Blockchain and cryptocurrencies are revolutionizing finance and challenging traditional regulatory frameworks. These technologies offer decentralized, borderless systems that promise increased efficiency and transparency, but also raise concerns about consumer protection and financial stability.

Regulators worldwide are grappling with how to oversee this rapidly evolving landscape. Key issues include jurisdictional challenges, anonymity concerns, and the need to balance innovation with risk management. Approaches range from permissive to restrictive, with many countries adopting regulatory sandboxes to test new ideas.

Fundamentals of blockchain technology

- Blockchain technology forms the foundation of cryptocurrencies and decentralized systems, revolutionizing data storage and transaction processing

- This technology intersects with policy considerations due to its potential to disrupt traditional financial systems and governance structures

- Understanding blockchain fundamentals provides crucial context for developing effective regulatory frameworks in the digital age

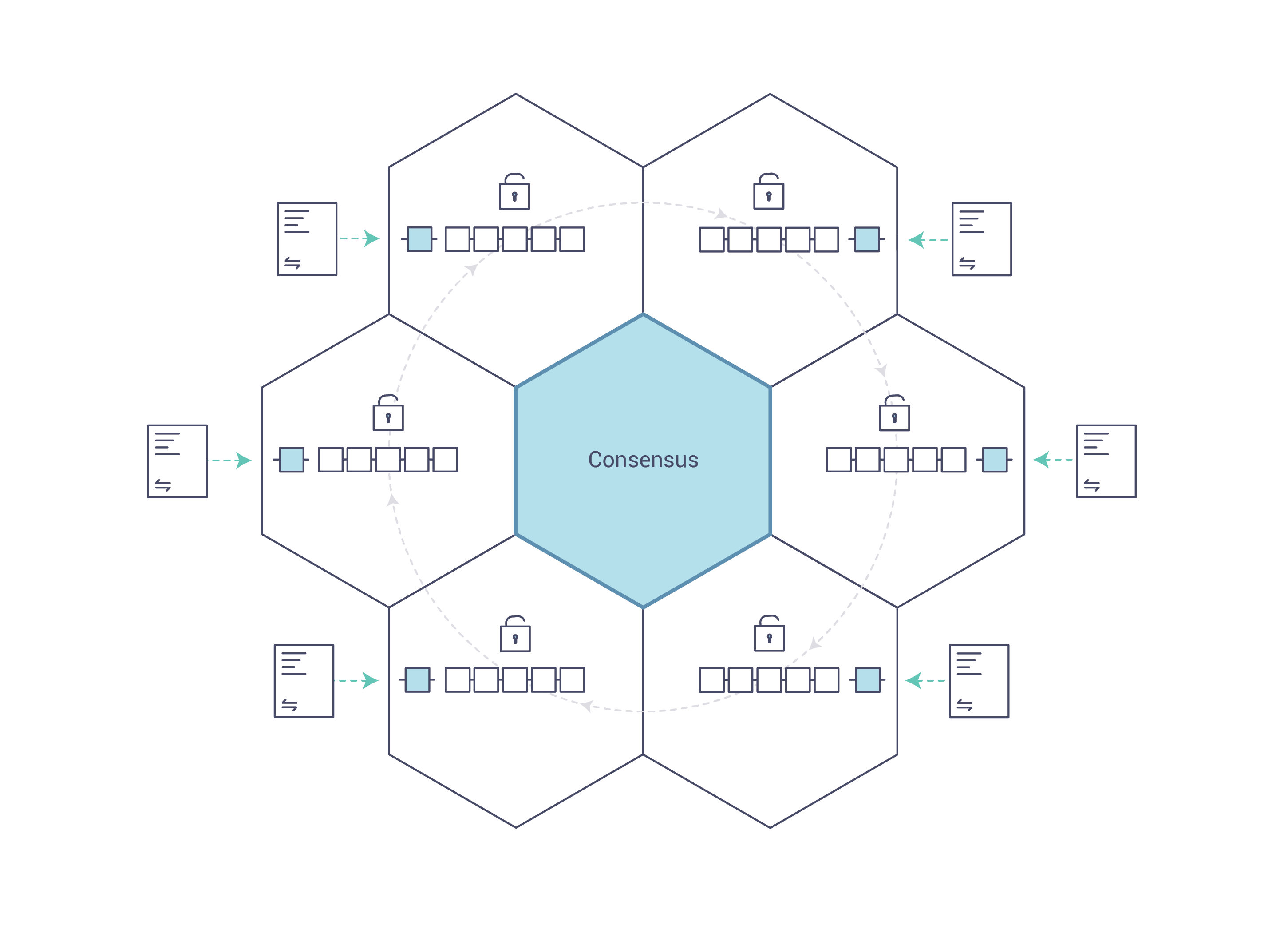

Distributed ledger systems

- Decentralized databases maintain synchronized copies across multiple nodes

- Eliminate need for central authority to validate transactions

- Enhance transparency and reduce single points of failure

- Implement through various consensus mechanisms (proof-of-work, proof-of-stake)

Cryptographic principles

- Utilize public key cryptography for secure transactions and digital signatures

- Employ hash functions to create unique, tamper-evident block identifiers

- Ensure data integrity and user authentication within the blockchain network

- Implement zero-knowledge proofs for privacy-preserving transactions

Consensus mechanisms

- Algorithms used to achieve agreement on the state of the blockchain

- Proof-of-Work (PoW) relies on computational power to solve complex puzzles

- Proof-of-Stake (PoS) selects validators based on their cryptocurrency holdings

- Delegated Proof-of-Stake (DPoS) allows token holders to vote for block producers

- Byzantine Fault Tolerance (BFT) protocols ensure consensus in presence of malicious actors

Smart contracts

- Self-executing agreements with terms directly written into code

- Automate contract execution when predefined conditions are met

- Enable creation of decentralized applications (DApps) on blockchain platforms

- Raise regulatory challenges due to their autonomous and borderless nature

Cryptocurrency basics

- Cryptocurrencies represent digital or virtual currencies secured by cryptography

- These digital assets operate on blockchain technology, offering alternatives to traditional financial systems

- Understanding cryptocurrency fundamentals informs policy decisions on their integration into existing economic frameworks

Types of cryptocurrencies

- Bitcoin serves as the first and most well-known cryptocurrency

- Altcoins include alternative cryptocurrencies like Ethereum, Litecoin, and Ripple

- Stablecoins peg their value to external references (USD, gold) for price stability

- Privacy coins (Monero, Zcash) focus on enhanced transaction anonymity

- Utility tokens provide access to specific blockchain-based services or products

Digital wallets

- Software applications store private keys for cryptocurrency management

- Hot wallets maintain constant internet connection for easy access

- Cold wallets store keys offline for enhanced security (hardware wallets, paper wallets)

- Multi-signature wallets require multiple approvals for transactions

- Implement various security measures (two-factor authentication, biometric verification)

Mining and transactions

- Mining involves validating new transactions and adding them to the blockchain

- Proof-of-Work mining requires solving complex mathematical problems

- Transactions broadcast to the network for verification by nodes

- Block rewards and transaction fees incentivize miners to maintain the network

- Mining pools allow multiple users to combine computational resources

Blockchain vs traditional finance

- Decentralized nature eliminates need for intermediaries (banks, clearinghouses)

- Increased transaction speed and reduced costs for cross-border transfers

- Enhanced transparency through public ledgers accessible to all participants

- Programmable money enables automated, condition-based transactions

- Challenges traditional monetary policy tools and financial regulations

Regulatory challenges

- Blockchain and cryptocurrencies present unique regulatory challenges due to their decentralized and borderless nature

- Policymakers must balance innovation fostering with consumer protection and financial stability

- Addressing these challenges requires collaboration between technologists, economists, and legal experts

Jurisdictional issues

- Decentralized networks operate across national borders, complicating enforcement

- Determining applicable laws for blockchain-based transactions proves challenging

- Conflicting regulations between jurisdictions create regulatory arbitrage opportunities

- International cooperation needed to establish consistent global regulatory framework

- Extraterritorial application of national laws raises sovereignty concerns

Anonymity concerns

- Pseudonymous nature of blockchain transactions complicates user identification

- Privacy coins and mixing services further enhance transaction anonymity

- Balancing privacy rights with need for financial transparency and accountability

- Challenges in implementing Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations

- Development of privacy-preserving compliance techniques (zero-knowledge proofs)

Fraud and market manipulation

- Pump-and-dump schemes exploit low liquidity and high volatility in crypto markets

- Wash trading artificially inflates trading volumes on exchanges

- Front-running attacks take advantage of public transaction pools

- Challenges in detecting and preventing smart contract vulnerabilities and exploits

- Need for robust market surveillance and enforcement mechanisms

Tax implications

- Classifying cryptocurrencies as property, currency, or securities affects tax treatment

- Tracking cost basis and capital gains for frequent traders proves complex

- Challenges in valuing cryptocurrencies received as income or payment

- International tax evasion concerns due to ease of cross-border transactions

- Development of specialized software for crypto tax reporting and compliance

Global regulatory approaches

- Countries adopt diverse strategies to regulate blockchain and cryptocurrencies

- Regulatory approaches range from embracing innovation to outright bans

- Global coordination efforts aim to establish consistent standards and prevent regulatory arbitrage

Permissive vs restrictive policies

- Permissive jurisdictions (Singapore, Switzerland) foster innovation through supportive regulations

- Restrictive approaches (China, India) impose bans or severe limitations on crypto activities

- Balanced policies (United States, European Union) aim to protect consumers while enabling innovation

- Regulatory clarity attracts blockchain businesses and investment to certain jurisdictions

- Policy decisions influence global competitiveness in emerging digital economy

Regulatory sandboxes

- Controlled environments allow testing of innovative financial products and services

- Enable regulators to understand new technologies without stifling innovation

- Provide temporary regulatory relief for blockchain and crypto startups

- Facilitate dialogue between innovators and regulators to inform policy development

- Implemented successfully in jurisdictions like the UK, Singapore, and Australia

International cooperation efforts

- Financial Action Task Force (FATF) develops global standards for crypto regulation

- G20 countries collaborate on creating consistent approach to crypto asset risks

- Bank for International Settlements (BIS) researches implications of cryptocurrencies

- European Union's Markets in Crypto-Assets (MiCA) regulation aims for harmonized framework

- Bilateral agreements between countries address cross-border enforcement and information sharing

Key regulatory bodies

- Various government agencies and organizations play crucial roles in shaping blockchain and cryptocurrency regulations

- Coordination between these bodies essential for developing comprehensive regulatory frameworks

- Understanding the roles and jurisdictions of these entities informs effective policy development

Financial regulators

- Securities and Exchange Commission (SEC) oversees securities laws application to cryptocurrencies

- Commodity Futures Trading Commission (CFTC) regulates crypto derivatives and futures markets

- Financial Crimes Enforcement Network (FinCEN) enforces AML regulations for crypto businesses

- Office of the Comptroller of the Currency (OCC) provides guidance on banks' crypto activities

- State-level regulators issue licenses and oversee local crypto businesses (New York BitLicense)

Securities commissions

- Determine whether cryptocurrencies and tokens qualify as securities

- Enforce registration requirements for crypto offerings deemed securities

- Investigate and prosecute fraudulent Initial Coin Offerings (ICOs)

- Provide guidance on compliant token issuance and trading platforms

- Collaborate internationally to address cross-border securities violations

Central banks

- Research and develop Central Bank Digital Currencies (CBDCs)

- Assess impact of cryptocurrencies on monetary policy and financial stability

- Provide guidance to commercial banks on crypto-related activities

- Participate in international forums to address global crypto challenges

- Monitor systemic risks posed by large-scale adoption of cryptocurrencies

Law enforcement agencies

- Investigate crypto-related crimes (money laundering, terrorist financing, fraud)

- Develop specialized units for tracking and seizing illicit crypto assets

- Collaborate with international partners to combat cross-border crypto crimes

- Provide training and resources for law enforcement on blockchain forensics

- Work with crypto businesses to improve compliance and prevent illicit activities

Legal frameworks

- Existing legal structures adapt to accommodate blockchain and cryptocurrency innovations

- New laws and regulations developed to address unique challenges posed by these technologies

- Balancing innovation, consumer protection, and financial stability guides legal framework development

Securities laws

- Apply Howey Test to determine if cryptocurrencies qualify as investment contracts

- Regulate Initial Coin Offerings (ICOs) and Security Token Offerings (STOs)

- Enforce registration requirements for crypto exchanges trading securities

- Adapt disclosure rules for blockchain-based securities offerings

- Develop guidance on compliant tokenization of traditional securities

Anti-money laundering regulations

- Extend Know Your Customer (KYC) requirements to crypto exchanges and wallet providers

- Implement Travel Rule for crypto transactions above certain thresholds

- Require Suspicious Activity Reports (SARs) for potentially illicit crypto activities

- Develop blockchain analytics tools to trace and monitor suspicious transactions

- Establish international cooperation for cross-border AML enforcement

Consumer protection measures

- Mandate clear disclosures of risks associated with cryptocurrency investments

- Implement cooling-off periods for crypto purchases to prevent impulsive decisions

- Regulate advertising and marketing practices for crypto products and services

- Establish dispute resolution mechanisms for crypto-related consumer complaints

- Develop educational initiatives to improve public understanding of blockchain and cryptocurrencies

Data privacy considerations

- Balance transparency of public blockchains with individual privacy rights

- Implement data minimization principles in blockchain-based systems

- Develop privacy-enhancing technologies compatible with regulatory requirements

- Address challenges of applying "right to be forgotten" to immutable blockchains

- Establish guidelines for secure storage and handling of private keys and personal data

Policy considerations

- Blockchain and cryptocurrency regulations intersect with broader policy objectives

- Policymakers must balance competing interests and potential societal impacts

- Long-term implications of these technologies shape policy decisions across various domains

Financial stability

- Assess systemic risks posed by large-scale cryptocurrency adoption

- Monitor potential impacts on traditional banking and payment systems

- Develop stress testing scenarios for crypto market crashes or stablecoin failures

- Evaluate effects of decentralized finance (DeFi) on broader financial ecosystem

- Consider implications of Central Bank Digital Currencies (CBDCs) on monetary policy

Innovation vs regulation

- Strike balance between fostering technological advancement and protecting public interest

- Implement principle-based regulations to accommodate rapid technological changes

- Encourage dialogue between innovators, regulators, and policymakers

- Develop regulatory frameworks flexible enough to adapt to emerging blockchain use cases

- Consider potential unintended consequences of overly restrictive regulations

Environmental impact

- Address energy consumption concerns associated with Proof-of-Work mining

- Encourage adoption of more energy-efficient consensus mechanisms (Proof-of-Stake)

- Develop policies to promote use of renewable energy sources for crypto mining

- Consider carbon taxation or offsetting requirements for energy-intensive blockchain activities

- Evaluate potential of blockchain technology in supporting environmental sustainability initiatives

Social equity concerns

- Assess potential of cryptocurrencies to promote financial inclusion for unbanked populations

- Address digital divide issues limiting access to blockchain-based services

- Consider implications of crypto adoption on wealth inequality and economic power distribution

- Develop policies to prevent exploitation of vulnerable populations through crypto scams

- Evaluate potential of blockchain technology in promoting transparent and equitable governance

Cryptocurrency exchanges

- Cryptocurrency exchanges serve as crucial infrastructure for buying, selling, and trading digital assets

- Regulatory frameworks for exchanges aim to ensure market integrity and protect investors

- Balancing innovation with consumer protection guides policy development for exchange oversight

Licensing requirements

- Implement specific licensing regimes for cryptocurrency exchanges (BitLicense in New York)

- Establish minimum capital requirements to ensure financial stability

- Mandate regular audits and financial reporting for licensed exchanges

- Require robust cybersecurity measures and insurance coverage

- Develop criteria for listing new cryptocurrencies or tokens on exchanges

KYC and AML compliance

- Implement tiered KYC requirements based on transaction volumes and risk levels

- Conduct ongoing customer due diligence and transaction monitoring

- Establish procedures for identifying and reporting suspicious activities

- Implement Travel Rule compliance for large-value crypto transfers

- Develop blockchain analytics capabilities for tracing transaction flows

Security standards

- Mandate multi-signature wallets and cold storage for majority of customer funds

- Implement regular security audits and penetration testing

- Establish incident response and disaster recovery plans

- Require strong authentication methods for user accounts (2FA, biometrics)

- Develop industry standards for secure key management and storage

Market surveillance

- Implement real-time monitoring systems to detect market manipulation

- Establish cross-market surveillance to identify coordinated manipulation attempts

- Develop algorithms to detect wash trading and other fraudulent activities

- Implement circuit breakers and trading halts during extreme market volatility

- Establish information sharing mechanisms between exchanges and regulators

Initial coin offerings

- Initial Coin Offerings (ICOs) represent a novel fundraising method using blockchain technology

- Regulatory approaches to ICOs vary globally, reflecting different interpretations of their nature

- Balancing innovation in capital formation with investor protection guides ICO regulation

ICO vs traditional fundraising

- ICOs allow direct fundraising from global investor base without intermediaries

- Tokens offer utility or equity-like rights in blockchain-based projects

- Lower barriers to entry compared to traditional IPOs or venture capital

- Rapid capital formation enables faster project development and scaling

- Challenges traditional securities laws and investor protection frameworks

Regulatory scrutiny

- SEC applies Howey Test to determine if ICO tokens qualify as securities

- Some jurisdictions ban ICOs outright due to investor protection concerns

- Regulatory uncertainty leads to decline in ICO activity and rise of Security Token Offerings (STOs)

- Increased focus on compliance and legal structuring of token sales

- Development of new regulatory frameworks specifically addressing token offerings (JOBS Act)

Investor protection measures

- Mandate detailed white papers disclosing project details and risk factors

- Implement KYC and AML procedures for ICO participants

- Establish escrow mechanisms for raised funds to prevent misuse

- Require smart contract audits to identify potential vulnerabilities

- Develop standards for post-ICO reporting and project milestone tracking

Central bank digital currencies

- Central Bank Digital Currencies (CBDCs) represent digital forms of national currencies issued by central banks

- CBDC development aims to modernize payment systems and address challenges posed by private cryptocurrencies

- Policy considerations for CBDCs include monetary policy implications, financial stability, and privacy concerns

CBDC design options

- Account-based models provide digital accounts directly with the central bank

- Token-based models mimic physical cash in digital form

- Wholesale CBDCs limited to financial institutions for interbank settlements

- Retail CBDCs available to general public for everyday transactions

- Hybrid models involve intermediaries managing CBDC distribution and user interfaces

Potential economic impacts

- Enhance monetary policy transmission through programmable money features

- Reduce costs and increase efficiency of payment systems

- Potentially disrupt traditional banking models and credit creation

- Address challenges posed by declining use of physical cash

- Provide financial inclusion for unbanked populations

Privacy vs transparency

- Balance individual privacy rights with need for financial oversight

- Implement tiered privacy levels based on transaction amounts or user types

- Develop privacy-enhancing technologies compatible with regulatory requirements

- Address concerns about government surveillance and control over financial activities

- Consider implications for cash-like anonymity in digital transactions

Decentralized finance (DeFi)

- Decentralized Finance (DeFi) leverages blockchain technology to recreate traditional financial services without intermediaries

- DeFi presents unique regulatory challenges due to its decentralized and borderless nature

- Policymakers grapple with applying existing financial regulations to this emerging ecosystem

DeFi protocols

- Decentralized exchanges (DEXs) enable peer-to-peer trading of cryptocurrencies

- Lending platforms allow users to borrow and lend crypto assets directly

- Yield farming protocols incentivize liquidity provision through token rewards

- Synthetic asset platforms create blockchain-based derivatives and tokenized assets

- Decentralized insurance protocols offer coverage for smart contract risks

Regulatory gaps

- Absence of clear regulatory jurisdiction over decentralized protocols

- Challenges in applying KYC and AML regulations to permissionless systems

- Difficulties in enforcing securities laws on decentralized token issuances

- Lack of clear guidelines for decentralized governance structures

- Regulatory uncertainty surrounding cross-border DeFi activities

Risk management challenges

- Smart contract vulnerabilities pose systemic risks to DeFi ecosystems

- High volatility and interconnectedness amplify potential for cascading failures

- Lack of consumer protections in case of hacks or protocol failures

- Challenges in assessing and managing counterparty risks in trustless systems

- Potential for market manipulation and front-running in decentralized markets

Future of blockchain regulation

- Evolving nature of blockchain technology necessitates adaptive regulatory approaches

- Balancing innovation, consumer protection, and financial stability guides future regulatory efforts

- International cooperation and harmonization play crucial roles in effective blockchain governance

Evolving legal frameworks

- Develop specialized blockchain laws addressing unique aspects of the technology

- Adapt existing regulations to accommodate blockchain-based business models

- Create new regulatory categories for crypto assets and decentralized organizations

- Establish clear guidelines for the intersection of blockchain with other emerging technologies (AI, IoT)

- Implement regulatory sandboxes to test and refine blockchain-specific regulations

Technology-neutral approaches

- Focus on regulating activities and outcomes rather than specific technologies

- Develop principle-based regulations adaptable to rapid technological changes

- Encourage self-regulatory efforts within the blockchain industry

- Implement risk-based approaches to accommodate diverse blockchain use cases

- Balance prescriptive rules with flexible guidelines to foster innovation

International harmonization efforts

- Establish global standards for blockchain and cryptocurrency regulation

- Develop common taxonomies and definitions for crypto assets across jurisdictions

- Create mechanisms for cross-border information sharing and enforcement cooperation

- Address regulatory arbitrage through coordinated policy approaches

- Promote inclusive dialogue involving developed and developing nations in shaping global blockchain governance