🎳Intro to Econometrics Unit 3 Review

3.3 Omitted variable bias

3.3 Omitted variable bias

Unit & Topic Study Guides

Probability & Statistics Fundamentals

Linear Regression: Simple and Multiple

Econometric Model Design

Gauss-Markov Assumptions & OLS Properties

Hypothesis Tests & Confidence Intervals

Dummy Variables & Selection Models

Multicollinearity & Heteroskedasticity

Autocorrelation in Time Series Analysis

Instrumental Variables & Two-Stage LS

Panel Data Models & Fixed Effects

Limited Dependent Variable Models

Econometric Software: Tools and Applications

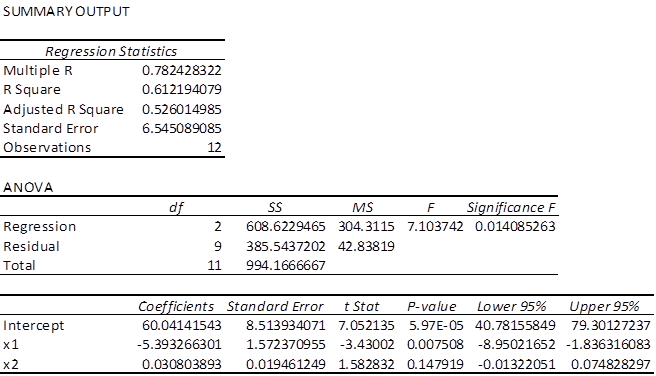

Omitted variable bias is a critical issue in econometrics that can lead to inaccurate estimates and flawed conclusions. It occurs when a relevant explanatory variable is left out of a regression model, causing bias in the coefficients of included variables.

Understanding omitted variable bias is crucial for conducting reliable econometric analyses. This topic explores its definition, consequences, detection methods, and strategies for addressing and preventing it in various data contexts.

Definition of omitted variable bias

- Occurs when a relevant explanatory variable is excluded from a regression model

- The omitted variable is correlated with both the dependent variable and one or more included explanatory variables

- Leads to biased and inconsistent estimates of the coefficients for the included explanatory variables

- The bias can be positive or negative, depending on the direction of the correlations

Consequences of omitted variables

Biased coefficient estimates

- The estimated coefficients for the included explanatory variables will be biased

- The bias can lead to incorrect conclusions about the magnitude and direction of the relationships between the variables

- The bias can also affect the statistical significance of the estimated coefficients

- The direction of the bias depends on the correlations between the omitted variable and the included explanatory variables

Incorrect model specification

- Omitting a relevant variable results in a misspecified model

- The model may not accurately represent the true relationships between the variables

- The model may have poor predictive power and may not fit the data well

- Misspecification can lead to incorrect policy recommendations or business decisions

Detecting omitted variable bias

Residual plots vs explanatory variables

- Plotting the residuals against each explanatory variable can reveal patterns or trends

- If there is a systematic relationship between the residuals and an explanatory variable, it may indicate the presence of an omitted variable

- A non-random pattern in the residual plot suggests that the model is misspecified and that an important variable has been omitted

Correlation between error term and regressors

- In a correctly specified model, the error term should be uncorrelated with the explanatory variables

- If there is a correlation between the error term and one or more explanatory variables, it may indicate the presence of an omitted variable

- Testing for correlation between the error term and the regressors can help detect omitted variable bias (Durbin-Watson test, Breusch-Godfrey test)

Addressing omitted variable bias

Including relevant variables

- The most straightforward way to address omitted variable bias is to include the omitted variable in the model

- This requires identifying the omitted variable and collecting data on it

- Including the relevant variable can eliminate the bias and improve the model's accuracy

- However, it may not always be possible to include the omitted variable due to data limitations or measurement difficulties

Proxy variables for unobservable factors

- When the omitted variable is unobservable or difficult to measure, a proxy variable can be used instead

- A proxy variable is a measurable variable that is correlated with the omitted variable

- Including a proxy variable can reduce the omitted variable bias, although it may not eliminate it completely

- Examples of proxy variables: using education level as a proxy for ability, using age as a proxy for work experience

Instrumental variables approach

- An instrumental variable (IV) is a variable that is correlated with the explanatory variable but not with the error term

- The IV approach involves using the instrumental variable to estimate the effect of the explanatory variable on the dependent variable

- This approach can provide consistent estimates of the coefficients even in the presence of omitted variable bias

- Finding a suitable instrumental variable can be challenging, as it must satisfy the relevance and exogeneity conditions

Omitted variable bias vs multicollinearity

Differences in bias direction

- Omitted variable bias can lead to either overestimation or underestimation of the coefficients, depending on the correlations between the omitted variable and the included explanatory variables

- Multicollinearity, which occurs when explanatory variables are highly correlated with each other, typically leads to larger standard errors and less precise estimates of the coefficients

- While omitted variable bias affects the consistency of the estimates, multicollinearity affects the efficiency of the estimates

Implications for model interpretation

- Omitted variable bias can lead to incorrect conclusions about the relationships between the variables and the effectiveness of policy interventions

- Multicollinearity can make it difficult to distinguish the individual effects of the correlated explanatory variables on the dependent variable

- In the presence of multicollinearity, the coefficients may be sensitive to small changes in the data or the model specification

- Addressing omitted variable bias is crucial for obtaining reliable estimates, while addressing multicollinearity is important for precise interpretation of the coefficients

Examples of omitted variable bias

In cross-sectional data analysis

- Estimating the effect of education on earnings without controlling for ability: If ability is correlated with both education and earnings, omitting ability from the model will lead to biased estimates of the return to education

- Analyzing the impact of advertising on sales without accounting for product quality: If higher-quality products tend to have both higher advertising expenditures and higher sales, omitting product quality from the model will overestimate the effect of advertising on sales

In time series data analysis

- Modeling the relationship between crime rates and unemployment without controlling for demographic changes: If demographic factors (age structure, population density) are correlated with both crime rates and unemployment, omitting these factors will result in biased estimates of the effect of unemployment on crime

- Examining the impact of monetary policy on economic growth without considering fiscal policy: If changes in fiscal policy (government spending, tax rates) are correlated with both monetary policy and economic growth, omitting fiscal policy variables will lead to biased estimates of the effect of monetary policy on growth

Strategies to prevent omitted variables

Careful model specification

- Researchers should carefully consider the potential determinants of the dependent variable and include all relevant explanatory variables in the model

- Economic theory, previous research, and institutional knowledge can guide the selection of variables to include in the model

- Conducting sensitivity analyses by adding or removing variables can help assess the robustness of the results to different model specifications

Thorough literature review

- Reviewing the existing literature on the topic can help identify important variables that have been found to influence the dependent variable

- Researchers should consider the variables used in previous studies and assess their relevance for the current analysis

- Meta-analyses and systematic reviews can provide valuable insights into the key determinants of the dependent variable and guide model specification

Subject matter expertise

- Consulting with subject matter experts, such as economists, policymakers, or industry professionals, can help identify important variables that may be overlooked

- Experts can provide insights into the underlying mechanisms and relationships between the variables

- Collaborating with experts from different fields (psychology, sociology, etc.) can help incorporate relevant variables from other disciplines that may influence the dependent variable

- Engaging with stakeholders and practitioners can help ensure that the model captures the most important factors affecting the outcome of interest