The Modigliani-Miller theorem is a cornerstone of modern finance theory. It suggests that, under perfect market conditions, a company's value isn't affected by how it's financed. This challenges the idea that there's an optimal mix of debt and equity.

In reality, factors like taxes and bankruptcy costs do impact capital structure decisions. Companies must balance the tax benefits of debt against the risks of financial distress. This trade-off shapes how firms choose to finance their operations.

Modigliani-Miller Theorem Assumptions

Key Assumptions and Implications

- The Modigliani-Miller (MM) theorem, proposed by Franco Modigliani and Merton Miller, states that under certain assumptions, a firm's value is unaffected by its capital structure

- The value of a firm is determined by its earning power and the risk of its underlying assets, not by its debt-to-equity ratio

- The key assumptions of the MM theorem include:

- Perfect capital markets

- No taxes

- No transaction costs

- No bankruptcy costs

- Symmetry of market information

- No effect of debt on a firm's earnings before interest and taxes (EBIT)

- Under these assumptions, the MM theorem implies that the weighted average cost of capital (WACC) remains constant regardless of the debt-to-equity ratio

- The increase in the cost of equity offsets the lower cost of debt as leverage increases

- The irrelevance proposition of the MM theorem challenges the traditional view that a firm can optimize its value by finding the optimal debt-to-equity ratio

Arbitrage Mechanism and Investor Behavior

- In perfect capital markets, investors can create their own leverage or unlever the firm's equity returns by borrowing or lending on their own account

- This makes the firm's capital structure irrelevant, as investors can replicate any capital structure on their own

- The arbitrage mechanism plays a crucial role in the MM theorem

- If two firms with identical cash flows have different market values due to their capital structure, investors can exploit this mispricing by creating a portfolio that replicates the cash flows of the overvalued firm

- This arbitrage opportunity will drive the prices of the firms to their fundamental values, eliminating any capital structure-related valuation differences

- Under the MM assumptions, the cost of equity increases linearly with the debt-to-equity ratio, as the financial risk for equity holders increases with leverage

- This increase in the cost of equity exactly offsets the benefit of using cheaper debt financing, keeping the WACC constant

Capital Structure Irrelevance in Perfect Markets

Value Independence and Investor Replication

- In perfect capital markets, as assumed by the MM theorem, a firm's value is independent of its capital structure

- The debt-to-equity ratio does not affect the value of the firm, as the cash flows generated by the firm's assets determine its value

- Investors can replicate any capital structure by borrowing or lending on their own account

- If a firm has a high debt-to-equity ratio, investors can unlever their investment by holding a larger proportion of the firm's equity and lending money to offset the firm's debt

- Conversely, if a firm has a low debt-to-equity ratio, investors can lever their investment by borrowing money and investing in the firm's equity

Linear Relationship between Cost of Equity and Leverage

- As a firm increases its leverage, the financial risk for equity holders increases, leading to a higher required rate of return on equity

- The cost of equity increases linearly with the debt-to-equity ratio, compensating equity holders for the additional risk

- The increase in the cost of equity exactly offsets the benefit of using cheaper debt financing

- The weighted average cost of capital (WACC) remains constant regardless of the debt-to-equity ratio

- This linear relationship between the cost of equity and leverage is a key implication of the MM theorem in perfect capital markets

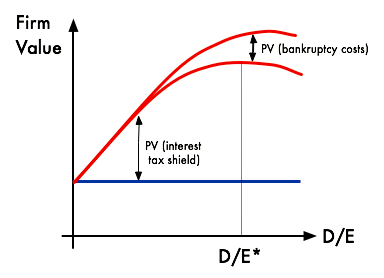

Taxes and Bankruptcy Costs on Capital Structure

Tax Shield Benefits and the Trade-off Theory

- When corporate taxes are introduced, the MM theorem is modified to recognize the tax shield benefits of debt

- Interest payments on debt are tax-deductible, creating a tax advantage for debt financing

- The value of the levered firm is equal to the value of the unlevered firm plus the present value of the tax shield

- The presence of corporate taxes encourages firms to use more debt in their capital structure

- Debt financing lowers the weighted average cost of capital (WACC) and increases the value of the firm

- However, the tax benefits of debt are limited by the potential costs of financial distress and bankruptcy

- The trade-off theory suggests that firms should balance the tax benefits of debt against the potential bankruptcy costs when making capital structure decisions

- The optimal capital structure is reached when the marginal tax benefits of debt equal the marginal expected bankruptcy costs

Bankruptcy Costs and Financial Distress

- Bankruptcy costs are the direct and indirect costs associated with a firm's financial distress and potential bankruptcy

- Direct costs include legal fees and administrative expenses

- Indirect costs include the loss of key employees, customers, and suppliers due to the perception of financial instability

- As a firm increases its leverage, the probability of financial distress and bankruptcy increases

- This increased risk of bankruptcy limits the extent to which a firm can benefit from the tax shield of debt

- Firms with higher profitability and more stable cash flows can afford to take on more debt, as they have a lower risk of bankruptcy

- Conversely, firms with volatile cash flows or operating in uncertain environments should be more conservative in their use of debt financing

Modigliani-Miller Theorem Applications

Industry-Specific Factors and Capital Structure

- While the MM theorem provides a useful framework for analyzing capital structure decisions, managers should consider industry-specific factors when making these decisions

- Firms in mature, stable industries with predictable cash flows (utilities) can afford to take on more debt than firms in rapidly growing or cyclical industries (technology)

- Regulated utilities often have higher debt ratios due to their stable cash flows and lower business risk

- The level of competition, the stage of the business cycle, and the regulatory environment also influence capital structure decisions

- Firms in highly competitive industries may prefer lower debt ratios to maintain financial flexibility and avoid the risk of financial distress

- During economic downturns, firms may reduce their debt levels to weather the storm and avoid bankruptcy

Pecking Order Theory and Signaling Effects

- The pecking order theory, an alternative to the trade-off theory, suggests that firms prefer internal financing over external financing and debt over equity when external financing is required

- This theory is based on the idea of asymmetric information between managers and investors

- Managers may choose to finance projects with internal funds or debt to avoid the perceived undervaluation of equity by the market

- Capital structure decisions can also have signaling effects

- Issuing debt may signal confidence in the firm's future cash flows and ability to meet its debt obligations

- Issuing equity may signal that managers believe the stock is overvalued, leading to a negative market reaction

Practical Considerations and Target Debt Ratios

- In practice, firms often set target debt ratios based on industry benchmarks and adjust their capital structure over time

- Firms may issue debt, issue equity, or repurchase shares to maintain their target debt ratios

- The speed at which firms adjust their capital structure depends on the costs of adjustment and the benefits of reaching the target ratio

- Managers should also consider the firm's growth opportunities, financial flexibility, and the costs and benefits of different financing options when making capital structure decisions

- Firms with valuable growth opportunities may prefer lower debt ratios to avoid the underinvestment problem and maintain financial flexibility

- The costs and benefits of different financing options, such as bank loans, bonds, or equity issuances, should be evaluated based on the firm's specific circumstances and market conditions