Least squares estimation is a powerful method for finding the best-fitting line in linear regression. It minimizes the sum of squared residuals, providing optimal estimates for the slope and intercept of the regression equation.

This technique is crucial in simple linear regression, allowing us to quantify relationships between variables. By minimizing errors, least squares estimation helps create models that accurately predict outcomes and explain variability in data.

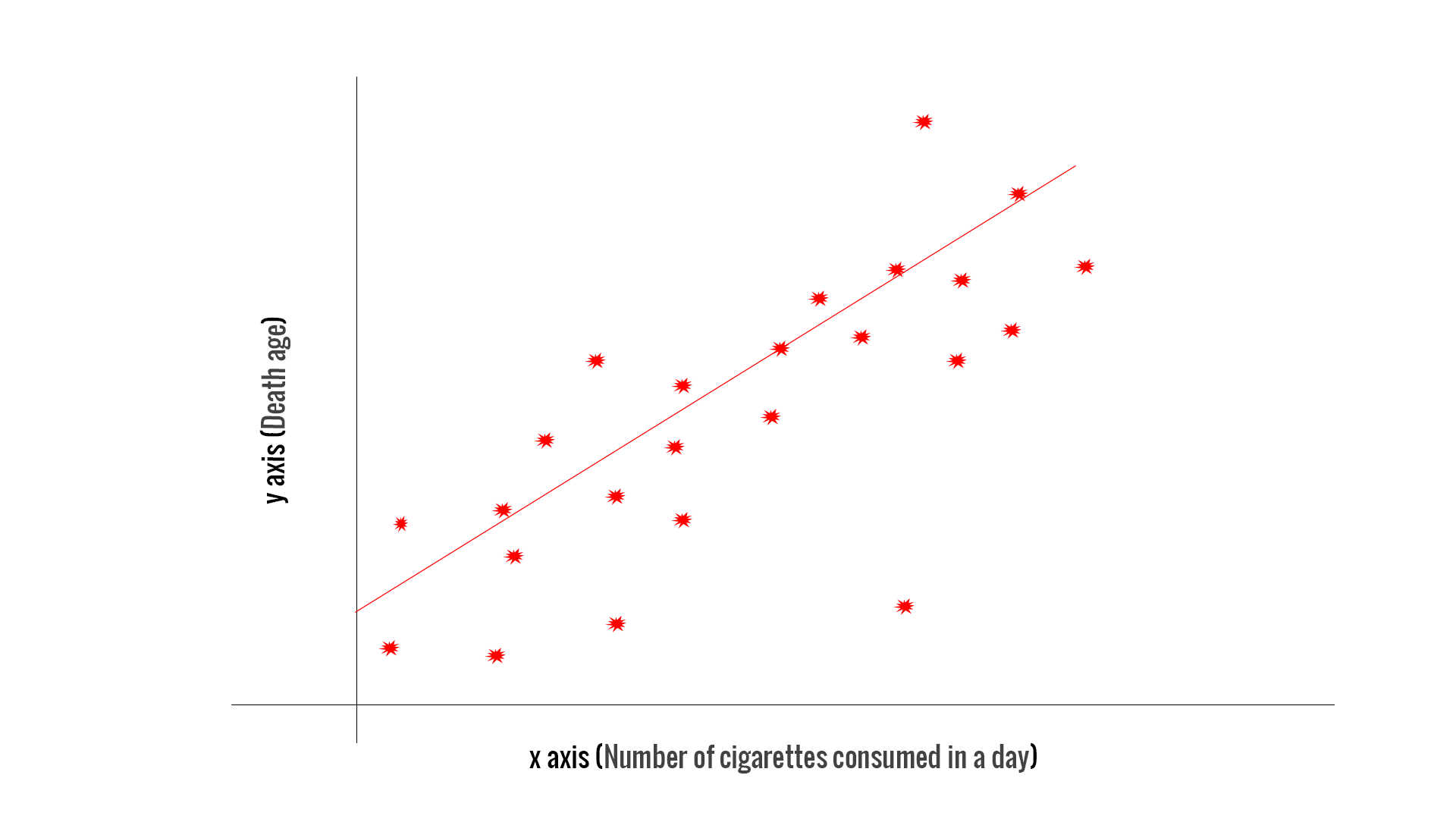

Linear Regression Model Components

Key Elements of Linear Regression

- Linear regression model describes the relationship between two variables using a straight line

- Dependent variable (Y) represents the outcome or response being predicted

- Independent variable (X) serves as the predictor or explanatory variable

- Regression line forms the best-fit line through the data points

- Slope (β1) measures the change in Y for a one-unit increase in X

- Y-intercept (β0) indicates the predicted value of Y when X equals zero

Mathematical Representation

- Linear regression equation:

- β0 and β1 are population parameters estimated from sample data

- ε represents the error term, accounting for unexplained variation

- Estimated regression equation:

- b0 and b1 are sample estimates of β0 and β1

- Ŷ denotes the predicted value of Y for a given X

Interpreting Regression Components

- Positive slope indicates a direct relationship between X and Y

- Negative slope signifies an inverse relationship between X and Y

- Slope magnitude reflects the strength of the relationship

- Y-intercept may have practical meaning in some contexts (initial value when X = 0)

- Y-intercept can be meaningless or extrapolated beyond the data range in other cases

Residuals and Estimation

Understanding Residuals

- Residuals measure the difference between observed and predicted Y values

- Residual formula:

- Positive residuals indicate underestimation by the model

- Negative residuals suggest overestimation by the model

- Residual plot helps visualize model fit and detect patterns

Least Squares Estimation

- Sum of squared residuals (SSR) quantifies the total squared deviation from the regression line

- SSR formula:

- Ordinary least squares (OLS) method minimizes the SSR to find the best-fitting line

- OLS estimates b0 and b1 to produce the smallest possible SSR

- Best linear unbiased estimator (BLUE) property ensures OLS estimates have minimum variance

Calculating Regression Coefficients

- Slope estimate:

- Y-intercept estimate:

- \bar{X} and \bar{Y} represent the means of X and Y, respectively

- These formulas provide point estimates for the regression coefficients

Model Evaluation Metrics

Assessing Model Fit

- Coefficient of determination (R-squared) measures the proportion of variance explained by the model

- R-squared formula:

- SST represents the total sum of squares:

- R-squared ranges from 0 to 1, with higher values indicating better fit

- Standard error of estimate (SEE) quantifies the average deviation of observed Y values from the regression line

- SEE formula:

Confidence and Prediction Intervals

- Prediction interval provides a range for individual Y values at a given X

- Prediction interval accounts for both model uncertainty and individual variation

- Confidence interval estimates the range for the mean Y value at a given X

- Confidence interval reflects only model uncertainty, not individual variation

- Both intervals widen as X moves away from \bar{X}, indicating increased uncertainty

Interpreting Model Performance

- Low R-squared suggests weak explanatory power of the independent variable

- High R-squared indicates strong relationship between X and Y

- Small SEE implies more precise predictions

- Large SEE suggests less accurate predictions

- Narrow confidence and prediction intervals indicate more reliable estimates

- Wide intervals suggest less precise estimates and potential need for model improvement