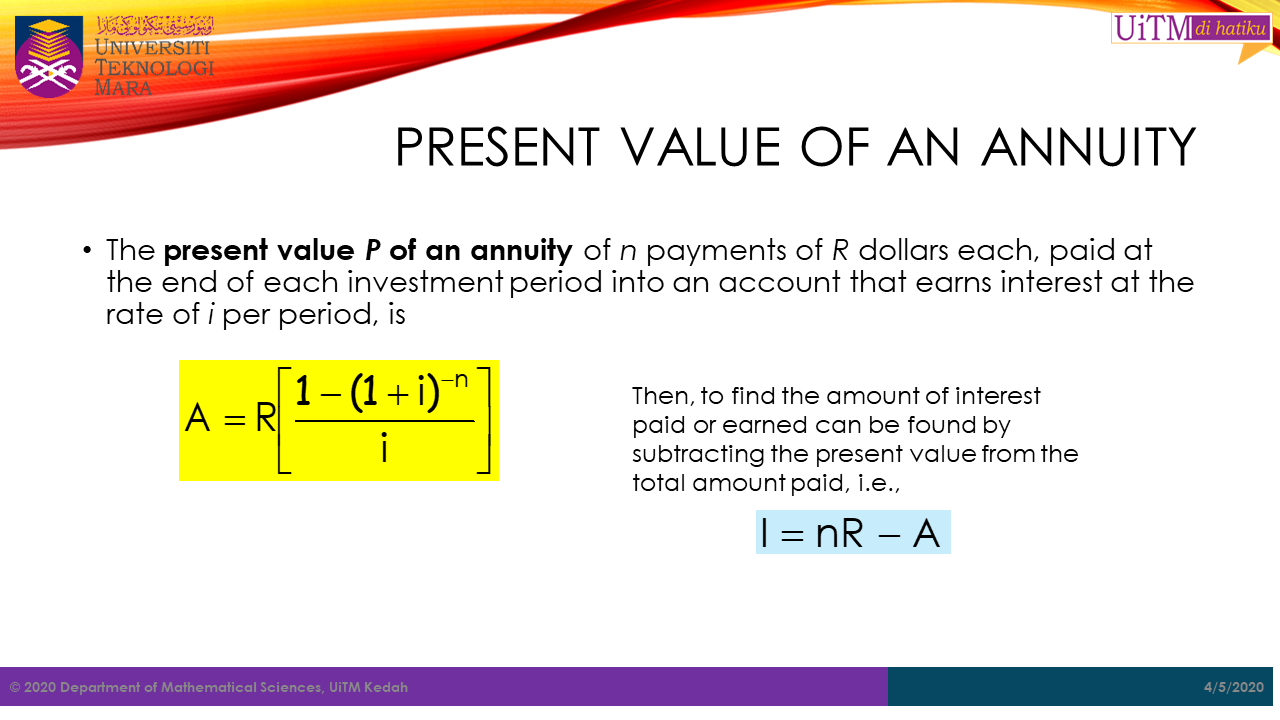

Present Value of Annuities

The present value (PV) of an annuity answers: What is a stream of future payments worth right now? You need this whenever you're recording a liability for a loan, pricing a bond, or evaluating a lease.

Derivation of Present Value Formula

The PV of an annuity is just the sum of each individual payment discounted back to today. Rather than discounting each payment separately (which works but is tedious), the geometric series simplifies to:

Where:

- = payment amount per period

- = interest rate per period

- = number of periods

The fraction is called the present value annuity factor. You'll often see it in tables or abbreviated as .

Present Value of Ordinary Annuities

For an ordinary annuity, apply the formula directly. The first payment is discounted for one full period because it arrives at the end of period 1.

Example: You'll receive $5,000 at the end of each year for 4 years. The discount rate is 6%.

Present Value of Annuities Due

Because each payment occurs one period earlier, multiply the ordinary annuity PV by :

Using the same example but with payments at the beginning of each year:

The annuity due is worth more because you receive each payment sooner.

Future Value of Annuities

The future value (FV) of an annuity answers: How much will all these payments be worth at the end, after compounding? This is useful for savings plans, sinking funds, and any situation where you're accumulating money over time.

Derivation of Future Value Formula

Sum the future values of each individual payment compounded forward, and the series simplifies to:

Where the variables are the same as before. The fraction is the future value annuity factor.

Future Value of Ordinary Annuities

Apply the formula directly. The first payment (made at the end of period 1) earns interest for periods, and the last payment earns no interest at all.

Example: You deposit $2,000 at the end of each year for 5 years at 8%.

Future Value of Annuities Due

Each payment earns interest for one additional period, so multiply by :

Same example with beginning-of-year deposits:

Annuity Payment Calculations

Often you know the present or future value and need to solve for one of the other variables. These rearrangements come up frequently in loan structuring and financial planning.

Solving for Annuity Payments

Rearrange the PV formula to isolate :

Example: You borrow $100,000 at 5% annual interest, repaid in 10 equal annual installments. What's the annual payment?

Determining Number of Payments

Rearrange the FV formula to solve for :

This requires logarithms, so a financial calculator or spreadsheet is the practical approach.

Calculating Interest Rate in Annuities

Solving for cannot be done algebraically because appears both inside and outside an exponent. You'll need to use:

- Trial and error with interpolation

- A financial calculator (the I/Y key)

- A spreadsheet function like

RATE()in Excel

Deferred Annuities and Values

A deferred annuity is one where payments don't start until some future date. For example, a student loan might not require payments until 6 months after graduation. The deferral period is the gap between now and the first payment.

Deferred Annuity Calculations

To find the present value of a deferred annuity, use a two-step process:

- Calculate the PV of the annuity as if it starts today. Use the standard ordinary annuity PV formula. This gives you the value as of one period before the first payment.

- Discount that lump sum back to the actual present. Treat the result from Step 1 as a single future amount and discount it for the number of deferral periods using , where is the number of deferral periods.

Example: An annuity pays $3,000 per year for 5 years, but the first payment is at the end of year 4 (so there's a 3-year deferral). The rate is 7%.

-

PV at end of year 3:

-

Discount to today:

Present and Future Values

- The present value of a deferred annuity is always less than that of an identical annuity starting immediately, because of the additional discounting during the deferral period.

- The future value is calculated by first finding the value at the start of the payment period, then compounding forward to the desired future date using the single-sum FV formula.

Annuities with Non-Annual Periods

Many real-world annuities involve monthly, quarterly, or semiannual payments. The formulas don't change; you just need to adjust the rate and number of periods to match the payment frequency.

Adjusting for Monthly Payments

- Use the monthly interest rate:

- Use the total number of monthly periods:

The PV formula for a monthly ordinary annuity becomes:

Example: A car loan requires $400/month for 5 years at 6% annual interest.

Adjusting for Quarterly Payments

- Use the quarterly interest rate:

- Use the total number of quarterly periods:

The FV formula for a quarterly annuity due becomes:

Watch out: These adjustments assume the stated annual rate is a nominal rate that compounds at the same frequency as the payments. If you're given an effective annual rate, you'll need to convert it to the periodic rate differently.

Annuities with Changing Payments

Not all annuities have level payments. Some increase or decrease by a fixed amount each period (arithmetic gradient) or by a fixed percentage (geometric gradient). These are less common in introductory problems but do appear in practice.

Increasing Annuity Payments

For payments that increase by a fixed dollar amount each period (so payments are , , , etc.), you can split the stream into a level annuity plus a gradient component.

The present value of the gradient portion alone is:

Add this to the PV of the level annuity (using the base payment ) to get the total present value.

Decreasing Annuity Payments

For payments that decrease by a fixed amount each period, use the same gradient formula but subtract the gradient PV from the level annuity PV. The logic is the same, just in reverse: you have a base annuity minus an increasing reduction.

Perpetuities and Calculations

A perpetuity is an annuity that never ends. While no payment stream truly lasts forever, perpetuities are a useful model for preferred stock dividends, endowment funds, and certain valuation techniques.

Present Value of Perpetuities

Because the payments continue indefinitely, the formula simplifies dramatically. As , the term , and the annuity formula collapses to:

This assumes an ordinary perpetuity (payments at end of period). For a perpetuity due (payments at beginning of period):

Example: A preferred stock pays $8 per year indefinitely. If the required return is 10%:

Distinguishing Perpetuities from Annuities

- Annuities have a fixed number of periods ; perpetuities do not.

- Perpetuities have no future value (there's no end point to accumulate to).

- The perpetuity PV formula is actually the annuity PV formula with the term set to zero.

Annuities in Financial Statements

Annuity calculations directly affect how companies report obligations and assets. The present value of an annuity stream determines the recorded amount, and changes over time flow through the income statement.

Annuity Impacts on Balance Sheet

- The PV of an annuity obligation (like a loan or lease) appears as a liability. At inception, a $100,000 loan is recorded at its present value.

- If the company receives annuity payments (e.g., a note receivable), the PV appears as an asset.

- Each period, the carrying amount changes as interest accrues and payments are made. The liability decreases over time as principal is repaid.

Annuity Impacts on Income Statement

- Interest expense is recognized each period on annuity obligations. It equals the beginning carrying amount multiplied by the interest rate.

- Interest income is recognized if the company holds an annuity-based asset.

- The cash payment is split between interest (income statement) and principal reduction (balance sheet). Early in the annuity's life, a larger share of each payment goes to interest; later, more goes to principal.

Annuity Applications and Examples

Loan Amortization Schedules

An amortization schedule shows how each payment on a loan breaks down into interest and principal. Here's how it works:

- Calculate the periodic payment using the PV annuity formula solved for .

- For each period, compute interest as the beginning balance times the periodic rate.

- The principal portion is the total payment minus the interest.

- Subtract the principal portion from the beginning balance to get the ending balance.

- Repeat until the balance reaches zero.

Example (partial schedule): $10,000 loan, 5% annual rate, 3 annual payments.

| Year | Beg. Balance | Payment | Interest (5%) | Principal | End Balance |

|---|---|---|---|---|---|

| 1 | $10,000.00 | $3,672.09 | $500.00 | $3,172.09 | $6,827.91 |

| 2 | $6,827.91 | $3,672.09 | $341.40 | $3,330.69 | $3,497.22 |

| 3 | $3,497.22 | $3,672.09 | $174.86 | $3,497.23 | $0.00 |

Notice how interest shrinks and principal grows with each payment.

Retirement Planning with Annuities

- Immediate annuities begin payments right away and are used to convert a lump sum into a steady income stream.

- Deferred annuities delay payments to a future date, allowing the investment to grow during the deferral period.

- Annuities can be fixed (constant payments) or variable (payments fluctuate based on investment returns).

Valuing Annuity-Based Financial Instruments

Bonds are the most common example. A bond's price equals the PV of its coupon payments (an annuity) plus the PV of its face value (a single lump sum), both discounted at the market interest rate.

This framework applies to any instrument that combines periodic payments with a final lump sum.