Modern Portfolio Theory revolutionized investing by showing how diversification can maximize returns while minimizing risk. It's the foundation for smart asset allocation, teaching us to look at our whole portfolio instead of individual investments.

This theory assumes investors are rational and risk-averse, aiming to optimize their portfolios. It introduces key concepts like the efficient frontier and optimal portfolios, which help us understand the trade-offs between risk and return in our investment choices.

Modern Portfolio Theory Principles

Key Insights and Assumptions

- MPT is a framework for constructing and selecting portfolios based on maximizing expected return for a given level of market risk

- Emphasizes diversification to reduce risk

- An asset's risk and return should not be assessed in isolation, but by how it contributes to a portfolio's overall risk and return

- Correlation between assets is a key factor

- Investors are assumed to be rational, risk-averse, and seeking to maximize satisfaction from returns on their investments

- Investors should select portfolios that maximize returns for a given level of risk

Relevant Risks and Measures

- Market risk (systematic risk) is the only relevant risk because diversification eliminates asset-specific (idiosyncratic) risk

- Beta measures an asset's sensitivity to market risk

- The Capital Asset Pricing Model (CAPM) emerges from MPT

- Describes the relationship between systematic risk and expected return for assets, particularly stocks

Efficient Frontier and Optimal Portfolios

Defining the Efficient Frontier

- The efficient frontier is a set of optimal portfolios that offer the highest expected return for a defined level of risk or the lowest risk for a given level of expected return

- Optimal portfolios that comprise the efficient frontier tend to have a higher degree of diversification

- Investors should only select from these optimal portfolios

Calculating Efficient Portfolios

- To calculate the efficient frontier, the expected return and volatility (standard deviation) for each asset must be estimated, as well as the covariance (correlation) between assets

- Quadratic programming or the critical line algorithm can be used to calculate the asset compositions of portfolios on the efficient frontier at various levels of risk

- The tangency portfolio is the optimal portfolio of risky assets on the efficient frontier

- Combining this with the risk-free asset creates the Capital Market Line

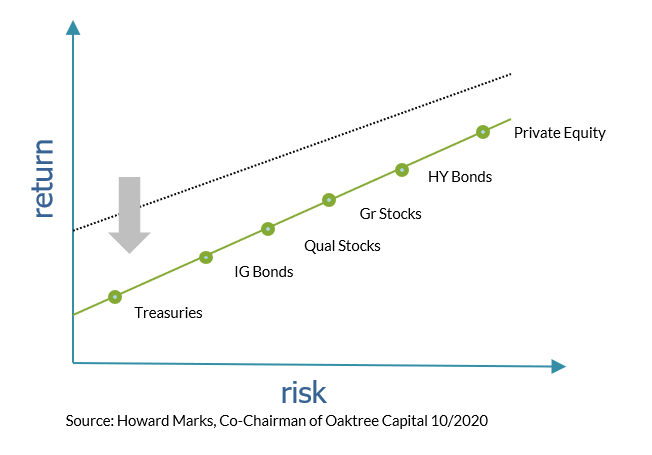

Risk vs Return in Portfolio Selection

The Risk-Return Trade-off

- Risk and return are positively correlated

- Assets with higher expected returns generally have higher risk (volatility)

- Investors must determine their risk tolerance when selecting portfolios

- The Sharpe ratio measures risk-adjusted return - how much return is achieved per unit of risk

- Optimal portfolios will have the highest Sharpe ratios

Investor Utility and Portfolio Choice

- The Capital Market Line (CML) is comprised of portfolios with optimal combinations of the risk-free asset and tangency portfolio

- Investors should select portfolios on the CML based on their risk preference

- Risk aversion refers to an investor's reluctance to accept a bargain with an uncertain payoff rather than another bargain with a more certain, but possibly lower, expected payoff

- More risk-averse investors will select portfolios with lower volatility

- Utility theory states that investors will choose the portfolio that maximizes their expected utility given their level of risk aversion

- Indifference curves can depict an equal level of utility for different combinations of risk and return

MPT Assumptions vs Real-World Investing

Limitations of Statistical Assumptions

- MPT assumes that asset returns follow a Gaussian distribution, but asset returns tend to have fat tails

- This means MPT may underestimate risk, especially risk of extreme events (market crashes)

- Estimating expected returns, volatilities, and correlations of assets is challenging and subject to error

- Small changes in inputs can lead to large differences in the efficient frontier and portfolio weights

Investor Behavior and Market Inefficiencies

- Investors are not always rational and risk-averse as assumed

- Behavioral biases such as loss-aversion, overconfidence, and herd mentality can impact investment decisions

- MPT assumes that markets are efficient, but real-world markets can exhibit inefficiencies, especially in the short term

- Arbitrage opportunities may exist (mispriced assets)

Practical Constraints and Additional Risks

- Transaction costs, taxes, and liquidity constraints can impact the practical implementation of MPT portfolios

- Frequent rebalancing to maintain an optimal portfolio may be costly

- Other risk factors besides market risk, such as inflation risk, credit risk, and liquidity risk, are not accounted for in MPT

- These risks may be relevant for some investors (long-term investors, bond investors)