🎳Intro to Econometrics Unit 8 Review

8.4 Moving average models

8.4 Moving average models

Unit & Topic Study Guides

Probability & Statistics Fundamentals

Linear Regression: Simple and Multiple

Econometric Model Design

Gauss-Markov Assumptions & OLS Properties

Hypothesis Tests & Confidence Intervals

Dummy Variables & Selection Models

Multicollinearity & Heteroskedasticity

Autocorrelation in Time Series Analysis

Instrumental Variables & Two-Stage LS

Panel Data Models & Fixed Effects

Limited Dependent Variable Models

Econometric Software: Tools and Applications

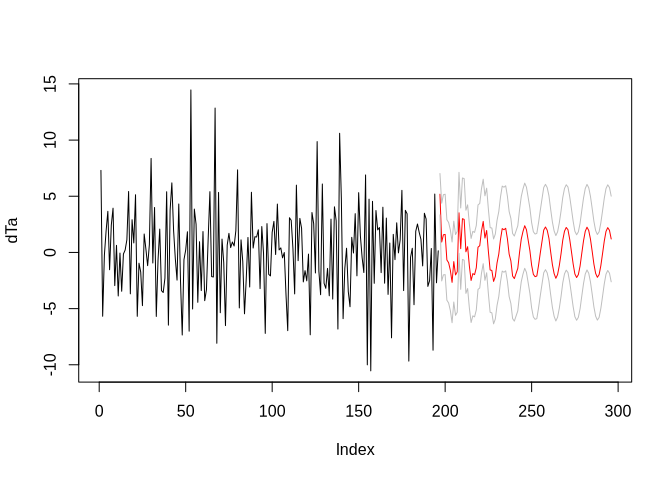

Moving average models are a crucial tool in time series analysis, capturing dependencies between observations and forecast errors. These models express current values as linear combinations of current and past forecast errors, with different types like simple, weighted, and exponential moving averages.

MA models are always stationary and have distinct autocorrelation patterns. They're estimated using methods like maximum likelihood and can be selected using criteria like AIC and BIC. MA models are useful for forecasting, especially in econometrics, but have limitations in capturing long-term trends or seasonality.

Definition of moving average models

- Moving average (MA) models are a class of time series models used to capture the dependence between an observation and a residual error from a moving average model applied to lagged observations

- MA models express the current value of a time series as a linear combination of the current and past forecast errors (also known as white noise or innovations)

- The order of an MA model, denoted as MA(q), indicates the number of lagged forecast errors included in the model

Types of moving average models

Simple moving average

- A simple moving average (SMA) model assigns equal weights to each observation in the moving average window

- The SMA is calculated by taking the arithmetic mean of a fixed number of past observations

- Example: A 5-day SMA would be calculated as , where is the price at time

Weighted moving average

- A weighted moving average (WMA) model assigns different weights to each observation in the moving average window, typically giving more weight to recent observations

- The weights are usually chosen based on the importance or relevance of each observation

- Example: A 3-day WMA with weights (0.5, 0.3, 0.2) would be calculated as

Exponential moving average

- An exponential moving average (EMA) model assigns exponentially decreasing weights to older observations, giving more importance to recent observations

- The weighting factor, known as the smoothing factor (), determines the rate at which the weights decrease over time

- The EMA is calculated recursively using the formula: , where

Characteristics of moving average processes

Stationarity

- A moving average process is always stationary, as it is a linear combination of white noise terms, which are stationary by definition

- Stationarity implies that the mean, variance, and autocovariance of the process do not change over time

Autocorrelation function

- The autocorrelation function (ACF) of a moving average process cuts off after lag q, where q is the order of the MA model

- The ACF measures the correlation between observations separated by a given lag

- For an MA(q) process, the ACF will be non-zero for lags up to q and zero for lags greater than q

Partial autocorrelation function

- The partial autocorrelation function (PACF) of a moving average process decays gradually, often exhibiting a sinusoidal or exponential decay pattern

- The PACF measures the correlation between observations separated by a given lag, while controlling for the effects of intermediate lags

- The PACF can be used to identify the order of an MA model, as it will have significant values at lags up to the order of the model

Estimation of moving average models

Method of moments

- The method of moments is a simple approach to estimate the parameters of an MA model

- It involves equating the sample moments (mean, variance, and autocovariances) to their theoretical counterparts and solving for the model parameters

- The method of moments is less efficient than maximum likelihood estimation but is computationally simpler

Maximum likelihood estimation

- Maximum likelihood estimation (MLE) is a more efficient method for estimating the parameters of an MA model

- MLE involves finding the parameter values that maximize the likelihood function, which measures the probability of observing the given data under the assumed model

- MLE requires numerical optimization techniques and is computationally more intensive than the method of moments

Order selection for moving average models

Akaike information criterion (AIC)

- The Akaike information criterion (AIC) is a model selection criterion that balances the goodness of fit with the complexity of the model

- AIC is calculated as , where is the number of parameters and is the maximum likelihood value

- The model with the lowest AIC value is considered the best among the competing models

Bayesian information criterion (BIC)

- The Bayesian information criterion (BIC), also known as the Schwarz criterion, is another model selection criterion similar to AIC

- BIC penalizes model complexity more heavily than AIC, favoring more parsimonious models

- BIC is calculated as , where is the sample size

- Like AIC, the model with the lowest BIC value is preferred

Forecasting with moving average models

One-step-ahead forecasts

- One-step-ahead forecasts predict the value of the time series one period into the future

- For an MA(q) model, the one-step-ahead forecast is given by , where is the mean of the process, are the MA coefficients, and are the forecast errors

- The forecast errors for future periods are assumed to be zero, as they are unknown at the time of forecasting

Multi-step-ahead forecasts

- Multi-step-ahead forecasts predict the values of the time series multiple periods into the future

- For an MA(q) model, the multi-step-ahead forecasts are equal to the mean of the process for all horizons beyond q

- This is because the MA process has a finite memory, and the effect of the current and past forecast errors diminishes after q periods

- The multi-step-ahead forecast for an MA(q) model at horizon h > q is given by

Invertibility of moving average models

- A moving average model is said to be invertible if it can be expressed as an infinite-order autoregressive (AR) model

- Invertibility is a desirable property because it ensures that the model has a unique representation and can be used for forecasting

- For an MA(q) model to be invertible, the roots of the characteristic equation must lie outside the unit circle in the complex plane

Moving average models vs autoregressive models

- Moving average (MA) models and autoregressive (AR) models are two fundamental classes of time series models

- MA models express the current value of a time series as a linear combination of the current and past forecast errors, while AR models express the current value as a linear combination of past values of the series

- MA models have a finite memory and are always stationary, while AR models have an infinite memory and can be either stationary or non-stationary

- In practice, many time series exhibit both MA and AR characteristics, leading to the development of combined ARMA models

Applications of moving average models

Time series data analysis

- Moving average models are widely used in analyzing time series data across various fields, such as economics, finance, and environmental sciences

- They can be used to model and forecast a wide range of time series, including stock prices, exchange rates, inflation rates, and weather variables

- MA models are particularly useful for capturing short-term dependencies and smoothing out noise in the data

Econometric modeling

- In econometrics, moving average models are often used in conjunction with autoregressive models to build ARMA or ARIMA (autoregressive integrated moving average) models

- These models are used to analyze and forecast economic variables, such as GDP growth, unemployment rates, and consumer prices

- MA models can help capture the impact of random shocks or innovations on the economic system

Limitations of moving average models

- Moving average models are not suitable for capturing long-term trends or seasonality in the data, as they focus on short-term dependencies

- MA models assume that the series is stationary, which may not always be the case in practice. Non-stationary series may require differencing or other transformations before fitting an MA model

- The invertibility condition for MA models can be restrictive, limiting the range of possible parameter values

- MA models may not be the best choice for series with strong autocorrelation at longer lags, as they have a finite memory and may not capture long-range dependencies effectively

Extensions of moving average models

Autoregressive moving average (ARMA) models

- Autoregressive moving average (ARMA) models combine the features of both AR and MA models

- An ARMA(p, q) model includes p autoregressive terms and q moving average terms

- ARMA models can capture a wider range of time series patterns and are more flexible than pure AR or MA models

- The order of an ARMA model can be determined using model selection criteria like AIC or BIC

Seasonal moving average models

- Seasonal moving average (SMA) models are an extension of MA models that incorporate seasonal patterns in the data

- An SMA(Q) model includes Q seasonal moving average terms, where Q is the number of periods per season (e.g., Q=12 for monthly data with a yearly seasonal cycle)

- SMA models can be combined with non-seasonal MA terms to form a multiplicative seasonal ARIMA (SARIMA) model

- SARIMA models are useful for modeling and forecasting time series with both short-term dependencies and seasonal patterns