Segment disclosures provide crucial insights into a company's performance across different business units or geographic areas. This information helps investors and analysts understand how various parts of the business contribute to overall results and assess potential risks and opportunities.

Companies must identify reportable segments based on internal organizational structure and financial reporting. They're required to disclose specific information about each segment's revenues, profits, assets, and other key metrics, as well as provide entity-wide disclosures about products, geographic areas, and major customers.

Defining reportable segments

- Reportable segments are distinct components of a company that engage in business activities from which they may earn revenues and incur expenses

- Segment managers are held accountable for the operating results and are responsible for allocating resources within their segment

- Reportable segments are determined based on the management approach, which considers how the company is organized and how financial information is reported internally

Quantitative thresholds for segments

- A segment must meet certain quantitative thresholds to be considered reportable

- The segment's reported revenue, including both sales to external customers and intersegment sales or transfers, should be 10% or more of the combined revenue of all operating segments

- The absolute amount of the segment's reported profit or loss should be 10% or more of the greater, in absolute amount, of either the combined reported profit of all operating segments that did not report a loss or the combined reported loss of all operating segments that reported a loss

- The segment's assets should be 10% or more of the combined assets of all operating segments

Management approach to segmentation

- The management approach focuses on how management organizes the company for making operating decisions and assessing performance

- Segments are identified based on the structure of the company's internal organization and financial reporting system

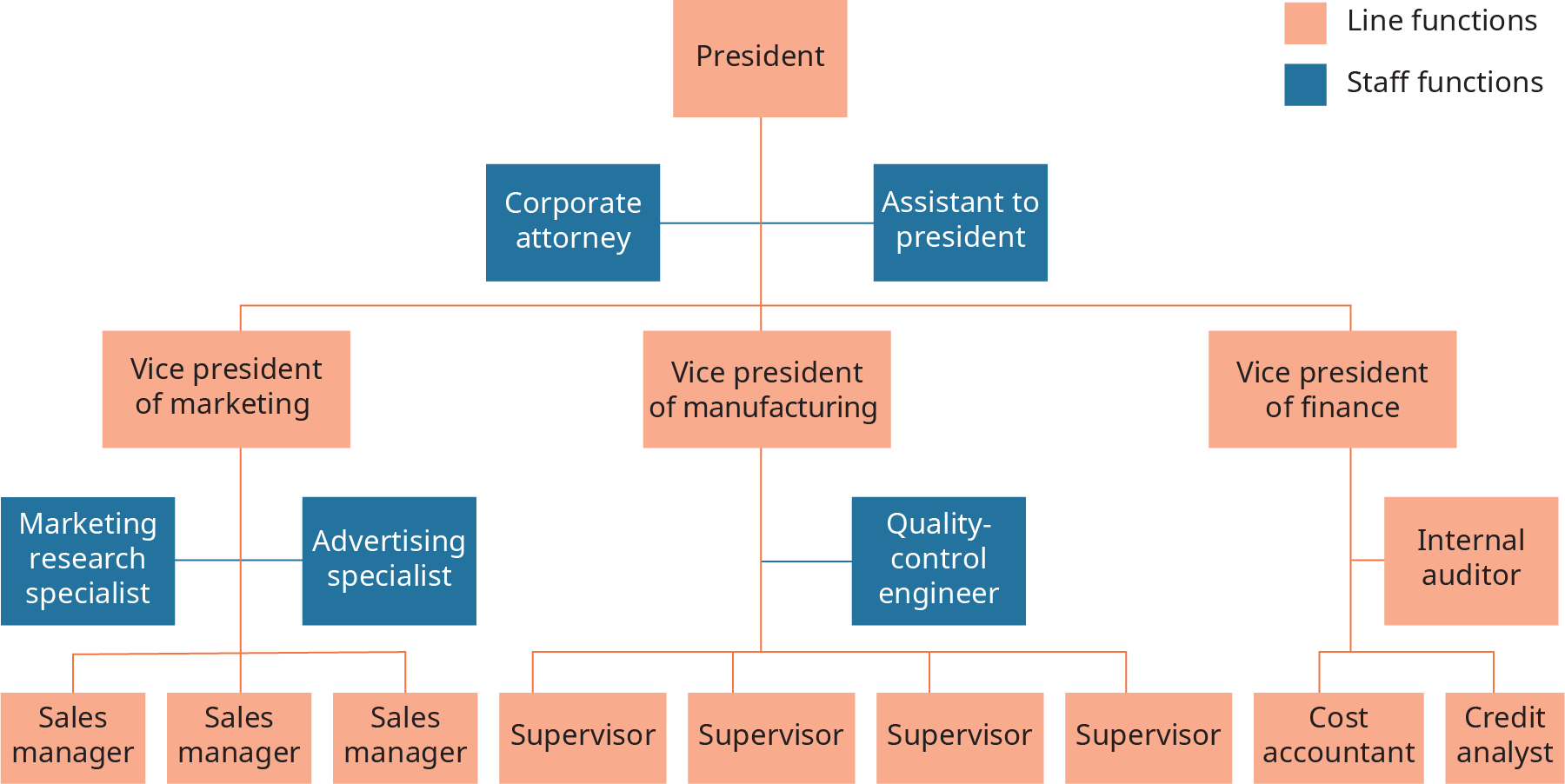

Organizational structure considerations

- The company's organizational structure, such as divisions, departments, or subsidiaries, is considered when identifying reportable segments

- Segments may be based on products and services, geographic areas, regulatory environments, or a combination of factors

Internal reporting practices

- The identification of reportable segments is based on the regular internal financial reports reviewed by the chief operating decision maker (CODM)

- The CODM is the function or individual responsible for allocating resources and assessing the performance of the operating segments

Required segment disclosures

- Companies are required to disclose certain information about their reportable segments in the notes to the financial statements

General information

- Description of the factors used to identify the reportable segments, including the basis of organization and types of products and services

- Information about how the operating segments were determined and aggregated

Profit or loss amounts

- Measure of profit or loss for each reportable segment

- Basis of accounting for any transactions between reportable segments

- Reconciliation of the total of the reportable segments' measures of profit or loss to the company's consolidated income before income taxes and discontinued operations

Assets and liabilities

- Total assets for each reportable segment if such amounts are regularly provided to the CODM

- Total liabilities for each reportable segment if such amounts are regularly provided to the CODM

Reconciliations to financial statements

- Reconciliations of the totals of the reportable segments' revenues, measures of profit or loss, assets, liabilities, and other significant items to corresponding items in the company's consolidated financial statements

Aggregation criteria for segments

- Operating segments may be combined into a single reportable segment if aggregation is consistent with the objective and basic principles of segment reporting

- Aggregated segments must have similar economic characteristics and be similar in terms of the nature of products and services, the nature of the production process, the type or class of customer, the methods used to distribute the products or provide the services, and the nature of the regulatory environment

Changes in reportable segments

- If there are changes in the structure of the company's internal organization that cause the composition of its reportable segments to change, the corresponding information for prior periods should be restated

Restatement of prior periods

- Prior period segment information should be restated to conform to the current period's segment structure unless it is impracticable to do so

- If prior periods are not restated, segment information for the current period should be reported on both the old basis and the new basis of segmentation in the year in which the change occurs

Entity-wide disclosures

- In addition to segment-specific disclosures, companies are required to provide entity-wide disclosures about their products and services, geographic areas, and major customers

Products and services

- Revenues from external customers for each product and service or each group of similar products and services (unless impracticable)

Geographic areas

- Revenues from external customers attributed to the company's country of domicile and attributed to all foreign countries in total

- Revenues from external customers attributed to an individual foreign country, if material

- Long-lived assets other than financial instruments, deferred tax assets, post-employment benefit assets, and rights arising under insurance contracts located in the company's country of domicile and located in all foreign countries in total

- Long-lived assets in an individual foreign country, if material

Major customers

- Information about major customers, including the total amount of revenues from each major customer and the identity of the segment(s) reporting the revenues (if revenues from a single external customer amount to 10% or more of the company's total revenues)

Segment reporting examples

- Companies may have different levels of complexity in their segment reporting, depending on their organizational structure and internal reporting practices

Single vs multiple segments

- A company with a single reportable segment will have limited segment disclosures, focusing primarily on entity-wide disclosures

- Companies with multiple reportable segments will provide more extensive segment-specific disclosures, including information about each segment's revenues, profit or loss, assets, and liabilities

Auditing segment disclosures

- Auditors are responsible for evaluating the appropriateness and adequacy of a company's segment disclosures

- Auditors should consider the consistency of segment information with other parts of the financial statements and their understanding of the company's business

- Auditors may perform procedures such as inquiries of management, analytical procedures, and tests of details to assess the reliability and completeness of segment information

Segment disclosures vs disaggregated revenue

- Segment disclosures provide information about a company's reportable segments, which are determined based on the management approach and internal reporting structure

- Disaggregated revenue disclosures, as required by ASC 606 (Revenue from Contracts with Customers), provide information about the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers

- While there may be overlap between segment disclosures and disaggregated revenue disclosures, they serve different purposes and are based on different criteria