Understanding cost structure and breakeven analysis is crucial for entrepreneurs. These tools help you grasp how costs impact your business and when you'll start making a profit. By analyzing fixed and variable costs, you can make smart decisions about pricing and production.

Breakeven analysis shows you the sales volume needed to cover all costs. It helps set realistic goals and evaluate profitability. While it has limitations, breakeven analysis is a valuable tool for financial planning and decision-making in your entrepreneurial journey.

Components of cost structure

- Understanding the various components of a company's cost structure is crucial for effective financial management and decision-making in entrepreneurship

- The cost structure refers to the types and relative proportions of fixed and variable costs that a business incurs

- Analyzing the cost structure helps entrepreneurs identify areas for cost optimization and improve profitability

Fixed vs variable costs

- Fixed costs remain constant regardless of the level of production or sales volume (rent, salaries, insurance)

- Variable costs fluctuate directly with the level of production or sales (raw materials, packaging, shipping)

- Understanding the mix of fixed and variable costs helps entrepreneurs make informed decisions about pricing, production levels, and profitability

Direct vs indirect costs

- Direct costs are directly attributable to the production of a specific product or service (raw materials, direct labor)

- Indirect costs are not directly tied to a specific product or service but are necessary for the overall operation of the business (rent, utilities, administrative salaries)

- Allocating indirect costs accurately is important for determining the true cost of production and making pricing decisions

Economies of scale

- Economies of scale refer to the cost advantages that businesses can exploit by expanding their scale of production

- As production volume increases, fixed costs are spread over a larger number of units, reducing the average cost per unit

- Economies of scale can help businesses improve efficiency, reduce costs, and increase profitability

Cost of goods sold (COGS)

- COGS refers to the direct costs attributed to the production of the goods sold by a company

- COGS includes costs such as raw materials, direct labor, and manufacturing overhead directly related to the products sold

- Accurately calculating COGS is essential for determining gross profit margins and making pricing decisions

Operating expenses

- Operating expenses are the costs incurred in the day-to-day operations of a business

- Examples of operating expenses include salaries, rent, utilities, marketing, and administrative costs

- Monitoring and controlling operating expenses is crucial for maintaining profitability and ensuring the long-term sustainability of the business

Overhead costs

- Overhead costs are the ongoing expenses of running a business that are not directly related to creating a product or service

- Examples of overhead costs include rent, utilities, insurance, and administrative salaries

- Allocating overhead costs to products or services is important for accurate pricing and profitability analysis

Analyzing cost structure

- Analyzing the cost structure of a business is essential for making informed financial decisions and optimizing profitability

- Entrepreneurs need to understand the various components of their cost structure and how they impact the overall financial performance of the company

Importance of cost analysis

- Cost analysis helps entrepreneurs identify areas where costs can be reduced or optimized

- By understanding the cost structure, businesses can make informed decisions about pricing, production levels, and resource allocation

- Cost analysis also helps in budgeting, forecasting, and strategic planning

Identifying cost drivers

- Cost drivers are the factors that cause costs to increase or decrease

- Identifying cost drivers helps entrepreneurs understand what influences their costs and how to manage them effectively

- Examples of cost drivers include sales volume, production efficiency, raw material prices, and labor costs

Calculating unit costs

- Unit cost refers to the total cost of producing one unit of a product or service

- Calculating unit costs involves dividing the total production costs by the number of units produced

- Knowing the unit cost is crucial for setting prices, analyzing profitability, and making production decisions

Conducting sensitivity analysis

- Sensitivity analysis involves examining how changes in key variables impact the cost structure and profitability of a business

- Entrepreneurs can use sensitivity analysis to assess the impact of changes in prices, production levels, or input costs on their bottom line

- Sensitivity analysis helps identify potential risks and opportunities and enables businesses to develop contingency plans

Strategies for cost optimization

- Cost optimization involves finding ways to reduce costs without compromising the quality of products or services

- Strategies for cost optimization include negotiating better prices with suppliers, improving production efficiency, reducing waste, and optimizing inventory management

- Implementing cost optimization strategies can help businesses improve their profitability and competitiveness in the market

Breakeven analysis fundamentals

- Breakeven analysis is a crucial tool for entrepreneurs to determine the point at which their business will start generating profits

- It helps businesses understand the relationship between costs, prices, and sales volume

Definition of breakeven point

- The breakeven point is the level of sales at which a business's total revenue equals its total costs

- At the breakeven point, the company generates neither a profit nor a loss

- Knowing the breakeven point helps entrepreneurs set sales targets and make informed pricing and production decisions

Breakeven formula

- The breakeven formula calculates the number of units a business needs to sell to cover its total costs

- Breakeven quantity = Fixed costs ÷ (Price per unit - Variable cost per unit)

- The formula takes into account fixed costs, price per unit, and variable cost per unit

Contribution margin

- Contribution margin is the amount of revenue left after subtracting the variable costs of producing a product or service

- It represents the amount available to cover fixed costs and generate profit

- Contribution margin per unit = Price per unit - Variable cost per unit

Assumptions in breakeven analysis

- Breakeven analysis relies on several assumptions, such as constant fixed costs, stable variable costs per unit, and consistent pricing

- It assumes that all units produced are sold and that the sales mix remains constant

- Entrepreneurs should be aware of these assumptions and consider their limitations when interpreting the results of breakeven analysis

Conducting breakeven analysis

- To conduct a breakeven analysis, entrepreneurs need to gather information about their costs, prices, and sales volume

- The process involves several steps, including determining fixed costs, calculating variable costs per unit, setting price points, and solving for the breakeven quantity

Determining fixed costs

- Fixed costs are the expenses that remain constant regardless of the level of production or sales volume

- Examples of fixed costs include rent, salaries, insurance, and depreciation

- Identifying and accurately allocating fixed costs is crucial for conducting a reliable breakeven analysis

Calculating variable costs per unit

- Variable costs are the expenses that vary directly with the level of production or sales volume

- To calculate variable costs per unit, divide the total variable costs by the number of units produced

- Examples of variable costs include raw materials, packaging, and shipping costs

Setting price points

- Setting the right price point is crucial for achieving breakeven and generating profits

- Entrepreneurs need to consider factors such as production costs, target profit margins, and market demand when setting prices

- The price point should be high enough to cover costs and generate a profit but competitive enough to attract customers

Solving for breakeven quantity

- Once the fixed costs, variable costs per unit, and price per unit are determined, entrepreneurs can solve for the breakeven quantity using the breakeven formula

- The breakeven quantity represents the number of units that need to be sold to cover all costs and generate zero profit or loss

- Entrepreneurs can use this information to set sales targets and make production decisions

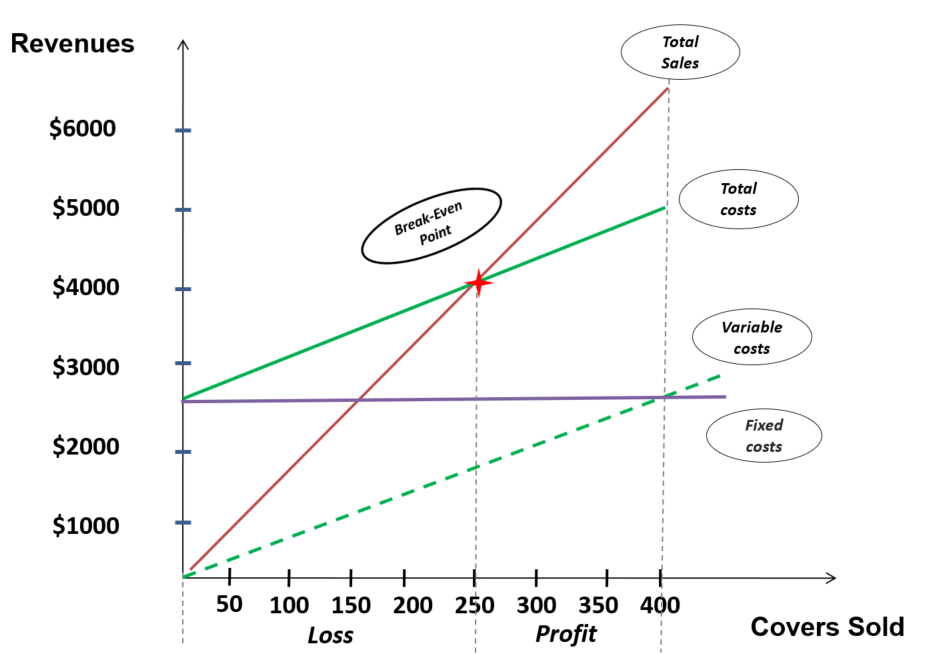

Breakeven charts and graphs

- Breakeven charts and graphs provide a visual representation of the breakeven point and the relationship between costs, revenue, and profit

- They help entrepreneurs understand how changes in prices, costs, or sales volume impact profitability

- Breakeven charts typically include lines for total revenue, total costs, and the breakeven point

Applications of breakeven analysis

- Breakeven analysis has numerous applications in entrepreneurship and business decision-making

- It can be used to evaluate profitability, compare products or services, assess the impact of price changes, determine sales targets, and make production decisions

Evaluating profitability

- Breakeven analysis helps entrepreneurs determine whether a product or service is profitable at a given price point and sales volume

- By comparing the breakeven point with the expected sales volume, businesses can assess the potential profitability of a venture

- If the expected sales volume is higher than the breakeven quantity, the business is likely to generate profits

Comparing products or services

- Breakeven analysis can be used to compare the profitability of different products or services

- By conducting separate breakeven analyses for each product or service, entrepreneurs can determine which ones are more profitable and allocate resources accordingly

- This information can help businesses optimize their product mix and focus on the most profitable offerings

Assessing impact of price changes

- Breakeven analysis allows entrepreneurs to evaluate the impact of price changes on profitability

- By adjusting the price per unit in the breakeven formula, businesses can determine how price changes affect the breakeven quantity and overall profitability

- This information can help entrepreneurs make informed pricing decisions and assess the sensitivity of their profitability to price fluctuations

Determining sales targets

- Breakeven analysis helps entrepreneurs set realistic sales targets based on their costs and desired profit margins

- By calculating the breakeven quantity and considering the desired profit margin, businesses can determine the sales volume needed to achieve their financial goals

- This information can be used to develop sales strategies, set performance targets for sales teams, and monitor progress towards achieving profitability

Making production decisions

- Breakeven analysis can inform production decisions by helping entrepreneurs determine the optimal level of production based on costs and expected demand

- By comparing the breakeven quantity with the forecasted demand, businesses can make informed decisions about production levels, inventory management, and resource allocation

- This information can help entrepreneurs optimize their production processes, minimize waste, and improve overall efficiency

Limitations of breakeven analysis

- While breakeven analysis is a valuable tool for entrepreneurs, it has certain limitations that should be considered when interpreting the results

- Understanding these limitations helps entrepreneurs make more informed decisions and avoid relying solely on breakeven analysis

Sensitivity to assumptions

- Breakeven analysis relies on several assumptions, such as constant fixed costs, stable variable costs per unit, and consistent pricing

- Changes in these assumptions can significantly impact the accuracy of the breakeven analysis

- Entrepreneurs should regularly review and update their assumptions to ensure the analysis remains relevant and reliable

Difficulty with multi-product firms

- Breakeven analysis becomes more complex when dealing with multi-product firms

- Allocating fixed costs and determining the sales mix among different products can be challenging

- In such cases, entrepreneurs may need to use more advanced techniques, such as weighted average contribution margin, to conduct accurate breakeven analysis

Ignores time value of money

- Breakeven analysis does not take into account the time value of money

- It assumes that a dollar earned today is worth the same as a dollar earned in the future

- This limitation can be significant when considering long-term projects or investments where the timing of cash flows is important

Short-term vs long-term considerations

- Breakeven analysis primarily focuses on short-term profitability and does not consider long-term strategic objectives

- It does not account for factors such as market share, brand building, or customer loyalty, which may be important for long-term success

- Entrepreneurs should use breakeven analysis in conjunction with other strategic planning tools to make well-rounded decisions

Strategies for improving breakeven

- Entrepreneurs can employ various strategies to improve their breakeven point and increase profitability

- These strategies involve reducing costs, increasing prices, boosting sales volume, and optimizing the product mix

Reducing fixed costs

- Lowering fixed costs can significantly improve the breakeven point by reducing the overall cost structure

- Strategies for reducing fixed costs include negotiating better lease terms, outsourcing non-core functions, and optimizing staffing levels

- By minimizing fixed costs, businesses can lower their breakeven quantity and achieve profitability faster

Lowering variable costs

- Reducing variable costs per unit can help businesses improve their contribution margin and lower the breakeven point

- Strategies for lowering variable costs include negotiating better prices with suppliers, optimizing production processes, and reducing waste

- By decreasing variable costs, entrepreneurs can improve their profitability and competitiveness in the market

Increasing prices

- Increasing prices can help businesses generate more revenue per unit sold and lower the breakeven quantity

- However, entrepreneurs must carefully consider the impact of price increases on customer demand and market competitiveness

- Strategies for increasing prices include offering premium features, bundling products or services, and communicating the value proposition effectively

Boosting sales volume

- Increasing sales volume can help businesses spread their fixed costs over a larger number of units, reducing the breakeven quantity

- Strategies for boosting sales volume include expanding marketing efforts, entering new markets, and improving sales team performance

- By driving higher sales volume, entrepreneurs can achieve economies of scale and improve overall profitability

Optimizing product mix

- Optimizing the product mix involves focusing on the most profitable products or services and allocating resources accordingly

- By conducting breakeven analysis for each product or service, entrepreneurs can identify the offerings with the highest contribution margins and prioritize their sales efforts

- Strategies for optimizing product mix include phasing out less profitable products, bundling complementary offerings, and focusing on high-margin niche markets