Operating leverage and margin of safety are crucial concepts in cost-volume-profit analysis. They help businesses understand how changes in sales impact profits and assess financial risk. These tools are vital for making informed decisions about pricing, production, and overall business strategy.

By analyzing operating leverage and margin of safety, managers can gauge their company's vulnerability to market fluctuations. This knowledge enables them to balance potential profitability with risk exposure, ultimately leading to more resilient and profitable operations.

Operating Leverage and DOL

Understanding Operating Leverage

- Operating leverage measures a company's fixed costs relative to its variable costs

- Higher operating leverage indicates a larger proportion of fixed costs in a company's cost structure

- Fixed costs remain constant regardless of production levels (rent, equipment leases, salaries)

- Variable costs change proportionally with production levels (raw materials, direct labor)

- Companies with high operating leverage experience greater profit fluctuations as sales volume changes

- Potential for higher profits during periods of increased sales

- Increased vulnerability during economic downturns or decreased demand

Calculating and Interpreting Degree of Operating Leverage (DOL)

- Degree of operating leverage quantifies the impact of changes in sales on operating income

- DOL formula:

- Alternative DOL formula:

- Higher DOL indicates greater sensitivity of operating income to changes in sales

- DOL of 2 means a 1% change in sales results in a 2% change in operating income

- Useful for comparing companies within the same industry

- Helps managers assess the impact of sales fluctuations on profitability

Assessing Business Risk

- Business risk refers to the uncertainty of a company's future operating income

- Factors influencing business risk include market conditions, competition, and cost structure

- Higher operating leverage generally leads to increased business risk

- Companies with high fixed costs face greater risk during economic downturns

- Low operating leverage provides more stability but may limit profit potential during growth periods

- Management must balance the trade-off between potential profitability and risk exposure

- Diversification of product lines or markets can help mitigate business risk

- Regular monitoring of DOL assists in managing and adjusting business risk levels

Margin of Safety

Calculating Margin of Safety

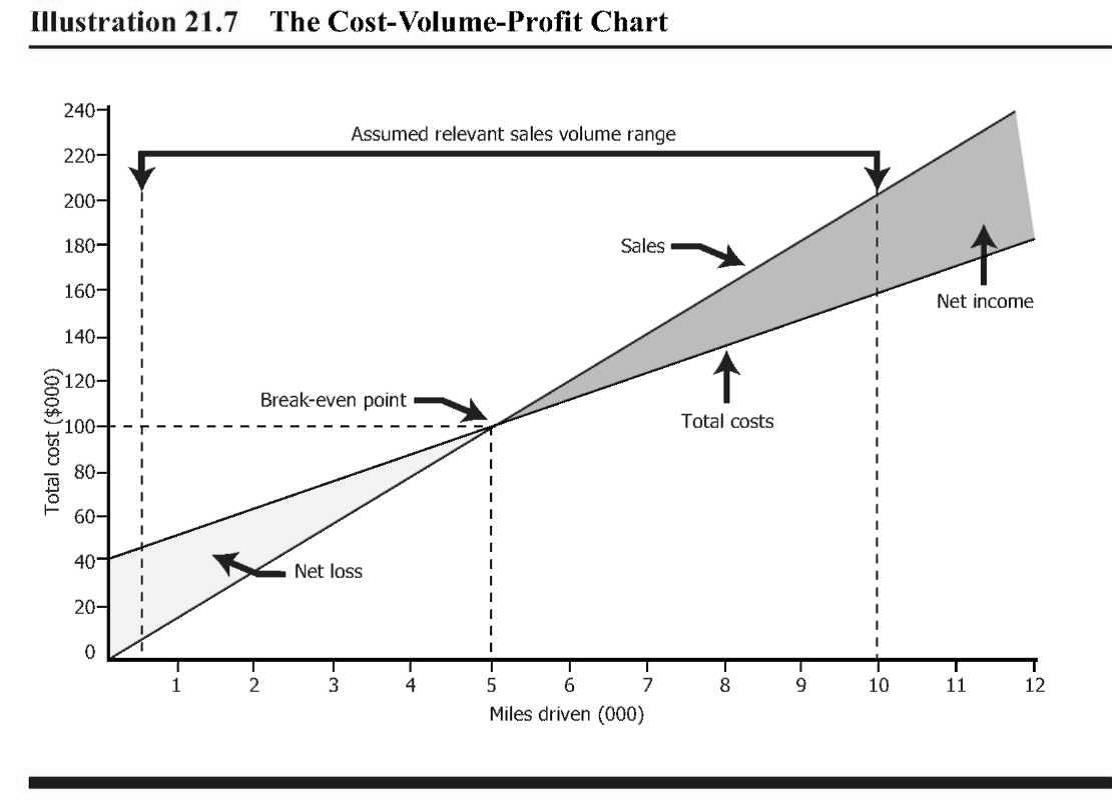

- Margin of safety represents the difference between actual or projected sales and break-even sales

- Formula:

- Expressed in units or monetary terms

- Larger margin of safety indicates greater financial cushion against potential sales declines

- Break-even point calculation:

- Contribution margin ratio:

- Managers use margin of safety to assess how much sales can decrease before incurring losses

Interpreting Margin of Safety Ratio

- Margin of safety ratio expresses the cushion as a percentage of total sales

- Formula:

- Higher ratio indicates stronger financial position and lower risk of losses

- Ratio of 30% means sales can drop by 30% before reaching the break-even point

- Useful for comparing different products, divisions, or time periods within a company

- Helps in setting sales targets and evaluating overall business performance

- Managers aim to increase the margin of safety ratio through cost control or sales growth

Utilizing Margin of Safety for Risk Assessment

- Margin of safety serves as a key indicator of a company's financial health and risk level

- Lower margin of safety suggests higher vulnerability to market fluctuations

- Useful for evaluating the impact of potential changes in sales volume or pricing

- Aids in decision-making processes (product mix, pricing strategies, cost management)

- Investors and creditors consider margin of safety when assessing company stability

- Regular monitoring allows for early detection of declining financial performance

- Combining margin of safety analysis with other financial metrics provides comprehensive risk assessment

- Scenario analysis using different margin of safety levels helps in strategic planning and risk mitigation