📈Business Microeconomics Unit 1 Review

1.4 Economic models and their applications in decision-making

1.4 Economic models and their applications in decision-making

Unit & Topic Study Guides

Microeconomics for Business Decisions

Supply and Demand: Market Equilibrium

Elasticity: Business Applications

Consumer Behavior & Utility Theory

Production and Cost Analysis

Competitive Markets & Profit Maximization

Market Structures: Monopoly to Oligopoly

Pricing Strategies & Market Power

Game Theory in Strategic Decision-Making

Asymmetric Info: Selection & Moral Hazard

Externalities, Public Goods & Gov't Role

Factor Markets & Income Distribution

Financial Markets in Microeconomics

Investment & Risk Management Decisions

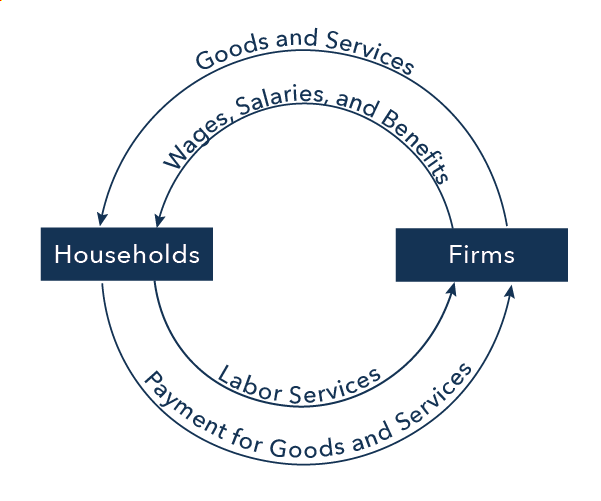

Economic models simplify complex real-world phenomena, helping businesses understand and predict economic behavior. They use assumptions like ceteris paribus to isolate key variables, but this can limit their accuracy in certain scenarios.

Businesses use various models for different purposes. Supply and demand models analyze markets, production functions optimize resources, and game theory models inform competitive strategies. Evaluating model effectiveness is crucial for informed decision-making.

Purpose and Limitations of Economic Models

Simplified Representations of Complex Phenomena

- Economic models create simplified representations of complex real-world phenomena

- Used to explain, predict, and analyze economic behavior and outcomes

- Serve as tools for understanding relationships between variables

- Allow for testing hypotheses and formulating economic theories

- Ceteris paribus assumption forms a fundamental component in economic modeling

- Enables isolation and analysis of specific variables

- Holds other variables constant to focus on key relationships

- Models often rely on assumptions and simplifications

- Can limit accuracy and applicability in certain real-world scenarios (financial crises, rapid technological changes)

- May not account for all relevant factors or oversimplify complex relationships

- Example: Assuming perfect competition in markets with significant barriers to entry

Effectiveness and Evaluation of Models

- Effectiveness of economic models varies based on context, available data, and specific economic phenomenon studied

- Example: Supply and demand models work well for commodity markets but may be less effective for unique goods

- Critical evaluation and interpretation of model results essential for informed decision-making

- Assess accuracy by comparing predictions with actual outcomes

- Identify potential sources of discrepancies (data quality, omitted variables)

- Analyze sensitivity of model results to changes in assumptions or input variables

- Determines robustness of model's conclusions

- Example: Testing how changes in interest rates affect investment models

- Evaluate trade-offs between model simplicity and complexity

- Consider balance between ease of use and accuracy of results

- Simple models may be more practical but less precise (linear demand curves)

- Complex models may offer more accuracy but require more data and expertise to implement

Common Economic Models for Business

Market and Production Models

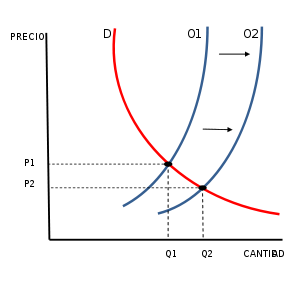

- Supply and demand models analyze market equilibrium and price determination

- Illustrate effects of shifts in supply or demand curves on market outcomes

- Applications include predicting price changes due to supply shocks (oil embargoes)

- Production functions show relationship between inputs and outputs

- Help businesses optimize resource allocation and production processes

- Examples include Cobb-Douglas function, constant elasticity of substitution (CES) function

- Cost curves assist in understanding cost structures and optimal production levels

- Include average cost (AC) and marginal cost (MC) curves

- Used to determine profit-maximizing output levels and break-even points

Strategic and Analytical Models

- Game theory models analyze strategic decision-making in competitive environments

- Consider actions and reactions of multiple players

- Applications include pricing strategies in oligopolistic markets (airline industry)

- Regression analysis models identify relationships between variables and forecast trends

- Based on historical data

- Used for sales forecasting, demand estimation, and economic indicator analysis

- Input-output models examine interdependencies between different economic sectors

- Useful for understanding supply chain dynamics and industry interactions

- Help assess impact of changes in one industry on related sectors (automotive manufacturing on steel production)

- Behavioral economics models incorporate psychological insights

- Explain deviations from rational decision-making in various business contexts

- Applications include designing marketing strategies and employee incentive programs

Applying Economic Models to Business

Market Analysis and Strategy

- Utilize supply and demand analysis to predict market outcomes

- Inform pricing strategies in response to changes in market conditions

- Example: Adjusting product prices based on seasonal demand fluctuations

- Employ game theory models to develop competitive strategies

- Anticipate competitors' actions in oligopolistic markets

- Applications include deciding on advertising expenditures or new product launches

- Apply behavioral economics insights to design effective strategies

- Develop pricing models that account for consumer psychology (anchoring effects)

- Create employee incentive programs based on loss aversion principles

Production and Cost Optimization

- Apply production functions to optimize resource allocation

- Determine most efficient combination of inputs for given output levels

- Example: Deciding between labor-intensive or capital-intensive production methods

- Use cost curve analysis to identify profit-maximizing production levels

- Make decisions regarding capacity expansion or contraction

- Applications include determining whether to open new facilities or outsource production

Forecasting and Industry Analysis

- Implement regression analysis to forecast key business metrics

- Predict sales, demand, or other economic variables

- Example: Estimating future raw material costs based on economic indicators

- Utilize input-output models to assess industry-wide impacts

- Inform supply chain management decisions

- Applications include evaluating effects of trade policies on interconnected industries

Effectiveness of Economic Models in Business

Model Performance and Adaptation

- Compare performance of different economic models in addressing similar business problems

- Determine most effective approach for specific contexts

- Example: Comparing time series models vs. econometric models for sales forecasting

- Identify situations where specific economic models are most applicable

- Recognize limitations in different business contexts

- Applications include using different models for short-term vs. long-term planning

- Consider impact of external factors on validity and relevance of economic models

- Account for technological changes or regulatory shifts over time

- Example: Adapting models to incorporate effects of e-commerce on traditional retail

Integrating Multiple Models

- Develop strategies for integrating insights from multiple economic models

- Provide more comprehensive analysis of complex business scenarios

- Combine supply-demand models with game theory for pricing in competitive markets

- Assess accuracy of model predictions through outcome comparison

- Identify potential sources of discrepancies (data quality, model specification)

- Use findings to refine and improve models over time

- Evaluate models' ability to capture real-world complexity

- Balance between model simplicity and ability to represent complex economic relationships

- Example: Incorporating non-linear relationships in demand models to better reflect consumer behavior