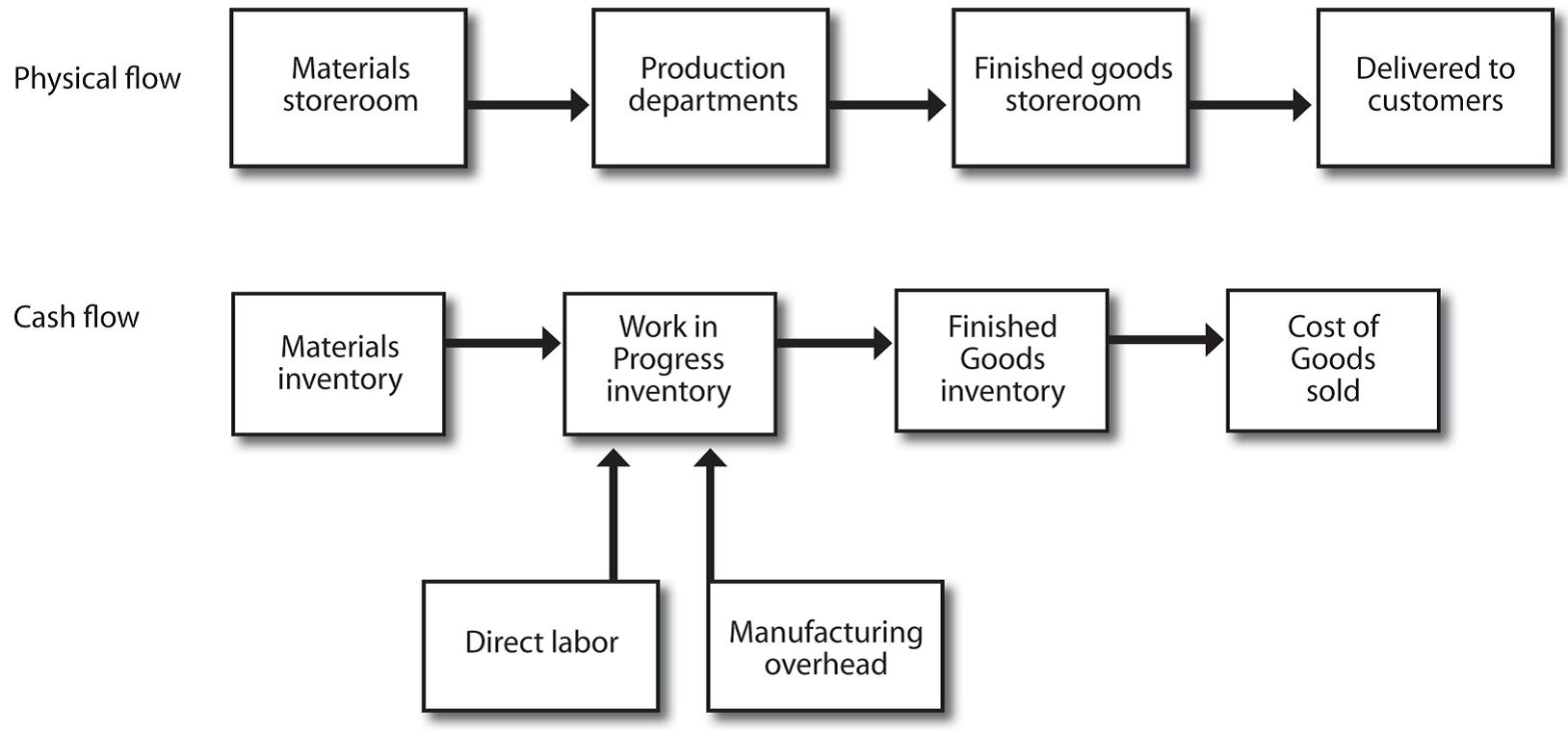

Job order costing and process costing are two key approaches to tracking production costs. Job order costing is used for unique, customized products, accumulating costs for each job separately. Process costing is used for standardized products made in continuous processes, accumulating costs by department or process.

These costing methods differ in how they track and assign costs. Job order costing uses job cost sheets and traces costs directly to specific jobs. Process costing averages costs over total units produced in each process. Understanding these approaches helps managers choose the right method for their production environment.

Job Order Costing vs Process Costing

Characteristics of costing systems

- Job order costing

- Tracks costs for unique, customized products or services (custom furniture, construction projects)

- Accumulates costs separately for each individual job or batch

- Fits companies with diverse product lines or customer-specific orders (printing services, automotive repair shops)

- Process costing

- Tracks costs for homogeneous, standardized products manufactured in a continuous process (oil refining, chemical manufacturing)

- Accumulates costs for each process or department over a specific time period

- Fits companies with mass production of similar products (food processing, textile manufacturing)

Cost tracking in costing methods

- Job order costing

- Uses job cost sheets to accumulate and assign costs to specific jobs

- Traces direct materials and direct labor costs directly to individual jobs (cost tracing)

- Allocates overhead costs to jobs using a predetermined overhead rate

- Maintains work-in-process inventory for each job until completion

- Process costing

- Accumulates and assigns costs to departments or processes for a specific time period

- Averages costs over the total units produced in each process

- Employs equivalent units of production (EUP) to allocate costs to partially completed units

- Transfers costs from one process to another until the products are completed

Applications of costing approaches

- Job order costing suits situations with

- Unique, customized, or made-to-order products or services (custom cabinetry, wedding cakes)

- Intermittent or non-continuous production

- Examples: aircraft manufacturing, custom software development

- Process costing suits situations with

- Homogeneous products produced in large quantities (gasoline, breakfast cereal)

- Continuous production following a standardized process (production flow)

- Examples: beer brewing, cement production

Cost Accumulation and Assignment

- Cost accumulation: The process of collecting cost data in an organized way

- Cost assignment: The process of attributing costs to cost objects

- Cost pools: Groups of individual cost items that are allocated together (e.g., manufacturing overhead)

- Cost allocation: The process of assigning indirect costs to cost objects using cost drivers

- Cost drivers: Factors that cause a change in the cost of an activity (e.g., machine hours, direct labor hours)