💲Honors Economics Unit 1 Review

1.3 Positive vs. Normative Economics

1.3 Positive vs. Normative Economics

Unit & Topic Study Guides

Economics and Economic Reasoning

Supply, Demand, and Market Equilibrium

Consumer Behavior and Utility Theory

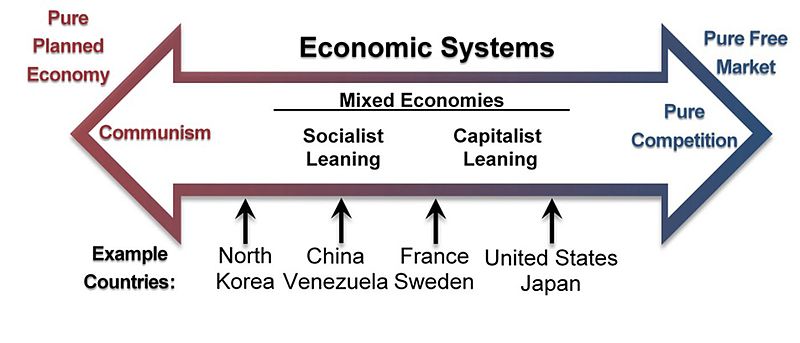

Production, Costs, and Market Structures

Resource Markets: Labor, Capital & Land

Market Failures: Externalities & Public Goods

Government Intervention and Regulation

Economic Performance and National Income

Economic Growth and Productivity

Unemployment and Inflation

Aggregate Demand and Aggregate Supply

Fiscal Policy and Government Budgets

Money, Banking, and Financial Markets

Monetary Policy & the Federal Reserve

International Trade & Comparative Advantage

Exchange Rates & Balance of Payments

Behavioral Economics and Decision Making

Game Theory and Strategic Interactions

Information Economics & Asymmetry

Economic Development and Globalization

Positive vs Normative Economics

Defining Positive and Normative Economics

Every economic statement falls into one of two categories, and being able to tell them apart is one of the most useful skills in this course.

Positive economics deals with objective, factual claims that can be tested and verified with evidence. These statements describe cause-and-effect relationships and rely on data-driven analysis. Positive statements use language that describes what is, was, or will be.

- "The unemployment rate in the United States was 3.6% in April 2022."

- "When the Federal Reserve raises interest rates, borrowing decreases."

Both of these can be checked against real-world data. You don't have to agree or disagree with them; you just verify whether they're true.

Normative economics involves subjective value judgments and opinions about what ought to be. These statements reflect individual or societal values rather than empirical evidence, and they often include words like "should," "ought," or "better."

- "The government should provide universal basic income to reduce income inequality."

- "The minimum wage ought to be raised to improve living standards."

You can't prove or disprove these with data alone, because they depend on what someone believes is fair or desirable.

Key Distinctions and Importance

The core test is straightforward: Can the statement be proven or disproven with data? If yes, it's positive. If it depends on values or opinions, it's normative.

- Positive economics can be objectively measured and tested (GDP growth rates, inflation figures, employment statistics).

- Normative economics relies on subjective interpretations and value systems, so two people can look at the same data and reach different normative conclusions.

Understanding this distinction matters for a few reasons:

- It helps economists and students separate facts from opinions in their analysis, which is the foundation of unbiased research.

- It makes it easier to evaluate economic theories and policies on their actual merits rather than on the rhetoric surrounding them.

- It highlights where conflicts between economic efficiency and social equity arise. Positive economics tends to address efficiency questions (Does this policy maximize output?), while normative economics addresses equity questions (Is the outcome fair? Who benefits and who loses?).

Examples of Economic Analysis

Positive Economic Analysis Examples

Positive analysis uses data and models to describe what happens in the economy. Here are some common examples:

- Minimum wage and employment: Economists examine historical data on wage changes and employment figures, then use regression analysis to determine whether higher minimum wages correlate with changes in employment levels. The conclusion is testable.

- Trade tariffs: Researchers measure changes in import/export quantities after a tariff is implemented and calculate the impact on domestic industry output. For instance, you could track U.S. steel production before and after a 25% tariff on imported steel.

- Interest rates and inflation: Central banks adjust interest rates, and economists track subsequent changes in inflation and GDP growth. If the Fed raises rates by 0.75%, you can measure what happens to consumer prices over the following quarters.

- Education and income: By collecting data on years of schooling and average salaries across professions, economists use statistical methods to quantify the relationship. Studies consistently find that each additional year of education correlates with roughly 8–13% higher earnings.

In each case, the analysis produces a claim that can be checked against evidence.

Normative Economic Analysis Examples

Normative analysis makes recommendations based on values. Notice how each example below involves a judgment call that data alone can't settle:

- Raising the minimum wage: Arguing that the government should raise the minimum wage reflects a belief that workers deserve a certain quality of life. Two economists can agree on the positive data (what a wage increase does to employment) and still disagree on whether the trade-offs are worth it.

- Free trade agreements: Advocating for or against free trade involves weighing job displacement in certain sectors against benefits like lower consumer prices and greater product variety. The "right" answer depends on whose interests you prioritize.

- Inflation targets: Proposing that the Federal Reserve should aim for a higher inflation target to stimulate growth reflects a judgment about the acceptable balance between price stability and economic expansion.

- Government spending on renewable energy: Recommending increased clean energy investment involves weighing upfront economic costs against long-term environmental and societal benefits. The value you place on environmental protection shapes your conclusion.

Importance of Distinguishing Economics in Policy

Enhancing Policy Evaluation and Development

When policymakers separate positive claims from normative ones, they can evaluate proposals more clearly:

- They can focus on empirical data when assessing potential outcomes, using economic models and statistical analysis rather than relying on rhetoric.

- They can identify the underlying assumptions and value judgments behind different proposals. This makes the ethical considerations behind a recommendation visible rather than hidden.

- They can develop more balanced policies by combining data-driven insights with explicit discussions about societal values, addressing both efficiency and equity.

Improving Economic Discourse and Decision-Making

This distinction also improves how people debate economic issues:

- It separates discussions about what is from debates about what ought to be, which helps identify where people actually agree on the facts and where they disagree on values.

- It helps reduce cognitive biases like confirmation bias. When you're aware that a statement is normative, you're less likely to treat it as settled fact just because it aligns with your beliefs.

- It encourages transparency. When politicians or economists make policy recommendations, recognizing the normative components helps citizens understand why a particular direction is being proposed and what values are driving it.

The bottom line: positive economics gives you the facts, normative economics applies values to those facts. Strong economic reasoning requires both, but you need to know which one you're using at any given moment.