Estimating variable and fixed costs is crucial for understanding how expenses change with activity levels. The high-low method and scatter graphs help managers analyze cost behavior and create cost equations for predicting future expenses.

These tools enable businesses to make informed decisions about pricing, resource allocation, and capacity planning. By accurately estimating costs, companies can better forecast budgets, perform break-even analysis, and evaluate the impact of changing activity levels on total costs.

Estimating Variable and Fixed Costs

High-low method for cost estimation

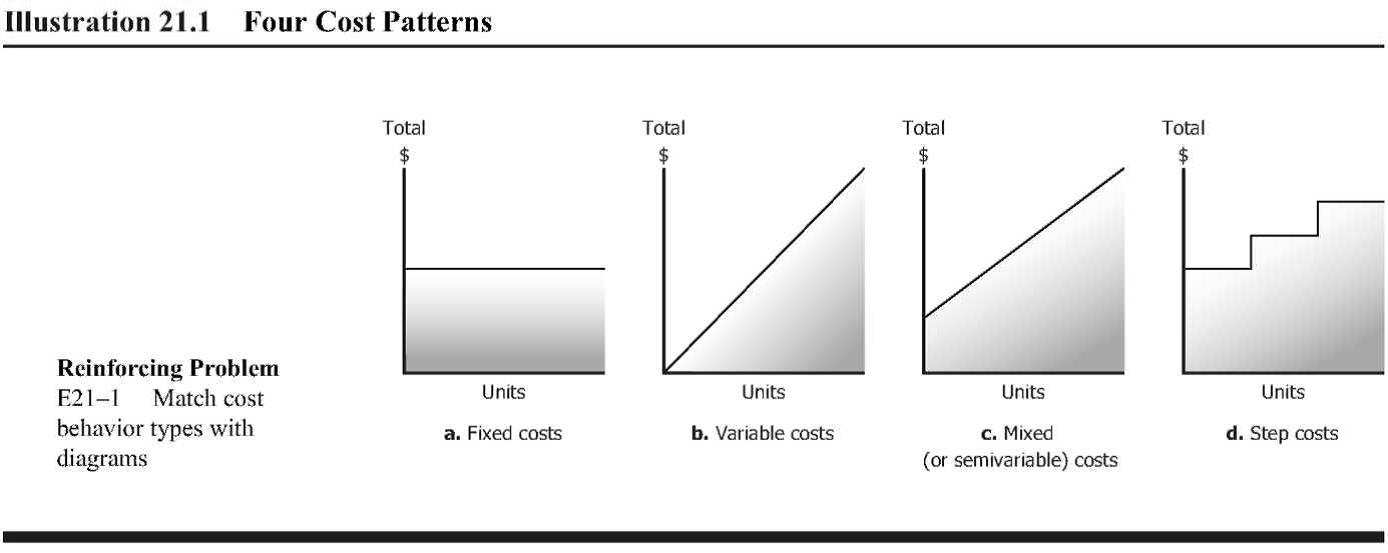

- Mixed costs contain both variable and fixed cost elements (labor costs with overtime pay)

- High-low method estimates variable and fixed components of mixed costs

- Identify periods with highest and lowest activity levels (machine hours, units produced)

- Determine total costs for highest and lowest activity periods

- Calculate variable cost per unit using formula:

- Calculate total fixed cost using highest or lowest activity level and corresponding total cost:

- Resulting cost equation:

- Predict future costs by inputting different activity levels into cost equation (production volumes, service hours)

- Consider the relevant range when applying the cost equation to ensure accuracy

Scatter graphs and cost relationships

- Scatter graph visually represents relationship between costs and activity levels

- Activity levels plotted on x-axis (labor hours, units produced)

- Total costs plotted on y-axis

- Each data point represents total cost at specific activity level

- Linear pattern suggests linear relationship between costs and activity

- Straight line approximates cost behavior (upward sloping for increasing costs)

- Non-linear pattern indicates cost behavior is not linear

- High-low method may not be appropriate (curvilinear, exponential relationships)

- Scatter graphs help identify cost drivers that influence total costs

Cost equations in business applications

- Cost equation from high-low method calculates total costs at different activity levels

- Manufacturing businesses:

- Activity levels include machine hours, labor hours, units produced

- Estimate total production costs at different output levels (batch sizes, production runs)

- Service businesses:

- Activity levels include service hours, customers served, transactions processed

- Estimate total service costs at different activity levels (consulting projects, customer support)

- Managers use cost equations to:

- Predict future costs based on expected activity (budgeting, forecasting)

- Make decisions on pricing, resource allocation, capacity planning (break-even analysis)

- Evaluate impact of activity level changes on total costs (sensitivity analysis)

Advanced Cost Estimation Techniques

- Regression analysis provides a more sophisticated method for estimating cost equations

- Least squares method minimizes the sum of squared differences between actual and predicted costs

- Cost behavior patterns can be analyzed to understand how costs change with activity levels

- Identifying appropriate cost drivers is crucial for accurate cost estimation and decision-making