Contemporary cost allocation approaches offer innovative ways to understand and manage costs. These methods go beyond traditional volume-based allocation, providing deeper insights into resource consumption and value creation.

From activity-based costing to lean accounting, these techniques help businesses make smarter decisions. They reveal hidden costs, optimize processes, and align financial management with strategic goals, ultimately improving profitability and competitiveness.

Activity-Based Costing Approaches

Traditional ABC and Time-Driven ABC

- Activity-Based Costing (ABC) assigns overhead costs to products based on activities performed

- Identifies cost drivers related to specific activities

- Allocates costs more accurately than traditional volume-based methods

- Improves decision-making by providing detailed cost information

- Time-Driven ABC simplifies the traditional ABC approach

- Uses time equations to estimate resource demands for each activity

- Reduces implementation complexity and maintenance costs

- Provides more flexibility in handling variations in activities

- Both methods help managers understand cost behavior and identify improvement opportunities

- (Customer profitability analysis, product mix decisions)

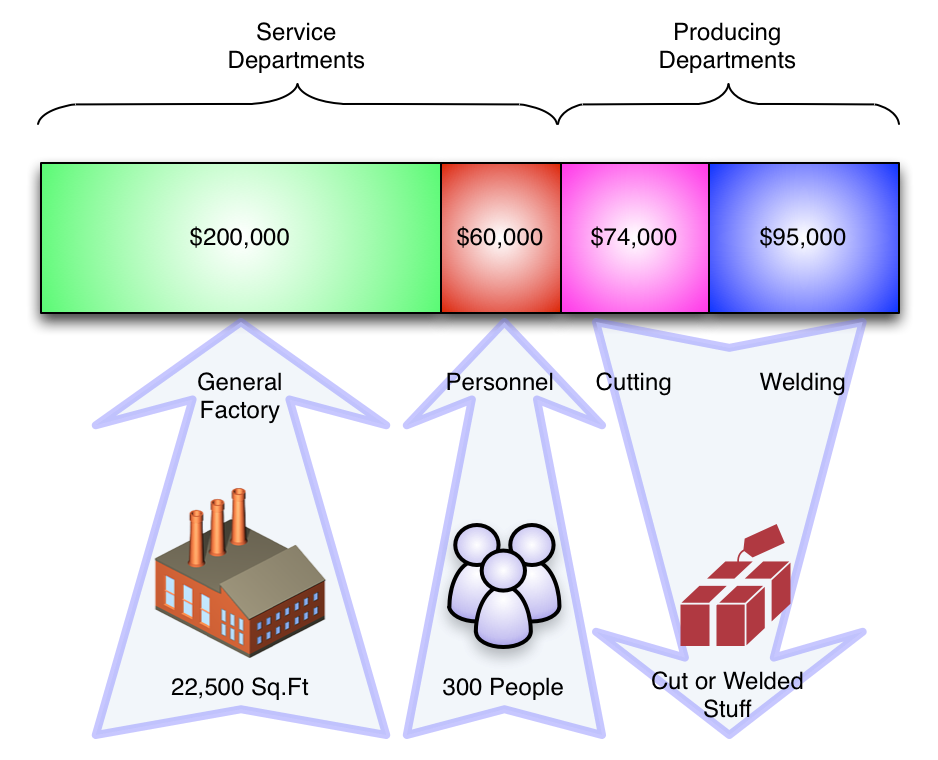

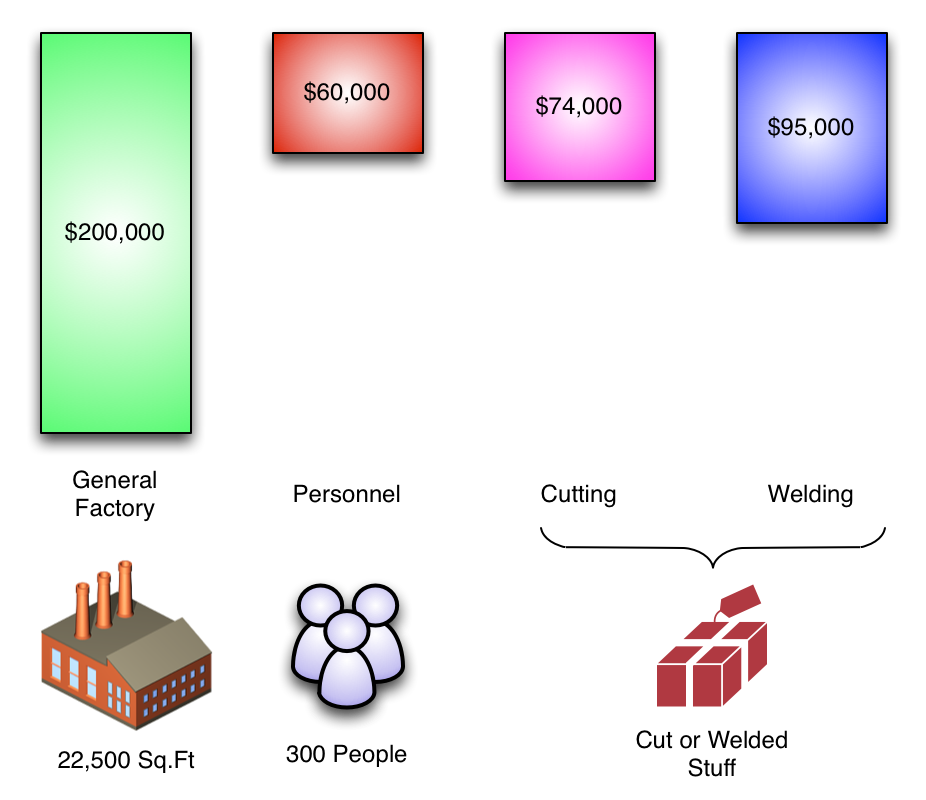

Capacity and Process-Based Approaches

- Capacity-driven allocation focuses on resource utilization

- Separates costs into used and unused capacity

- Highlights inefficiencies and excess capacity in operations

- Supports better resource management decisions

- Process-based costing analyzes costs along entire value chains

- Maps out all activities involved in delivering a product or service

- Identifies value-added and non-value-added activities

- Helps streamline processes and reduce waste

- These approaches provide insights for continuous improvement initiatives

- (Manufacturing plant layout optimization, service delivery redesign)

Resource Consumption Accounting

Resource Consumption Accounting (RCA) Principles

- Resource Consumption Accounting (RCA) combines elements of ABC and German cost accounting

- Emphasizes resource consumption and capacity analysis

- Uses a three-pillar approach: view of resources, quantity-based model, and cost flows

- Provides more granular cost information than traditional methods

- RCA helps identify underutilized resources and optimize capacity

- Supports make-or-buy decisions and outsourcing evaluations

- Enhances cost control and resource allocation strategies

- Implements a comprehensive cost management system

- (Manufacturing equipment utilization, IT infrastructure costs)

Lean Accounting and Value Stream Costing

- Value stream costing aligns with lean manufacturing principles

- Focuses on the flow of value through entire product families

- Simplifies cost allocation by assigning costs to value streams rather than individual products

- Supports continuous improvement and waste reduction efforts

- Lean accounting adapts financial reporting to lean operations

- Eliminates non-value-added accounting transactions

- Provides real-time performance measures aligned with lean goals

- Supports decision-making in a lean environment

- Both methods promote a holistic view of costs and value creation

- (Automotive assembly line optimization, healthcare service delivery improvement)

Cost Management Techniques

Target Costing and Cost Reduction Strategies

- Target costing reverses traditional cost-plus pricing approach

- Starts with target selling price and desired profit margin

- Determines allowable costs to achieve profit goals

- Drives innovation and cost reduction throughout product development

- Implements cross-functional teams to achieve cost targets

- Involves design, engineering, manufacturing, and marketing departments

- Encourages collaboration and creative problem-solving

- Supports continuous improvement and competitive pricing strategies

- (New product development in consumer electronics, automotive design)

- Integrates with other cost management techniques

- Value engineering to improve product functionality while reducing costs

- Kaizen costing for ongoing cost reduction in production processes

- Life-cycle costing to consider total product costs from development to disposal